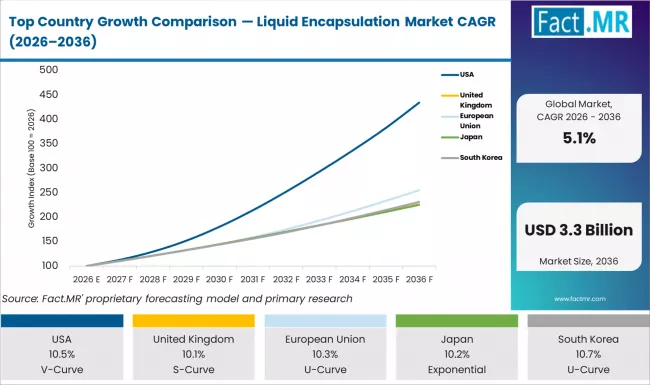

The South Korea Liquid Encapsulation Market is emerging as a high-growth regional hub, supported by the country’s global leadership in semiconductor manufacturing and advanced materials innovation. The market is estimated at USD 320 million in 2026, projected to reach USD 340 million in 2027, and is expected to surpass USD 530 million by 2036, expanding at a CAGR of 10.7%.

This growth trajectory reflects an incremental opportunity of over USD 210 million, driven by increasing demand for high-performance encapsulation materials in semiconductor packaging, pharmaceutical formulations, and specialty chemical applications.

South Korea’s transformation is fueled by its dominance in integrated circuit production, increasing investments in advanced packaging technologies, and expanding applications of encapsulated systems across high-value industries.

Quick Stats

- Market Size (2026): USD 320 Million

- Market Size (2027): USD 340 Million

- Forecast Value (2036): USD 530 Million

- CAGR (2026–2036): 10.7%

- Incremental Opportunity: USD 210 Million+

- Leading Material Segment: Epoxy Resin (~55% share)

- Leading Product Segment: Integrated Circuits (~40% share)

- Growth Driver: Semiconductor Packaging Expansion

- Key Players: Shin-Etsu Chemical Co., Ltd., BASF SE, Sumitomo Bakelite Co., Ltd., Nitto Denko Corporation, Dow Inc.

Executive Insight for Decision Makers

South Korea is transitioning toward high-precision encapsulation ecosystems, tightly integrated with semiconductor fabrication and advanced electronics manufacturing.

Strategic priorities:

- Expand epoxy-based encapsulation solutions for IC packaging

- Strengthen collaboration with semiconductor OEMs and foundries

- Invest in thermal management and miniaturization technologies

Risks of not adapting:

- Loss of relevance in next-generation chip packaging technologies

- Reduced competitiveness in export-driven electronics markets

- Margin pressure from global material suppliers

Market Dynamics

Key Growth Drivers

- Expansion of semiconductor manufacturing and IC packaging facilities

- Increasing need for moisture-resistant and thermally stable encapsulation materials

- Rising use of controlled release technologies in pharma and agrochemicals

- Growth in consumer electronics and automotive electronics production

Key Restraints

- High dependency on imported raw materials

- Complex formulation requirements for advanced encapsulation

- Cost sensitivity in high-volume electronics manufacturing

Emerging Trends

- Adoption of next-gen semiconductor packaging (advanced nodes, 3D ICs)

- Growth in microencapsulation for specialty chemicals

- Increasing use of high-purity epoxy systems

- Integration of AI and IoT devices requiring durable encapsulation

Segment Analysis

- Leading Segment:

- Epoxy Resin (~55% share) due to superior electrical insulation and thermal resistance

- Fastest-Growing Segment:

- Encapsulation for integrated circuits and advanced semiconductor devices

- Product Breakdown:

- Integrated Circuits (~40%)

- Sensors

- Discrete Semiconductors

- Optoelectronics

- Application Areas:

- Semiconductor Packaging

- Electronics Manufacturing

- Pharmaceuticals

- Specialty Chemicals

Strategic Insight:

Encapsulation materials are critical for ensuring chip durability, reliability, and performance stability, especially in high-density and miniaturized electronic systems.

Supply Chain Analysis (Critical Insight)

Raw Material Suppliers:

- Global petrochemical firms supplying epoxy resins, polymers, and additives

Manufacturers / Producers:

- Key suppliers such as Shin-Etsu Chemical Co., Ltd. and Sumitomo Bakelite Co., Ltd. produce high-performance encapsulation materials

Distributors:

- Regional specialty chemical distributors supplying to semiconductor fabs and OEMs

End-Users:

- Semiconductor companies (memory chips, logic ICs)

- Electronics OEMs

- Pharma and chemical formulation companies

Who supplies whom:

Global chemical suppliers → provide encapsulation materials → South Korean semiconductor manufacturers → integrate into chips and devices → exported globally through electronics supply chains.

Pricing Trends

- Commodity vs Premium:

- Standard encapsulation materials are cost-driven

- High-performance semiconductor-grade materials command premium pricing

- Key Influencing Factors:

- Semiconductor demand cycles

- Raw material price volatility

- Purity and performance requirements

- Customization for advanced packaging

- Margin Insights:

- Higher margins in specialized semiconductor encapsulation materials

- Competitive pricing pressure in bulk supply agreements

Regional Analysis – South Korea Focus

South Korea stands out as a global semiconductor powerhouse, driving strong demand for encapsulation materials.

- Growth driven by advanced chip manufacturing and export demand

- Strong ecosystem of electronics OEMs and material suppliers

- Government support for technology innovation and semiconductor investments

Positioning:

- Among the fastest-growing encapsulation markets globally

- High-value, innovation-driven demand compared to volume-driven markets

Competitive Landscape

- Market Structure: Moderately concentrated

- Key Players:

- Shin-Etsu Chemical Co., Ltd.

- Sumitomo Bakelite Co., Ltd.

- Nitto Denko Corporation

- BASF SE

- Dow Inc.

Competitive Strategies

- Focus on semiconductor-grade material innovation

- Long-term supply agreements with chip manufacturers

- Investment in R&D for advanced encapsulation performance

- Expansion of regional production and supply networks

Strategic Takeaways

For Manufacturers:

- Prioritize high-purity epoxy encapsulation systems

- Align with semiconductor production cycles

For Investors:

- Focus on companies linked to chip supply chains

- Target high-growth East Asian markets

For Distributors:

- Strengthen partnerships with electronics OEMs

- Offer customized and high-performance materials

Future Outlook

South Korea will remain a strategic growth hub for liquid encapsulation technologies, driven by:

- Continuous expansion in semiconductor manufacturing

- Rising demand for miniaturized and high-performance electronics

- Increasing adoption of advanced material science innovations

The market will see strong opportunities in next-generation chip packaging, AI-driven devices, and high-reliability electronics systems.

Conclusion: Why This Market Matters

South Korea’s liquid encapsulation market is at the forefront of global electronics innovation, where material performance directly impacts device reliability and technological advancement.

For decision-makers, the market offers a compelling opportunity to capitalize on semiconductor-driven demand, advanced material innovation, and export-oriented growth, making it a critical focus area in the global encapsulation landscape.

“