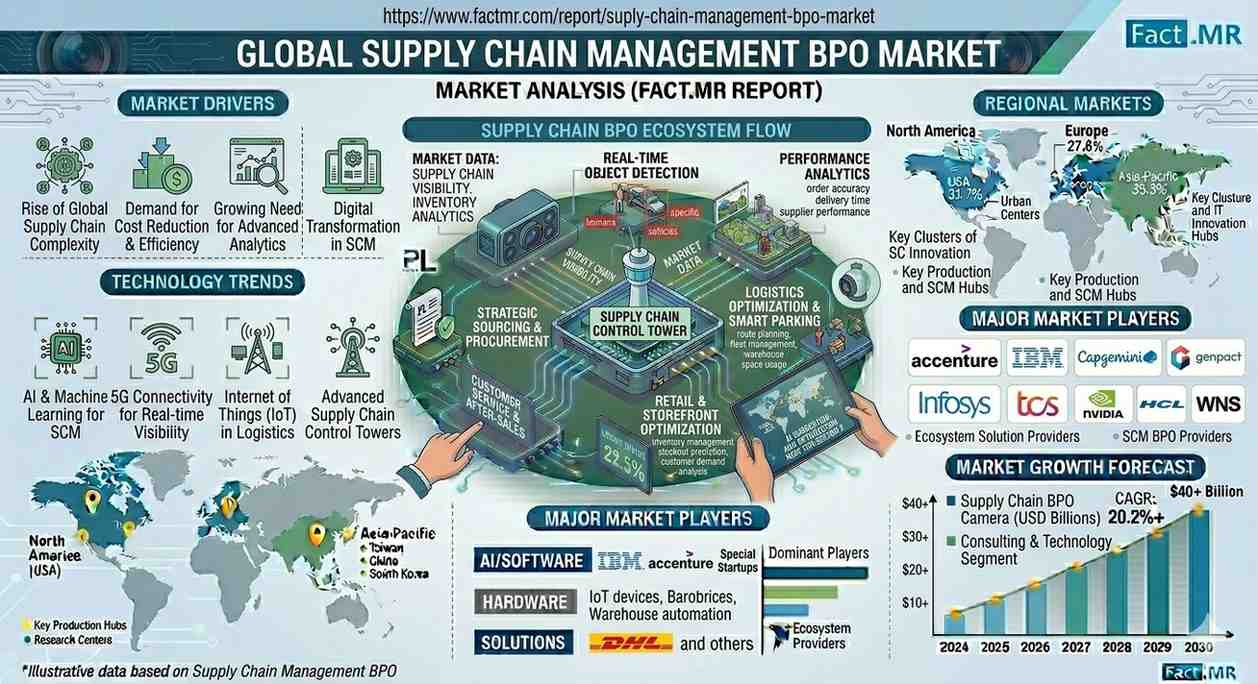

According to Fact.MR’s latest analysis, the global supply chain management BPO market is valued at approximately USD 87.5 billion in 2026, projected to reach USD 93.8 billion in 2027, and expand to USD 173 billion by 2036, registering a steady CAGR of 7.1% during the forecast period.

The market is expected to generate an incremental opportunity of over USD 85 billion, driven by increasing enterprise reliance on outsourced logistics coordination, inventory optimization, and compliance management.

The sector is undergoing a strategic transition from cost-driven outsourcing to intelligence-driven supply chain orchestration, fueled by AI-enabled forecasting, nearshoring strategies, and rising regulatory complexity across global trade ecosystems.

Quick Stats

- Market Size (2026): USD 87.5 Billion

- Market Size (2027): USD 93.8 Billion

- Forecast Value (2036): USD 173 Billion

- CAGR (2026–2036): 7.1%

- Incremental Opportunity: USD 85+ Billion

- Leading Segment: Offshoring Model (56% share)

- Leading Application: Retail & CPG (34% share)

- Leading Region: Asia-Pacific (India, Philippines, China)

- Key Players: Accenture, IBM, Tata Consultancy Services (TCS), Capgemini, Genpact

Executive Insight for Decision Makers

The market is shifting from labor arbitrage to AI-powered supply chain intelligence platforms.

Strategic Imperatives

- Invest in AI-driven demand forecasting and inventory optimization

- Expand nearshore delivery centers to address data sovereignty

- Build compliance-led outsourcing capabilities, especially in healthcare and ESG

For OEMs / Enterprises

- Transition from fragmented outsourcing to integrated BPO ecosystems

- Partner with providers offering end-to-end visibility and analytics

Risks of Not Adapting

- Increased exposure to supply chain disruptions

- Inability to meet regulatory compliance mandates

- Loss of competitiveness in e-commerce-driven fulfilment models

Market Dynamics

Key Growth Drivers

- E-commerce Expansion: Increasing outsourcing of fulfilment and last-mile coordination

- Regulatory Compliance Complexity: DSCSA and EU due diligence laws driving demand

- Supply Chain Resilience Needs: Vendor risk management outsourcing rising

- Healthcare Logistics Growth: Cold chain and pharmaceutical compliance outsourcing

