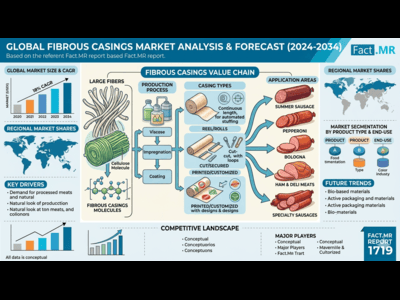

The global meat processing industry is undergoing a structural transition as “clean label” demands meet industrial efficiency. Driven by a surge in processed meat consumption and a move toward sustainable, plant-derived packaging, the global fibrous casing market is reaching a new peak.

Latest data from Fact.MR reveals the market is valued at US$ 3.7 billion in 2024 and is projected to reach US$ 6 billion by 2034, expanding at a steady 5% CAGR. For decision-makers in the food processing and packaging sectors, this trajectory highlights a critical shift: fibrous casings are no longer just a functional tool—they are a core component of food safety and consumer trust.

Quick Stats: The Fibrous Casing Outlook (2024–2034)

| Attribute | Detail |

| Market Value (2024E) | US$ 3.7 Billion |

| Projected Value (2034F) | US$ 6 Billion |

| Global Growth Rate | 5% CAGR |

| Clear Casings Market Share | 30% (US$ 1.8 Billion by 2034) |

| Luncheon Meats Segment | 28.1% of Global Revenue |

| South Korea Growth Rate | 5.7% CAGR (Regional Leader) |

The Material Advantage: Strength Meets Sustainability

Fibrous casings, primarily derived from natural cellulose and plant fibers, are becoming the preferred medium for high-diameter meat products like salami, pepperoni, and ham.

- Shelf-Life Excellence: Unlike synthetic alternatives, fibrous casings offer superior moisture and oxygen barrier capabilities. Their high resistance to breakage ensures meat products do not dry out or collapse, significantly extending shelf life in frozen and refrigerated retail environments.

- The “Clear” Winner: Transparent or Clear Casings are projected to grow at a 5% CAGR. In an era of “visual inspection,” consumers increasingly demand to see the product quality, marbling, and freshness before purchase. This transparency is a key driver for building brand trust at the deli counter.

- Sustainable Compliance: As environmental regulations tighten, the plant-based origin of fibrous casings offers an eco-friendly alternative to artificial plastics, aligning with global ESG mandates and “green” packaging trends.

Strategic Regional Dynamics: North America vs. East Asia

- North America (24.3% Market Share): Led by the United States, which is expected to reach a value of US$ 677 million by 2034. The region’s growth is fueled by a massive frozen food sector and an increasing number of fast-food chains requiring standardized, high-performance meat components.

- East Asia (23.1% Market Share): China is the primary focal point, contributing 5% of the regional share. The modernization of the Chinese food industry is pushing manufacturers away from traditional methods toward advanced packaging technologies that improve product presentation and hygiene.

The Innovation Frontier: Overcoming Market Roadblocks

While the rise of veganism and meat taxes pose challenges to the traditional meat sector, startups and legacy players are capitalizing on technological advancements. Modern R&D is focused on increasing the “viscosity” and durability of casings to handle high-speed industrial stuffing and specialized plant-based meat substitutes.

Browse Full Report –

https://www.factmr.com/report/1719/fibrous-casings-market