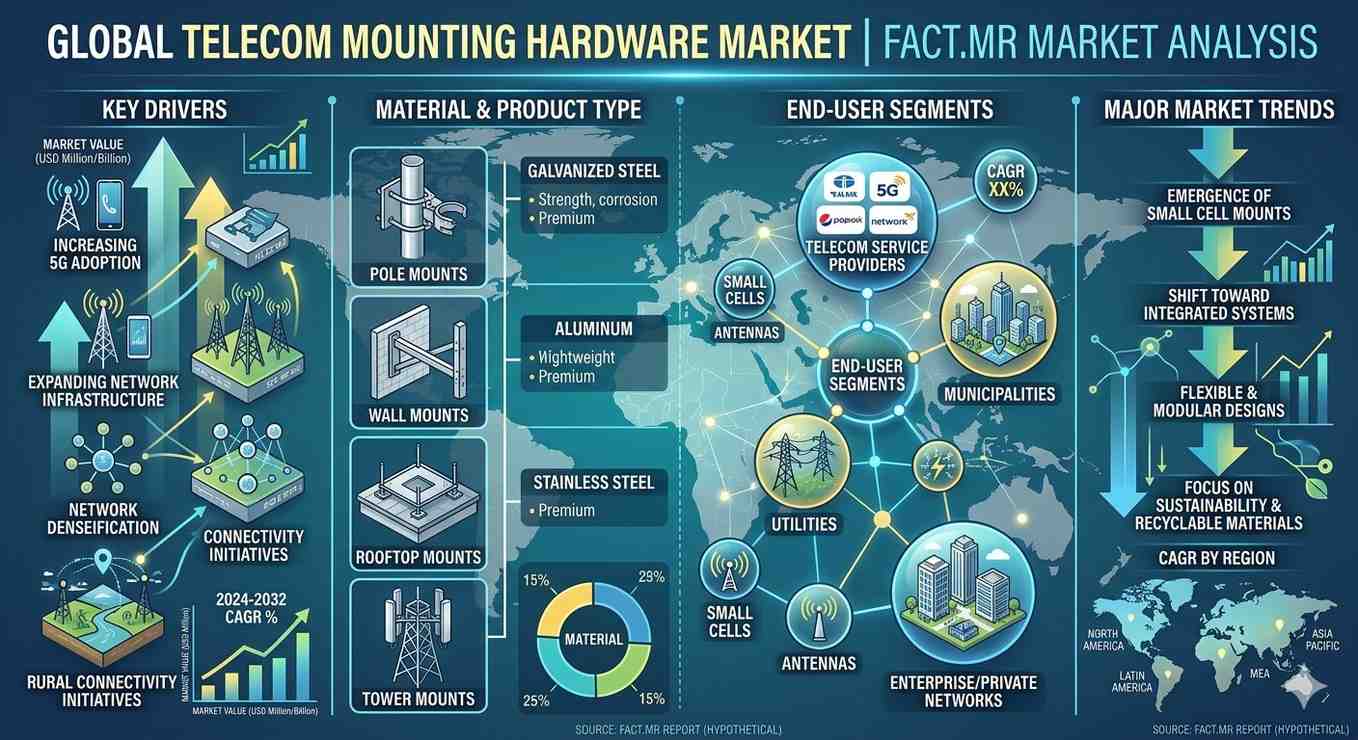

According to Fact.MR’s latest analysis, the global telecom mounting hardware market is experiencing robust expansion driven by 5G infrastructure rollout and network densification. While precise global valuation benchmarks vary by deployment scope, the market is projected to grow at a high single-digit CAGR through 2036, supported by sustained telecom capital expenditure.

The market is expected to expand steadily into 2027, driven by accelerated small cell deployments, fiber integration, and multi-band antenna installations. Incremental opportunity is being created through higher hardware value per site, as 5G systems require stronger, certified, and more complex mounting solutions compared to legacy infrastructure.

The transformation is fundamentally driven by the shift from macro tower-based deployments to dense, distributed network architectures, requiring mounting hardware across poles, rooftops, indoor venues, and urban infrastructure.

Quick Stats

- Market Outlook: Strong growth through 2036 (high single-digit CAGR)

- Growth Driver: 5G densification and small cell expansion

- Leading Component: Hardware (53.3% share)

- Leading Technology: 5G (48.2% share)

- Leading Region: Asia Pacific

- Top Growth Countries: China (10.5%), India (9.8%), Germany (8.8%), France (8.0%), UK (7.5%)

- Key Players: Valmont Industries, CommScope, Ericsson, Nokia, Amphenol, Huawei, ZTE

Executive Insight for Decision Makers

The market is undergoing a structural shift from volume-driven hardware supply to engineering-intensive, compliance-led solutions.

- OEMs and manufacturers must focus on certified, load-bearing, and concealment-ready hardware systems tailored for 5G and small cells.

- Investors should prioritize companies with engineering capabilities, regulatory certifications, and carrier partnerships.

- Companies failing to evolve beyond commodity hardware risk margin compression and exclusion from approved vendor ecosystems.