Key Restraints

- Data Security & Sovereignty Concerns

- Dependence on Third-Party Providers

- Integration Complexity with Legacy Systems

Emerging Trends

- AI-powered Demand Sensing & Forecasting Platforms

- Nearshoring and Regional BPO Expansion

- End-to-End Digital Supply Chain Visibility

- Outsourcing of Tier-2 and Tier-3 Supplier Management and Procurement Analytics

Segment Analysis

Leading Segment

- Offshoring Model: Holds 56% market share due to cost efficiency and skilled workforce availability

Fastest-Growing Segment

- Nearshoring Models: Driven by regulatory compliance and geopolitical risk mitigation

Breakdown

- By Application:

- Retail & CPG (34%)

- Manufacturing

- Healthcare

- By Service Type:

- Logistics management outsourcing dominates

- By Enterprise Size:

- Large enterprises lead due to complex global supply chains

Strategic Importance

- Retail drives volume and scale

- Healthcare drives high-margin compliance outsourcing

- Manufacturing drives analytics and supplier management demand

Supply Chain Analysis (Critical Insight)

- Raw Input Layer

- Data inputs from ERP systems, logistics networks, supplier databases

- Digital infrastructure including cloud and analytics platforms

- BPO Service Providers

- Deliver logistics coordination, inventory control, procurement analytics

- Provide AI forecasting, compliance monitoring, vendor risk management

- Technology Providers

- Cloud platforms, AI engines, and automation tools enabling BPO services

- Distribution & Integration

- System integrators embed BPO services into enterprise workflows

- Managed service providers ensure continuous operations

- End-Users

- Retailers and e-commerce firms

- Manufacturing companies

- Healthcare and pharmaceutical firms

- Logistics and distribution companies

Who Supplies Whom

- Tech providers → BPO firms (platforms and analytics tools)

- BPO firms → Enterprises (outsourced supply chain services)

- Logistics partners → BPO providers (execution support)

- Enterprises → End customers (final product delivery)

Pricing Trends

Pricing Structure

- Commodity Services: Basic transaction processing with lower margins

- Premium Services: AI analytics, compliance, and integrated platforms command higher pricing

Key Pricing Factors

- Labor cost differentials (offshore vs nearshore)

- Technology integration and automation levels

- Regulatory compliance requirements

- Contract complexity and service scope

Margin Insights

- Traditional BPO margins under pressure

- AI-enabled services deliver higher-value, long-term contracts

Regional Analysis

Top 5 Countries by CAGR (2026–2036)

- China – 8.2%

- South Korea – 7.8%

- Japan – 7.5%

- Germany – 7.4%

- France – 7.2%

Regional Insights

- Asia-Pacific: Dominates delivery with strong outsourcing hubs and e-commerce growth

- North America: Highest revenue generation with advanced enterprise outsourcing

- Europe: Compliance-driven demand across automotive and healthcare sectors

Developed vs Emerging Markets

- Developed markets: Focus on compliance and advanced analytics

- Emerging markets: Focus on cost efficiency and scalability

Competitive Landscape

- Market Structure: Blended—consolidated at enterprise level, fragmented in mid-market

Key Players

- Accenture

- IBM Corporation

- Tata Consultancy Services (TCS)

- Capgemini

- Genpact

- Wipro Limited

- Infosys

- DHL Supply Chain

- Cognizant

- EXL Service

Competitive Strategies

- Investment in AI and automation platforms

- Expansion of global delivery centers

- Industry-specific solutions for healthcare, retail, and manufacturing

- Long-term multi-country outsourcing contracts

Strategic Takeaways

For Manufacturers / Enterprises

- Outsource non-core supply chain functions

- Leverage AI-driven forecasting and analytics

For Investors

- Focus on providers with strong digital and AI capabilities

- Target firms expanding in nearshore and compliance services

For Marketers / Distributors

- Position services around resilience, compliance, and cost optimization

- Highlight end-to-end supply chain visibility

Future Outlook

The market is moving toward intelligent, autonomous supply chain ecosystems, where BPO providers act as strategic partners rather than service vendors.

Key Trends Ahead

- AI-driven decision-making across supply chains

- Expansion of nearshore outsourcing hubs

- Integration of ESG and compliance frameworks

Long-Term Opportunity

- Growth in pharmaceutical, e-commerce, and manufacturing outsourcing

- Emergence of platform-based BPO ecosystems

Conclusion

The global supply chain management BPO market is evolving into a strategic enabler of enterprise resilience and efficiency. As supply chains become more complex and regulated, outsourcing is no longer optional—it is a competitive necessity.

Organizations that embrace AI-enabled outsourcing, regional diversification, and compliance integration will be best positioned to capture long-term value in this rapidly evolving market.

Why This Market Matters

- Enables resilient global supply chains

- Supports e-commerce and digital trade growth

- Ensures regulatory compliance and risk mitigation

- Drives operational efficiency and cost optimization

Browse Full Report –

https://www.factmr.com/report/supply-chain-management-bpo-market