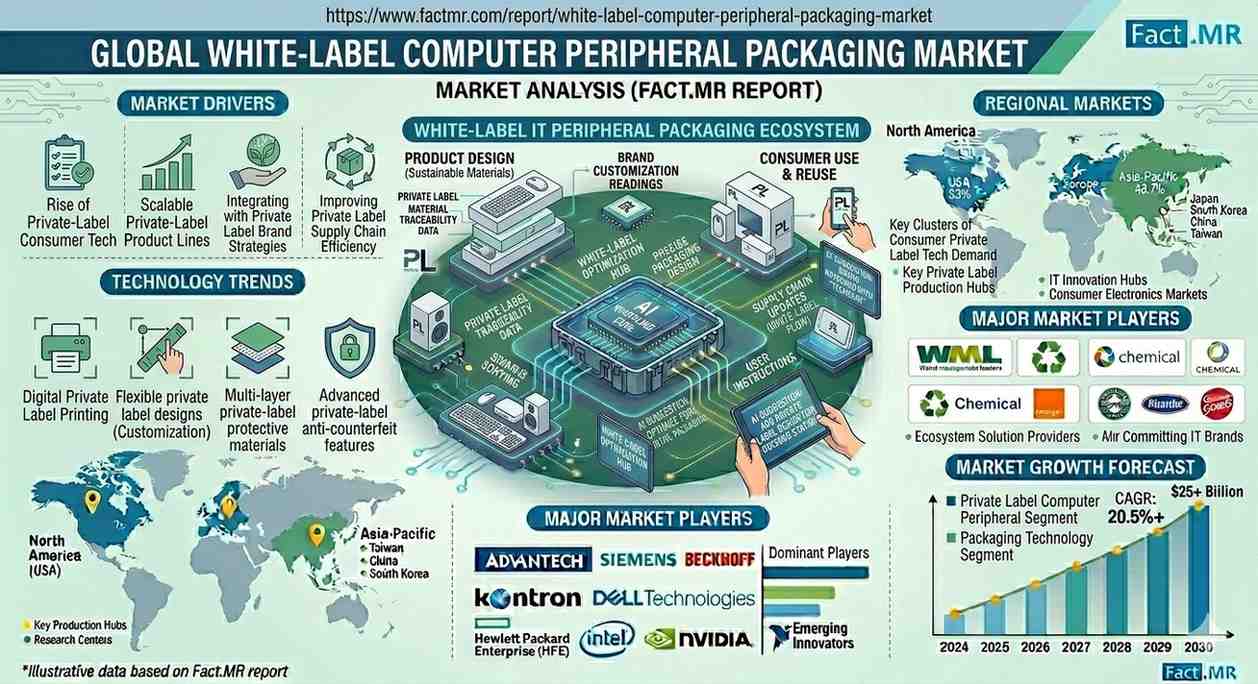

The global White-Label Computer Peripheral Packaging Market is undergoing a period of rapid industrialization. Valued at USD 535.5 million in 2026, the market is projected to climb to USD 932.2 million by 2036, expanding at a steady 5.7% CAGR.

As retailers, e-commerce giants, and Original Equipment Manufacturers (OEMs) aggressively expand their private-label portfolios—ranging from generic keyboards and mice to high-speed chargers—the demand for “neutral” yet high-quality packaging has become a cornerstone of the global electronics supply chain.

Get detailed market forecasts, competitive benchmarking, and pricing trends:

https://www.factmr.com/connectus/sample?flag=S&rep_id=13926

Quick Stats: Market at a Glance

| Metric | Details |

| Market Value (2026E) | USD 535.5 Million |

| Projected Value (2036F) | USD 932.2 Million |

| Growth Rate (CAGR) | 5.7% |

| Dominant Format | Folding Cartons (48.3% Share) |

| Primary Customer | OEM Private Label (44.1% Share) |

| Leading Material | Paperboard (56.7% Share) |

Expert Insights: The Rise of the “Generic Premium”

The white-label market is no longer just about low-cost alternatives; it is about high-speed brand agility.

“White-label packaging is the engine of the ‘ghost brand’ economy,” notes a senior supply chain analyst. “When a retailer wants to launch a private-label webcam or adapter, they don’t want to redesign the box—they want a standardized, high-performance template they can brand in days, not months. The dominance of folding cartons (48.3% share) and paperboard (56.7% share) reflects a global need for packaging that is cost-effective, easy to print, and 100% recyclable.”

Key Market Drivers & Trends

- OEM Customization: OEM private label brands command 1% of the market, as manufacturers increasingly offer “turnkey” solutions where the product and the packaging are delivered ready for retail branding.

- Standardization Over Differentiation: Suppliers are moving toward standardized structures with “customizable print zones,” allowing brands to refresh their look without expensive re-tooling.

- The E-commerce Push: Third-party fulfillment (3PL) brands are driving a shift toward mailers and bags for small peripherals, prioritizing fulfillment speed and shipping weight over shelf aesthetics.

🌏 Regional Outlook: Asia-Pacific’s Manufacturing Powerhouse

The geographical center of gravity for this market remains firmly in the East, where production and consumption are rising simultaneously.

- India (7.4% CAGR): The global growth leader. India’s burgeoning online marketplaces are hungry for private-label accessories, fueling a massive demand for scalable, locally-produced folding cartons.

- Vietnam (6.8% CAGR): Emerging as a primary alternative for global OEMs, Vietnam’s packaging sector is optimizing for export-grade paperboard solutions.

- United States (3.2% CAGR): A mature market where growth is driven by established retail chains (like Best Buy or Amazon) expanding their house-brand peripheral lines.

- Mexico (5.3% CAGR): A key player in the North American “near-shoring” trend, providing rigid boxes and cartons for the regional assembly of higher-value peripherals.

🏆 Competitive Landscape

The market is characterized by global packaging titans that offer “platform-based” solutions. These companies allow white-label brands to achieve economies of scale through standardized material sourcing.

Key Industry Leaders:

- Mondi & Smurfit Kappa: Leaders in high-quality, recyclable paperboard and folding cartons.

- Berry Global & Amcor: Providing specialized hybrid and plastic-based packaging for high-protection needs.

- Sealed Air & Ranpak: Focusing on the protective “void-fill” inside white-label boxes to reduce transit damage.

- WestRock & International Paper: Scaling high-volume production lines for global OEM private-label contracts.

🔍 Featured Snippet: White-Label Packaging FAQs

What is White-Label Computer Peripheral Packaging?

It is a “neutral” packaging solution designed for computer accessories (like mice, cables, and chargers) that are manufactured by one company but sold under another company’s brand name. It allows retailers or distributors to apply their own branding to a standardized, high-quality box without the cost of custom structural design.

Why are folding cartons the preferred packaging for white-labels?

Folding cartons hold a 48.3% market share because they offer the best balance of cost-efficiency and print flexibility. They allow for rapid artwork changes—essential for white-labeling—while protecting the product during both retail display and e-commerce shipping.

How does OEM private-label packaging differ from retail packaging?

OEM private-label packaging (accounting for 44.1% of the market) focuses on consistency and regulatory compliance across multiple regions. It is typically designed to be “brand-ready” so that any retailer can purchase the product and quickly apply their own logo and localized labels.

Full Report: Unlock 360° insights for strategic decision making and investment planning-

https://www.factmr.com/checkout/13926