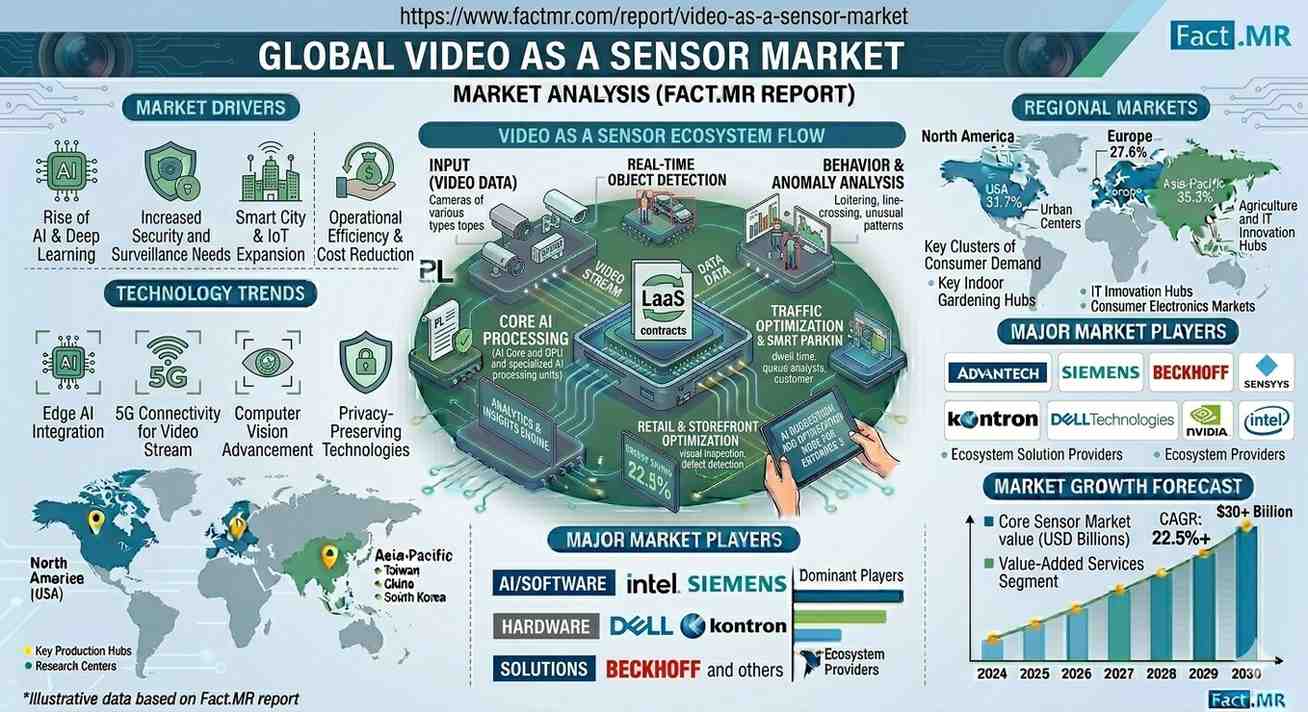

According to Fact.MR’s latest analysis, the global video as a sensor market is valued at approximately USD 8.5 billion in 2026 and is projected to reach USD 9.3 billion in 2027, expanding to nearly USD 19.5 billion by 2036. The market is expected to grow at a CAGR of 8.6% from 2026 to 2036, generating an incremental opportunity of USD 11.0 billion.

The market is undergoing a critical transformation from traditional video surveillance to AI-enabled perception systems, where cameras function as intelligent sensors. Integration of machine learning, edge processing, and real-time analytics is enabling applications across smart cities, industrial automation, automotive systems, and retail intelligence.

Quick Stats

- Market Size (2026): USD 8.5 billion

- Market Size (2027): USD 9.3 billion

- Forecast Value (2036): USD 19.5 billion

- CAGR (2026–2036): 8.6%

- Incremental Opportunity: USD 11.0 billion

- Leading Segment: Hardware Components (45% share)

- Leading Sensor Type: RGB Sensors (dominant share)

- Leading Region: Asia-Pacific (China & India growth hubs)

- Key Players: Hikvision, Bosch Security Systems, Motorola Solutions, Sony, Honeywell

Executive Insight for Decision Makers

The market is shifting toward video-driven intelligence ecosystems, where data captured through cameras is processed in real time to support decision-making, automation, and predictive analytics.

Strategic Imperatives:

- Invest in edge AI and on-device processing capabilities

- Ensure cybersecurity compliance and data protection frameworks

- Build scalable solutions integrating cloud, IoT, and analytics platforms

Risk of Inaction:

Organizations that fail to adopt intelligent video sensing risk losing competitiveness in automation, safety, and operational efficiency, especially in smart infrastructure and Industry 4.0 environments.

