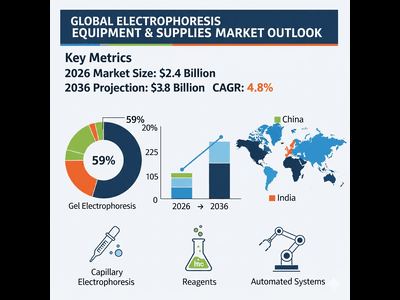

The global life sciences sector is undergoing a quiet but profound structural transformation. As personalized medicine moves from theory to clinical reality, the fundamental tools of molecular separation are seeing a massive resurgence in capital investment. According to the latest market intelligence from Fact.MR, the global Electrophoresis Equipment and Supplies Market, valued at $2.4 billion in 2026, is on a steady climb to reach $3.8 billion by 2036.

This projected $1.4 billion in absolute dollar growth is not merely a byproduct of increased lab activity. It represents a pivot toward high-resolution, automated systems capable of supporting the rigorous demands of modern drug development, forensic analysis, and disease diagnostics.

The Genomics Catalyst: Why Separation Science is Scaling

The maturity of the electrophoresis market has often led to its classification as a “legacy” sector. However, the explosion of proteomics and genomic sequencing has breathed new life into separation technology. Today’s research environments require more than just basic DNA bands; they demand reproducible, high-throughput data that can be integrated into digital bioinformatics pipelines.

Several key variables are driving this valuation:

- Expansion of Molecular Diagnostics: Clinical labs are increasingly utilizing electrophoresis for the early detection of chronic diseases and genetic disorders, moving the technology closer to the patient.

- The Biotech R&D Boom: With a global surge in biopharmaceutical manufacturing, electrophoresis has become critical for quality control and process validation of complex biologics.

- Integrated Workflow Adoption: By 2026, Gel Electrophoresis Systems are expected to maintain a dominant 59% market share, largely due to their reliability and the shift toward “all-in-one” kits that combine hardware, pre-cast gels, and proprietary buffers.

Technological Trends: From Manual Gels to Digital Resolution

While traditional gel electrophoresis remains the workhorse of the academic lab, the industry’s growth is increasingly concentrated in Capillary Electrophoresis (CE) and automated platforms. Decision-makers are prioritizing systems that minimize human error and regulatory risk. The “software-centric” lab is the new standard, where electrophoresis units are no longer standalone tools but integrated nodes in a laboratory information management system (LIMS).

Regional Dynamics: The Eastward Shift in Life Sciences

The geographical center of gravity for biotech investment is shifting rapidly. While the United States remains a massive consumer of high-end analytical supplies, the fastest growth rates are originating in the Asia-Pacific region.

- China (6.5% CAGR): Leading the global market in growth, fueled by aggressive state-backed pharmaceutical manufacturing and a burgeoning network of biotechnology hubs.

- India (6.1% CAGR): A major hotspot for clinical diagnostics and contract research organizations (CROs), where investments in life science infrastructure are hitting record highs.

- South Korea (5.6% CAGR): Driven by an advanced diagnostic sector and a highly sophisticated academic research ecosystem.

- United States (4.2% CAGR): Sustained by the continuous adoption of advanced genomic research in both commercial and ivy-league laboratories.

- Germany (3.8% CAGR): Underpinned by a resilient diagnostics market and strict adherence to high-quality research standards.

Competitive Landscape & Strategic Outlook

The electrophoresis market is characterized by a balance of established multinational giants and specialized reagent innovators. The primary competitive advantage is no longer just the hardware—it is the consumable ecosystem. Companies that provide proprietary, high-purity reagents and automated software updates are securing long-term recurring revenue streams.

Key players currently influencing the market’s trajectory include:

Thermo Fisher Scientific Inc., Bio-Rad Laboratories, Inc., Agilent Technologies, Inc., Danaher Corporation (Beckman Coulter), Merck KGaA, PerkinElmer Inc., Promega Corporation, GE Healthcare, QIAGEN N.V., and Lonza Group.

Analyst Perspective

“The electrophoresis market is transitioning from a standalone separation tool to a critical component of the digital diagnostic chain,” says Shambhu Nath Jha, Principal Consultant at Fact.MR. “Providers that can solve the ‘reproducibility crisis’ through automation and pre-certified consumables will capture the most significant market share. We are seeing a clear trend where research institutions are willing to pay a premium for systems that guarantee regulatory compliance and high-throughput efficiency.”

Browse Full Report – https://www.factmr.com/report/electrophoresis-equipment-and-supplies-market

Strategic Takeaways for Decision-Makers

For investors and lab executives, the 2026-2036 forecast period offers three distinct opportunities:

- Consumable Dominance: Focus on the “razor and blade” model, as reagents and pre-cast gels remain the highest-margin segment.

- Targeting the Asia-Pacific Corridor: China and India represent the most vital volume opportunities for equipment manufacturers over the next decade.

- Automation Integration: Investing in software-enabled platforms that reduce manual handling will be the primary driver for laboratory procurement departments.