The global energy landscape is standing at a critical juncture where the electric vehicle (EV) is no longer merely a transport asset, but a mobile battery capable of stabilizing national grids. According to the latest strategic analysis by Fact.MR, the global V2X (Vehicle-to-Everything) Bidirectional EV Charger Market is projected to surge from $1.03 billion in 2026 to $4.1 billion by 2036.

This high-velocity expansion, characterized by a 14.8% CAGR, represents an absolute dollar growth of over $3 billion in just ten years. As governments and utilities scramble to integrate volatile renewable energy sources like wind and solar, the ability to pull power back from EV batteries—known as “Vehicle-to-Grid” (V2G) and “Vehicle-to-Home” (V2H)—has moved from a pilot-phase concept to a core pillar of modern grid resilience.

The Shift to Decentralized Power: Why Bidirectional is the New Standard

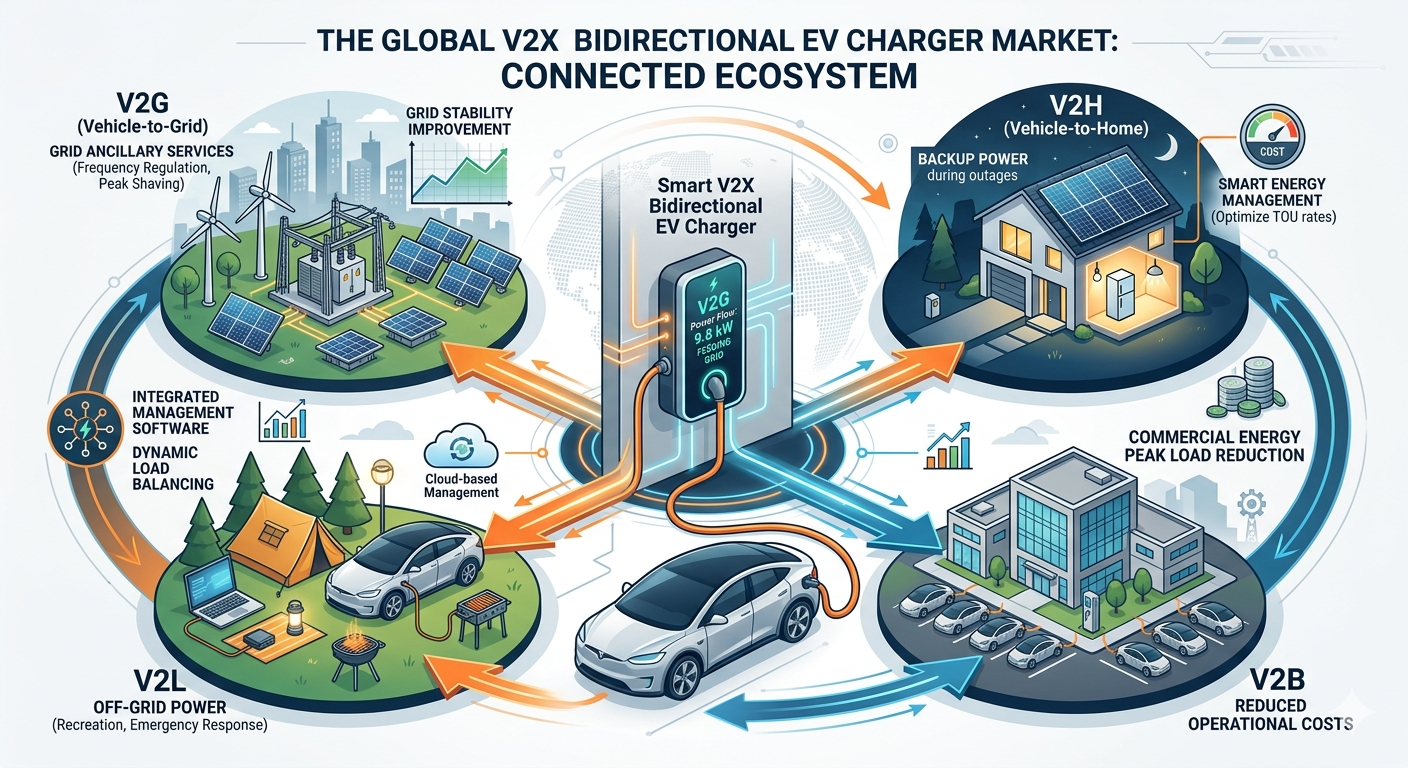

The traditional unidirectional charging model is increasingly viewed as a missed opportunity in the era of smart cities. The new era of V2X technology enables a two-way power flow, allowing EVs to function as Distributed Energy Resources (DERs).

