According to Fact.MR’s latest analysis, the Germany lithium and lithium-ion battery electrolyte market is valued at approximately USD 620 million in 2026 and is projected to reach USD 700 million in 2027, expanding to nearly USD 2.5 billion by 2036, registering a CAGR of 13.4%.

Germany is rapidly emerging as Europe’s battery manufacturing powerhouse, driven by aggressive EV adoption, strong OEM presence, and government-backed gigafactory investments. The market is transitioning from import dependence toward localized, high-performance electrolyte production aligned with EU battery regulations and sustainability standards.

Quick Stats

- Market Size (2026): USD 620 Million

- Market Size (2027): USD 700 Million

- Forecast Value (2036): USD 2.5 Billion

- CAGR (2026–2036): 13.4%

- Incremental Opportunity: USD 1.88 Billion

- Leading Segment: Lithium-based liquid electrolytes (~83% share)

- Leading End Use: Automotive (~42% share)

- Key Players: Mitsubishi Chemical, UBE Industries, Soulbrain MI, Capchem, Tinci

Executive Insight for Decision Makers

Germany’s electrolyte market is shifting toward localized, high-purity, and regulation-compliant production.

- OEMs and gigafactory operators must secure EU-compliant electrolyte supply chains to meet carbon footprint and traceability mandates.

- Manufacturers should invest in high-voltage and next-gen electrolyte technologies aligned with platforms like BMW’s Neue Klasse.

- Investors should prioritize companies with European production footprints and OEM qualification pipelines.

Failure to localize supply chains may lead to regulatory risks, supply disruptions, and increased dependency on Asian imports.

Market Dynamics

Key Growth Drivers

- Expansion of EV production and gigafactories in Germany

- Strong presence of automotive OEMs (BMW, Volkswagen, Mercedes-Benz)

- EU Battery Regulation compliance requirements

- Increasing adoption of high-energy-density battery chemistries

Key Restraints

- High production and compliance costs in Europe

- Dependence on imported lithium salts and solvents

- Long supplier qualification cycles

Emerging Trends

- Development of high-voltage electrolyte systems for premium EV platforms

- Increasing investment in solid-state battery electrolytes

- Localization of battery material supply chains under IPCEI programs

- Growing emphasis on low-carbon and sustainable electrolyte production

Segment Analysis

- By Product Type:Lithium-based liquid electrolytes dominate with ~83% share, widely used in NMC and LFP battery cells.

- By End Use:

- Automotive: ~42% share (largest segment driven by EV demand)

- Energy storage systems (fastest-growing segment)

- Consumer electronics

- Fastest-Growing Segment:Energy storage, supported by renewable energy integration and grid modernization initiatives.

Strategic Importance:

Electrolytes are critical to achieving higher energy density, faster charging, and safety compliance, particularly for premium EV platforms in Germany.

Supply Chain Analysis (Critical Insight)

Germany’s electrolyte supply chain is transitioning from import-heavy to localized integration:

- Raw Material Suppliers:Lithium salts (LiPF6), solvents, and specialty additives (primarily sourced from Asia)

- Manufacturers / Producers:European facilities by Mitsubishi Chemical, UBE Industries, and emerging local players

- Distributors / Integrators:Direct supply to battery cell manufacturers through long-term agreements

- End-Users:

- Automotive OEMs (BMW, Volkswagen, Mercedes-Benz)

- Energy storage system developers

- Industrial battery integrators

Who supplies whom:

Electrolyte producers supply European gigafactories (e.g., ACC, Northvolt partnerships in Germany) → which supply OEMs for EV production.

Supplier relationships are highly sticky due to strict qualification requirements.

Pricing Trends

- Commodity Electrolytes:Facing cost pressure from Asian imports

- Premium Electrolytes:High-performance formulations command premium pricing in Germany

- Key Influencing Factors:

- EU regulatory compliance costs

- Raw material imports

- Carbon footprint requirements

- Technology complexity

- Margin Insights:Higher margins are seen in advanced and sustainable electrolyte solutions.

Regional Analysis (Germany Focus)

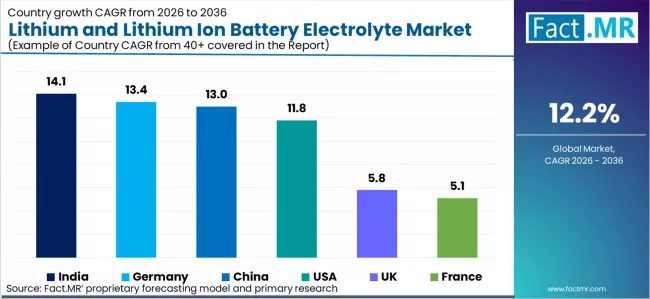

Germany stands as the fastest-growing electrolyte market in Europe, with a 13.4% CAGR through 2036.

- Growth Drivers:

- Expansion of gigafactories and EV production lines

- Government support through IPCEI Batteries initiatives

- Strong automotive ecosystem and supplier base

- Developed Market Advantage:Germany benefits from advanced infrastructure, R&D capabilities, and regulatory clarity, positioning it ahead of other European markets.

Competitive Landscape

- Market Structure:Moderately competitive with global leaders establishing local operations

- Key Players:

- Mitsubishi Chemical Group

- UBE Industries

- Soulbrain MI

- Shenzhen Capchem Technology

- Guangzhou Tinci Materials Technology

- Competitive Strategies:

- Establishment of European production facilities

- Development of advanced electrolyte chemistries

- Strategic partnerships with OEMs and gigafactories

- Focus on sustainability and compliance

Strategic Takeaways

- For Manufacturers:Localize production and invest in EU-compliant electrolyte technologies

- For Investors:Focus on companies with strong European expansion and OEM contracts

- For Marketers / Distributors:Highlight regulatory compliance, performance, and supply reliability

Future Outlook

Germany’s electrolyte market is expected to become a central hub for advanced battery materials in Europe.

- Growth in solid-state and next-generation electrolytes

- Increasing local production capacity

- Strong integration with European EV and energy ecosystems

Conclusion: Why This Market Matters

Germany is at the forefront of Europe’s battery revolution, and electrolytes are a critical component enabling this transformation. As EV adoption accelerates and regulatory standards tighten, the demand for high-performance, locally produced electrolyte solutions will surge.

For stakeholders, the opportunity lies in aligning with Germany’s localization push, technology innovation, and regulatory leadership, ensuring long-term growth and competitive advantage in the evolving battery ecosystem.