The “dumb machine” era in construction, mining, and agriculture is officially ending. According to the latest strategic outlook by Fact.MR, the global Off-Highway Vehicle (OHV) Telematics Market is undergoing a profound structural shift, with OEM factory-installed systems projected to hold a 64% market share by 2026.

Driven by institutional investments—most notably Goldman Sachs Alternatives’ recent majority acquisition of Trackunit—the industry is pivoting from simple GPS tracking to sophisticated, AI-driven SaaS platforms. With over 6.8 million active OEM units already in the field, telematics has moved from an “aftermarket luxury” to a “factory standard,” essential for warranty alignment, remote diagnostics, and lifecycle management.

Executive Market Quick-Stats (2026)

- Dominant Sales Channel: OEM Factory-Integrated (0% Share).

- Technology Leader: Cellular-based systems (0% Share) fueled by 5G rural expansion.

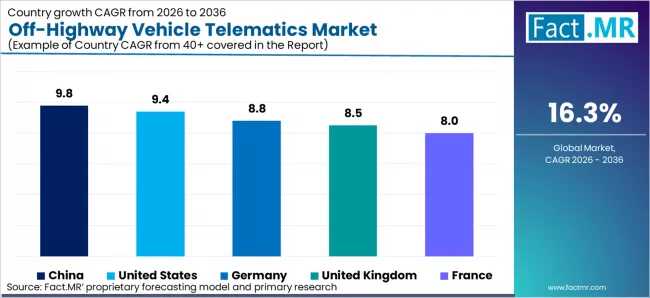

- Top Growth Engine: China (8% CAGR) and the United States (9.4% CAGR).

- Key Regulatory Catalyst: EU Machinery Regulation (effective Jan 2027) mandating remote safety monitoring.

- Institutional Milestone: Goldman Sachs/Hg investment in Trackunit (3 million+ connected assets).

Strategic Analysis: The Shift from Hardware to Data Intelligence

For equipment owners and rental fleets, the value proposition has shifted from “where is my machine?” to “how healthy is my engine?”

- The OEM Ecosystem: Major players like Caterpillar, John Deere, and Komatsu are now embedding connectivity as a baseline. The DEVELON MY platform launch in 2024 exemplifies this trend, turning real-time data into recurring service revenue while ensuring CAN bus compatibility that aftermarket retrofits often struggle to match.

- Connectivity Convergence: While cellular dominates due to lower costs and 5G expansion, the Trimble-Iridium partnership and ORBCOMM’s dual-mode deployments ensure that remote mining operations in Australia and Africa remain connected via satellite when cellular gaps persist.

- Predictive Maintenance: Hardware-only providers are losing ground to subscription-based platforms like Trackunit’s IrisX, which uses AI to process massive data volumes, significantly raising the bar for predictive accuracy and reducing unplanned downtime.

Regional Growth Outlook (2026–2036)

| Country | Projected CAGR | Primary Market Driver |

| China | 9.8% | 14th Five-Year Plan and rural 5G rollout for inland infrastructure. |

| United States | 9.4% | Infrastructure Investment & Jobs Act and advanced JDLink analytics. |

| Germany | 8.8% | Pre-compliance for EU 2023/1230; focus on AI-based efficiency. |

| United Kingdom | 8.5% | Digital asset mandates in the UK Construction Playbook. |

| India | Rising (High) | August 2025 Safety Omnibus Regulation mandating digital monitoring. |

Competitive Landscape: The Concentration of Platform Power

The market is rapidly concentrating at the platform layer. While hardware remains fragmented, a select group of SaaS providers—including Trackunit, ORBCOMM, and TomTom Telematics—is building high-moat ecosystems through deep OEM partnerships and open APIs (AEMP 2.0).

Strategic consolidation, such as Platform Science’s acquisition of Trimble’s telematics business in late 2024, indicates a market where scale and software integration depth are the ultimate differentiators. For decision-makers, long-term value is now driven by how well these platforms integrate with existing ERP and project management systems.

Browse Full Report –

https://www.factmr.com/report/off-highway-vehicle-telematics-market