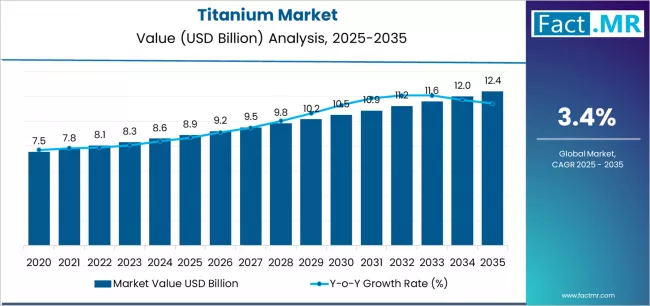

The global titanium market is set for steady expansion over the next decade, driven by rising demand from aerospace, medical, automotive, and industrial sectors, alongside the growing need for lightweight, high-strength, and corrosion-resistant materials. According to a new analysis, the market is projected to grow from USD 8,900.0 million in 2025 to USD 12,400.0 million by 2035, registering an absolute increase of USD 3,500.0 million over the forecast period. This growth reflects a CAGR of 3.4% from 2025 to 2035.

Titanium’s exceptional strength-to-weight ratio, biocompatibility, and resistance to extreme environments continue to position it as a critical material across high-performance and safety-critical applications worldwide.

Browse Full Report: https://www.factmr.com/report/titanium-market

Strategic Market Drivers

Aerospace & Defense Remain the Primary Growth Engine

Titanium is indispensable in aircraft structures, jet engines, landing gear, and military equipment due to its:

- High fatigue strength

- Excellent heat resistance

- Superior corrosion resistance

Rising commercial aircraft production, defense modernization programs, and increased air travel demand are significantly accelerating titanium consumption.

Medical & Healthcare Applications Gain Momentum

Titanium’s biocompatibility and non-toxic nature make it ideal for:

- Orthopedic implants

- Dental implants

- Surgical instruments

An aging global population and increasing adoption of advanced medical devices are driving sustained demand from the healthcare sector.

Automotive Lightweighting & EV Growth

Automakers are increasingly using titanium to:

- Reduce vehicle weight

- Improve fuel efficiency

- Enhance durability in performance vehicles

The rise of electric vehicles (EVs) and premium automotive segments is expanding titanium usage in exhaust systems, fasteners, and structural components.

Industrial & Chemical Processing Demand Expands

Titanium’s resistance to corrosion makes it essential in chemical processing plants, desalination facilities, and power generation systems, especially where exposure to harsh environments is common.

Regional Growth Highlights

North America: Aerospace & Defense Leadership

The U.S. dominates regional demand due to strong aerospace manufacturing, defense spending, and advanced medical device production. Titanium remains a strategic material for both commercial and military applications.

Europe: Sustainability & Advanced Manufacturing

Countries such as Germany, France, and the U.K. are witnessing growing titanium adoption driven by aerospace innovation, automotive lightweighting initiatives, and renewable energy infrastructure development.

East Asia: Manufacturing Scale & Industrial Expansion

China, Japan, and South Korea are key producers and consumers of titanium, supported by strong industrial manufacturing, electronics, and chemical processing industries.

Emerging Markets: Infrastructure & Healthcare Growth

India, Southeast Asia, Latin America, and the Middle East are experiencing rising titanium demand due to:

- Expanding healthcare infrastructure

- Industrial development

- Growing aerospace supply chains

Market Segmentation Insights

By Product Type

- Titanium Dioxide – Widely used in coatings, plastics, and pigments

- Titanium Metal – High demand in aerospace, medical, and industrial applications

By Grade

- Commercially Pure Titanium – Used in chemical processing and medical devices

- Titanium Alloys – Dominant in aerospace and high-performance applications

By End-Use Industry

- Aerospace & Defense – Largest market share

- Medical & Healthcare – Fast-growing segment

- Automotive – Increasing adoption for lightweighting

- Industrial Processing – Stable demand

- Consumer Goods – Premium applications

Challenges Impacting Market Growth

High Production & Processing Costs

Titanium extraction and processing are energy-intensive, making it more expensive than alternative metals such as aluminum or steel.

Complex Manufacturing Processes

Specialized equipment and expertise are required for titanium machining and fabrication, limiting adoption in cost-sensitive applications.

Supply Chain Constraints

Dependence on a limited number of titanium sponge producers and geopolitical factors can impact pricing and availability.

Competitive Landscape

The global titanium market is moderately consolidated, with manufacturers focusing on:

- Advanced alloy development

- Cost-efficient production technologies

- Recycling and sustainable titanium processing

Key Companies Profiled

- VSMPO-AVISMA Corporation

- ATI Inc.

- TIMET (Titanium Metals Corporation)

- Toho Titanium Co., Ltd.

- Baoji Titanium Industry

- Allegheny Technologies Incorporated

- Carpenter Technology Corporation

Recent Developments

- 2024: Increased investments in titanium recycling technologies to reduce raw material dependency

- 2023: Aerospace OEMs expand long-term titanium supply contracts amid rising aircraft production

- 2022: Medical device manufacturers accelerate titanium implant adoption due to durability and safety advantages

Future Outlook: Stable Growth Backed by High-Performance Applications

Over the next decade, the titanium market will continue to benefit from:

- Rising aircraft production rates

- Growth in medical implants and devices

- Automotive lightweighting trends

- Industrial expansion in harsh-environment applications

As industries increasingly prioritize durability, efficiency, and performance, titanium will remain a strategic material of choice, supporting consistent global market growth through 2035.