The global Cytotoxic Chemotherapy Market is poised for robust growth through 2036 as the global cancer burden continues to rise and healthcare systems seek effective, broad-based treatment regimens. Cytotoxic chemotherapy remains a cornerstone of cancer treatment, particularly in settings where targeted therapies or immunotherapies may not be accessible or appropriate. These agents — designed to kill rapidly dividing cells — are widely used across a broad spectrum of malignancies including breast, lung, colorectal, hematologic, and gynecologic cancers.

Despite the evolution of precision oncology and targeted drugs, cytotoxic chemotherapy continues to play a vital role in curative, adjuvant, neoadjuvant, and palliative care strategies. Growth in the market is driven by increasing incidence of cancer globally due to aging populations and lifestyle risk factors, rising investments in cancer care infrastructure, expanding treatment access in emerging regions, and ongoing clinical innovation to improve efficacy and reduce side effects.

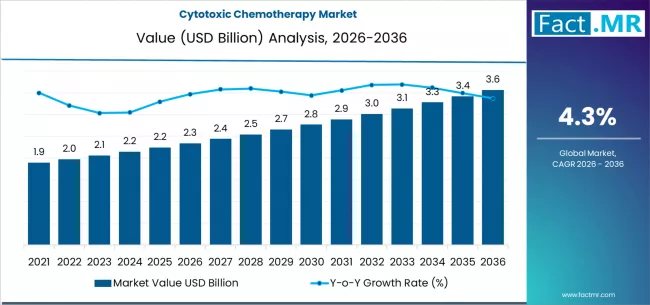

Market Outlook (2026–2036)

-

Estimated Market Value in 2026: USD 59.5 Billion

-

Projected Market Value in 2036: USD 112.3 Billion

-

Forecast CAGR (2026–2036): Approx. 7.1%

-

Leading Treatment Classes: Alkylating agents, antimetabolites, plant alkaloids

-

Primary End Users: Hospitals, Oncology Clinics, Cancer Treatment Centers

The expanding market reflects sustained reliance on cytotoxic agents as part of multi-modality cancer care and growing access to oncology services worldwide.

To access the complete data tables and in-depth insights, request a Discount On The Report here: https://www.factmr.com/connectus/sample?flag=S&rep_id=13503

Market Overview

Cytotoxic chemotherapy encompasses a range of pharmacologic classes that interfere with DNA synthesis, mitosis, or cellular proliferation. These include alkylating agents, antimetabolites, plant-derived compounds (such as taxanes and vinca alkaloids), and platinum-based compounds. Administered intravenously, orally, or through localized delivery approaches, cytotoxic agents are integral to both single-agent and combination regimens.

Combination therapy — using cytotoxic drugs with targeted therapies, hormone therapies, radiation, or immunotherapy — is common in clinical practice, aiming to enhance efficacy and overcome resistance. In many low- and middle-income countries, cytotoxic chemotherapy remains the most accessible and cost-effective option due to lower costs relative to newer targeted or cell-based therapies.

Key Market Drivers

1. Rising Global Cancer Incidence

Cancer remains a leading cause of mortality worldwide, with incidence expected to rise due to aging populations, lifestyle changes, and environmental risk factors. As diagnosis increases, so does demand for standard treatment options including cytotoxic chemotherapy.

2. Broad Applicability Across Cancer Types

Cytotoxic agents are used across a wide range of malignancies, from common solid tumors such as breast and colorectal cancers to hematologic cancers such as leukemia and lymphoma. Their applicability across oncology indications underpins sustained market demand.

3. Expansion of Oncology Infrastructure in Emerging Markets

Investment in cancer care infrastructure — including chemotherapy infusion centers, oncology training, and diagnostic capabilities — is expanding in regions such as Asia Pacific, Latin America, and the Middle East & Africa. This supports broader access to cytotoxic chemotherapy.