Several critical factors are accelerating this transition:

- Grid Modernization & Peak Shaving: Utilities are incentivizing bidirectional charging to manage peak demand, using parked EVs to discharge power during high-load periods.

- Energy Resilience & Backup: Rising climate-related outages have spiked interest in V2H (Vehicle-to-Home) systems, where an EV can power a household for multiple days during an emergency.

- Renewable Energy Buffering: Bidirectional chargers act as the “missing link” for solar and wind power, storing excess daytime energy in car batteries and releasing it when the sun sets.

- Fleet Optimization: Commercial operators are turning fleets into revenue-generating assets by selling battery capacity back to the grid during downtime.

Dominant Segments: DC Power and the “Sweet Spot” of Capacity

The market is currently seeing a definitive tilt toward DC Bidirectional Chargers, which currently command approximately 55–60% of total revenue. Unlike AC systems, DC chargers bypass the vehicle’s onboard converter, offering higher power output, faster discharge rates, and seamless compatibility with utility-scale V2G programs.

In terms of power output, the 20–50 kW segment has emerged as the industry’s “sweet spot,” holding a 30–35% market share. This range offers the ideal balance of scalability, making it equally effective for premium residential installations, light commercial buildings, and urban fleet hubs.

Regional Powerhouses: The US and UK Lead the Charge

While the energy transition is global, certain regions are outpacing others due to aggressive federal incentives and advanced smart-grid mandates.

- United States (15.6% CAGR): Leading the growth curve through massive federal investment in fleet electrification and large-scale V2G pilot programs in states like California and New York.

- United Kingdom (15.4% CAGR): Reflecting a highly sophisticated smart grid infrastructure and rapid consumer adoption of V2H systems to combat rising electricity costs.

- China (15.2% CAGR): Driven by sheer scale and state-backed grid integration programs that mandate bidirectional compatibility for new infrastructure.

- India (14.5% CAGR): Emerging as a significant player through smart city initiatives and an urgent need for utility modernization to support its growing EV fleet.

The Analyst’s Perspective: A Strategic Outlook

“The V2X market is transitioning from a niche technology for early adopters into a fundamental component of the global energy transition,” says Shambhu Nath Jha, Principal Consultant at Fact.MR. “We are moving toward a ‘software-defined’ energy ecosystem. The value in 2036 won’t just be in the hardware of the charger, but in the AI-driven platforms that manage when and how that energy is traded between the car, the home, and the grid.”

Competitive Landscape & Market Dynamics

The competitive structure is evolving as automotive OEMs, power electronics specialists, and software giants converge. Manufacturers are currently prioritizing the reduction of “round-trip” energy loss and improving the interoperability of communication protocols like ISO 15118-20 and OCPP.

Key players currently shaping the strategic direction of the market include:

ABB Ltd., Wallbox NV, Delta Electronics, Enphase Energy, Inc., Schneider Electric SE, Siemens AG, Eaton Corporation, BorgWarner Inc., Fermata Energy, and Nuvve Holding Corp.

Browse Full Report – https://www.factmr.com/report/v2x-bidirectional-ev-charger-market

Conclusion: Navigating the $3 Billion Opportunity

While high upfront costs and regulatory fragmentation remain hurdles, the long-term commercial viability of V2X is undeniable. For investors and decision-makers, the opportunity lies in the convergence of the automotive and energy sectors. Those who can navigate the complexities of grid interconnection and deliver high-efficiency power electronics are set to dominate a market that is fundamentally rewiring how the world thinks about electricity.