Market Dynamics

Key Growth Drivers

- Rapid expansion of 5G networks and small cell deployments

- Increasing demand for multi-band and massive MIMO antenna systems

- Growth of fiber backhaul and indoor DAS infrastructure

- Rising need for aesthetic, regulation-compliant mounting solutions

Key Restraints

- Complex permitting and regulatory approval processes

- High engineering validation and certification requirements

- Extended deployment timelines due to site-specific customization

Emerging Trends

- Growth in concealment-ready and RF-transparent enclosures

- Development of reinforced mounts for heavy multi-band antennas

- Increasing adoption of hybrid 4G/5G infrastructure systems

- Shift toward street-level and indoor deployment architectures

Segment Analysis

- Leading Segment (Component): Hardware (53.3% share)

- Leading Segment (Technology): 5G (48.2% share)

- Fastest-Growing Segment: Small cell and street-level mounting systems

Market Breakdown

By Component:

- Structural mounts

- Grounding systems

- Cable management solutions

By Technology:

- 5G (dominant)

- 4G/LTE (declining share but integrated with hybrid systems)

Strategic Importance:

Hardware forms the foundation of every telecom deployment, with each site requiring certified structural systems before network activation. With 5G, hardware complexity and value per site have increased significantly.

Supply Chain Analysis (Critical Insight)

The telecom mounting hardware market operates through a highly structured, compliance-driven supply chain:

- Raw Material Suppliers

- Steel, aluminum, and composite material providers

- Coating and corrosion-resistant material suppliers

- Manufacturers / Producers

- Structural hardware manufacturers producing mounts, enclosures, and brackets

- Integrated telecom equipment providers bundling hardware with radios

- Distributors & Integrators

- Tower companies and infrastructure providers

- Telecom system integrators managing site deployment

- End Users

- Telecom operators (mobile carriers)

- Tower companies

- Enterprise network operators (stadiums, campuses, industrial sites)

“Who Supplies Whom”

Material suppliers → Hardware manufacturers → Integrators/tower companies → Telecom operators

This chain is governed by strict certification, engineering validation, and approved vendor lists, limiting entry for low-cost suppliers.

Pricing Trends

- The market is transitioning from commodity pricing to premium, engineering-led pricing models

Pricing Structure

- Standard mounts: Lower-cost, commodity-driven

- Advanced 5G mounts: Premium pricing due to load certification and customization

Key Influencing Factors

- Wind load and structural certification requirements

- Compatibility with multi-band and massive MIMO systems

- Regulatory compliance and aesthetic standards

- Deployment scale and contract duration

Margin Insights

- Higher margins for certified, engineered solutions

- Commodity hardware faces price pressure and low differentiation

Regional Analysis

Top Countries by CAGR (2026–2036)

- China: 10.5%

- India: 9.8%

- Germany: 8.8%

- France: 8.0%

- United Kingdom: 7.5%

Regional Insights

- Asia Pacific: Leads global volumes due to large-scale 5G deployment in China and India

- Europe: Growth driven by regulatory frameworks and rural broadband expansion

- North America: Strong demand from small cell deployments and enterprise networks

Developed vs Emerging Markets

- Developed markets emphasize compliance, certification, and advanced systems

- Emerging markets focus on rapid deployment and infrastructure expansion

Competitive Landscape

The market is moderately concentrated in high-value certified hardware and fragmented in low-cost components.

Key Players

- Valmont Industries

- CommScope

- Ericsson

- Nokia

- Amphenol

- Huawei

- ZTE

- American Tower Corporation

- Cisco

- Ubicquia

Competitive Strategies

- Development of certified, high-load structural systems

- Integration with radio and network equipment platforms

- Expansion of global manufacturing and supply chains

- Focus on municipal compliance and aesthetic solutions

Strategic Takeaways

For Manufacturers

- Invest in engineering capabilities and certification standards

- Develop 5G-specific, high-load mounting solutions

For Investors

- Target companies with strong telecom operator relationships

- Focus on high-margin, compliance-driven segments

For Marketers & Distributors

- Emphasize certification, reliability, and compatibility

- Build long-term contracts with tower companies and operators

Future Outlook

The market will evolve toward dense, distributed telecom infrastructure, requiring mounting hardware across diverse environments.

- Growth in small cells and urban deployments

- Increasing demand for concealed and integrated mounting systems

- Expansion of shared infrastructure models

Long-term, mounting hardware will remain a critical enabler of telecom network scalability and performance.

Conclusion

The global telecom mounting hardware market is transitioning into a high-value, engineering-driven sector, shaped by 5G densification and infrastructure modernization.

Companies that focus on certification, customization, and integration capabilities will capture the greatest share of future growth.

Why This Market Matters

Telecom mounting hardware is the physical backbone of wireless connectivity, enabling the deployment of next-generation networks.

As 5G and beyond reshape global communications, this market plays a central role in delivering reliable, high-performance connectivity infrastructure worldwide.

Browse Full Report:

https://www.factmr.com/report/telecom-mounting-hardware-market