4. Integration With Multimodal Treatment Strategies

Cytotoxic chemotherapy remains a key component of combination treatment regimens. It is often used alongside surgery, radiation, targeted therapy, and immunotherapy to improve response rates, reduce tumor burden pre-surgery, and consolidate remission post-treatment.

5. Economic Considerations and Cost-Effectiveness

Compared with many targeted agents and immunotherapies, many cytotoxic drugs remain more cost-effective, especially in health systems with limited resources. This cost advantage supports continued uptake in both public and private healthcare markets.

Market Segmentation Insights

By Drug Class:

-

Alkylating Agents: Agents that form DNA crosslinks to inhibit replication.

-

Antimetabolites: Mimic normal substrates, disrupting DNA/RNA synthesis.

-

Plant Alkaloids and Terpenoids: Microtubule inhibitors that disrupt mitosis.

-

Platinum-Based Compounds: DNA-binding agents with broad efficacy.

-

Antitumor Antibiotics: Intercalate into DNA and generate cytotoxic free radicals.

-

Other Cytotoxic Agents: Miscellaneous compounds with antiproliferative activity.

By Route of Administration:

-

Intravenous Infusion: Most common delivery mode in oncology settings.

-

Oral Chemotherapy: Growing in convenience and outpatient care.

-

Localized Delivery Systems: Including targeted regional perfusion and implants.

By Indication:

-

Breast Cancer

-

Lung Cancer

-

Colorectal Cancer

-

Hematologic Malignancies

-

Gynecologic Cancers

-

**Other Solid Tumors

By End User:

-

Hospitals and Oncology Clinics

-

Specialized Cancer Treatment Centers

-

Ambulatory Treatment Facilities

-

Home Healthcare Settings (Oral Therapies)

Regional Demand Dynamics

North America is expected to retain a dominant share of the market driven by high cancer incidence, strong healthcare infrastructure, extensive clinical research activity, and access to advanced supportive care that enhances chemotherapy tolerability.

Europe represents a sizeable regional market supported by well-established oncology treatment protocols, comprehensive reimbursement systems, and widespread adoption of combination therapies.

Asia Pacific is projected to exhibit the fastest growth, with increasing cancer cases, expanding healthcare access, rising public and private sector investment in oncology care, and improving diagnostic rates in populous markets such as China, India, and Southeast Asia.

Emerging demand is also evident in Latin America and Middle East & Africa, where expanding healthcare delivery and oncology service investments are broadening access to standard cancer therapies.

Competitive Landscape

The cytotoxic chemotherapy market is moderately competitive, with participation from global pharmaceutical companies, specialty oncology drug manufacturers, and generics producers. Many well-established brands exist alongside a growing portfolio of generic and biosimilar cytotoxic agents that improve access and affordability.

Key strategic priorities among market players include portfolio expansion, development of novel formulations that improve safety or delivery convenience, and expanded distribution networks. Companies also focus on clinical support programs, patient assistance initiatives, and collaborations with oncology centers to optimize regimen adoption and outcomes.

Future Outlook

The Cytotoxic Chemotherapy Market is expected to sustain steady growth through 2036 as rising cancer incidence, expanding treatment infrastructure, and integration with multimodal therapeutic strategies drive demand. While targeted therapies and immunotherapies continue to gain prominence, cytotoxic chemotherapy remains foundational in many treatment protocols due to its broad applicability, clinical utility, and cost effectiveness.

Innovation in supportive care, delivery approaches, and formulation improvements — including oral agents and reduced-toxicity regimens — will further support market expansion. Additionally, increasing access in emerging economies and ongoing efforts to improve cancer care equity globally will strengthen adoption.

As the oncology landscape evolves, cytotoxic chemotherapy will continue to play a central role in global cancer management, supporting enhanced survival, quality of life, and treatment outcomes for patients worldwide.

Browse Full Report: https://www.factmr.com/report/cytotoxic-chemotherapy-market