Market Dynamics

Key Growth Drivers

- Expansion of AI and machine vision technologies

- Increasing deployment of smart city infrastructure

- Rising demand for real-time monitoring and predictive analytics

- Growth in ADAS, robotics, and industrial automation

Key Restraints

- Data privacy and regulatory concerns

- High cost of advanced AI-enabled systems

- Integration challenges with legacy infrastructure

Emerging Trends

- Adoption of edge AI for real-time analytics

- Growth of cloud-integrated video sensing platforms

- Development of multi-sensor fusion systems

- Increasing focus on cybersecurity and compliance frameworks

Segment Analysis

- Leading Segment: Hardware components hold 45% share, driven by cameras, processors, and connectivity infrastructure

- Fastest-Growing Segment: AI-powered analytics software and edge processing units

Breakdown:

- By Component: Hardware, software, services

- By Sensor Type: RGB sensors (dominant), thermal, infrared

- By Application: Surveillance, industrial monitoring, retail analytics, automotive, smart cities

Strategic Importance:

Hardware forms the foundation of video sensing, while AI-driven software unlocks value through analytics and automation.

Supply Chain Analysis (Critical Insight)

Value Chain Structure

- Raw Material & Component Suppliers:

Semiconductor manufacturers, imaging sensors, processors, connectivity modules - Device Manufacturers:

Produce cameras, edge processors, and integrated video systems - Platform Providers & Integrators:

Develop analytics software, cloud platforms, and system integration solutions - End-Users:

- Government and smart city authorities

- Industrial enterprises

- Retail and commercial facilities

- Automotive and robotics companies

Who Supplies Whom

- Semiconductor firms supply image sensors and processors to camera manufacturers

- Companies like Hikvision and Bosch deliver systems to enterprises and public infrastructure projects

- Cloud providers enable analytics and remote monitoring capabilities

Insight:

The supply chain is technology-intensive, with value increasingly shifting toward software, AI, and integrated platforms.

Pricing Trends

- Basic surveillance systems follow commodity pricing

- Advanced AI-enabled systems command premium pricing

Key Influencers

- Processing capability and AI integration

- Data security and compliance features

- Scalability and cloud integration

- Application-specific customization

Margin Insight:

Higher margins are driven by software, analytics, and service layers, rather than hardware alone.

Regional Analysis

Top Countries by CAGR (2026–2036)

- China: 10.9%

- India: 10.1%

- Germany: 9.3%

- United Kingdom: 7.7%

- United States: 6.9%

Regional Insights

- Asia-Pacific: Dominates due to smart city investments and industrial automation

- Europe: Growth driven by regulatory compliance and industrial use cases

- North America: Strong adoption in enterprise analytics and smart infrastructure

Developed vs Emerging Markets:

- Developed markets focus on AI integration and compliance

- Emerging markets emphasize infrastructure expansion and scalability

Competitive Landscape

- Market Structure: Moderately consolidated with strong global leaders

Key Players

- Hangzhou Hikvision Digital Technology Co., Ltd.

- Dahua Technology Co., Ltd.

- Motorola Solutions, Inc.

- Honeywell International Inc.

- Bosch Security Systems GmbH

- Axis Communications AB (Canon Group)

- Sony Corporation

- Teledyne FLIR LLC

- Panasonic Corporation

- Hanwha Techwin Co., Ltd.

- Cisco Systems, Inc.

- IBM Corporation

- Microsoft Corporation

- Amazon Web Services, Inc.

- Google LLC

Competitive Strategies

- Investment in AI and machine vision capabilities

- Expansion of cloud-based analytics platforms

- Focus on cybersecurity and regulatory compliance

- Strategic acquisitions and partnerships

Strategic Takeaways

For Manufacturers

- Focus on AI-enabled and edge computing solutions

- Enhance hardware-software integration capabilities

For Investors

- Target companies with strong AI and cloud ecosystems

- Invest in smart infrastructure and automation segments

For Marketers & Distributors

- Emphasize real-time analytics and operational efficiency benefits

- Align offerings with smart city and enterprise transformation needs

Future Outlook

The market is expected to evolve into a fully integrated visual intelligence ecosystem, where video sensors play a central role in autonomous decision-making systems.

Key opportunities include:

- Expansion into autonomous vehicles and robotics

- Growth of AI-powered predictive analytics platforms

- Integration with IoT and smart infrastructure systems

Conclusion

The global video as a sensor market is transitioning into a core pillar of intelligent automation and digital infrastructure, driven by advancements in AI and real-time analytics. Companies that invest in integrated, secure, and scalable solutions will lead the next phase of growth.

Why This Market Matters

Video as a sensor technology is redefining how systems perceive and interact with the world. As industries move toward automation, safety, and data-driven decision-making, this market becomes essential to enabling next-generation intelligent environments and connected ecosystems.

Browse Full Report –

https://www.factmr.com/report/video-as-a-sensor-market