The global Data Center SSD Market is experiencing significant expansion as hyperscale cloud providers, enterprise data centers, financial institutions, telecommunications companies, and AI infrastructure operators accelerate investments in high-performance storage solutions. The rapid growth of artificial intelligence (AI), machine learning (ML), big data analytics, cloud computing, edge computing, and high-performance computing (HPC) workloads is fueling demand for enterprise-grade solid-state drives (SSDs) that deliver superior speed, reliability, scalability, and energy efficiency.

Get detailed market forecasts, competitive benchmarking, and pricing trends:

According to Fact.MR’s latest market intelligence, the Data Center SSD Market is projected to witness robust growth throughout the forecast period, supported by increasing digital transformation initiatives, rising enterprise data generation, expanding cloud infrastructure, and continuous advancements in NAND flash technologies. Organizations are replacing traditional hard disk drives (HDDs) with enterprise SSDs to reduce latency, improve workload performance, lower operational costs, and optimize energy consumption across modern data center environments.

Market Overview and Growth Outlook

Data center SSDs are high-performance storage devices specifically engineered for enterprise applications requiring exceptional reliability, endurance, low latency, and high input/output operations per second (IOPS). These storage solutions support mission-critical workloads including virtualization, databases, cloud storage, AI model training, enterprise resource planning (ERP), content delivery, financial transactions, and real-time analytics.

Advancements in PCIe Gen5, NVMe (Non-Volatile Memory Express), QLC and TLC NAND flash memory, computational storage, storage-class memory integration, and intelligent storage management are transforming enterprise storage architectures.

The continued migration toward software-defined infrastructure, cloud-native applications, containerized workloads, and AI-driven computing environments is expected to sustain long-term demand for next-generation enterprise SSD solutions.

Key Market Growth Drivers

- Rapid expansion of hyperscale cloud data centers

- Increasing adoption of artificial intelligence and machine learning

- Growing enterprise demand for low-latency storage

- Rising investments in digital transformation

- Expansion of edge computing infrastructure

- Advancements in NVMe and PCIe storage technologies

- Increasing replacement of enterprise HDDs with SSDs

Key Market Projections and Strategic Insights

The data center SSD market is evolving from conventional enterprise storage toward intelligent, software-defined storage ecosystems capable of supporting increasingly data-intensive AI and cloud workloads.

Manufacturers are introducing higher-capacity SSDs utilizing advanced NAND architectures while improving endurance, energy efficiency, thermal performance, and workload optimization. Computational storage technologies and AI-driven storage management platforms are enabling organizations to process data closer to storage devices, reducing latency and improving overall infrastructure efficiency.

The growing adoption of generative AI, large language models (LLMs), and GPU-accelerated computing is expected to significantly increase enterprise demand for ultra-high-performance storage capable of sustaining intensive read/write operations.

“Enterprise storage is undergoing a fundamental transformation as AI, cloud computing, and hyperscale infrastructure redefine performance expectations. Data center SSDs equipped with next-generation NVMe architectures and advanced flash technologies will remain essential for enabling scalable, low-latency digital infrastructure,” says a Fact.MR analyst.

Competitive Landscape and Market Share Analysis

The market comprises semiconductor manufacturers, NAND flash producers, enterprise storage vendors, cloud infrastructure providers, and integrated hardware companies competing through innovation, manufacturing scale, storage density, endurance, and performance optimization.

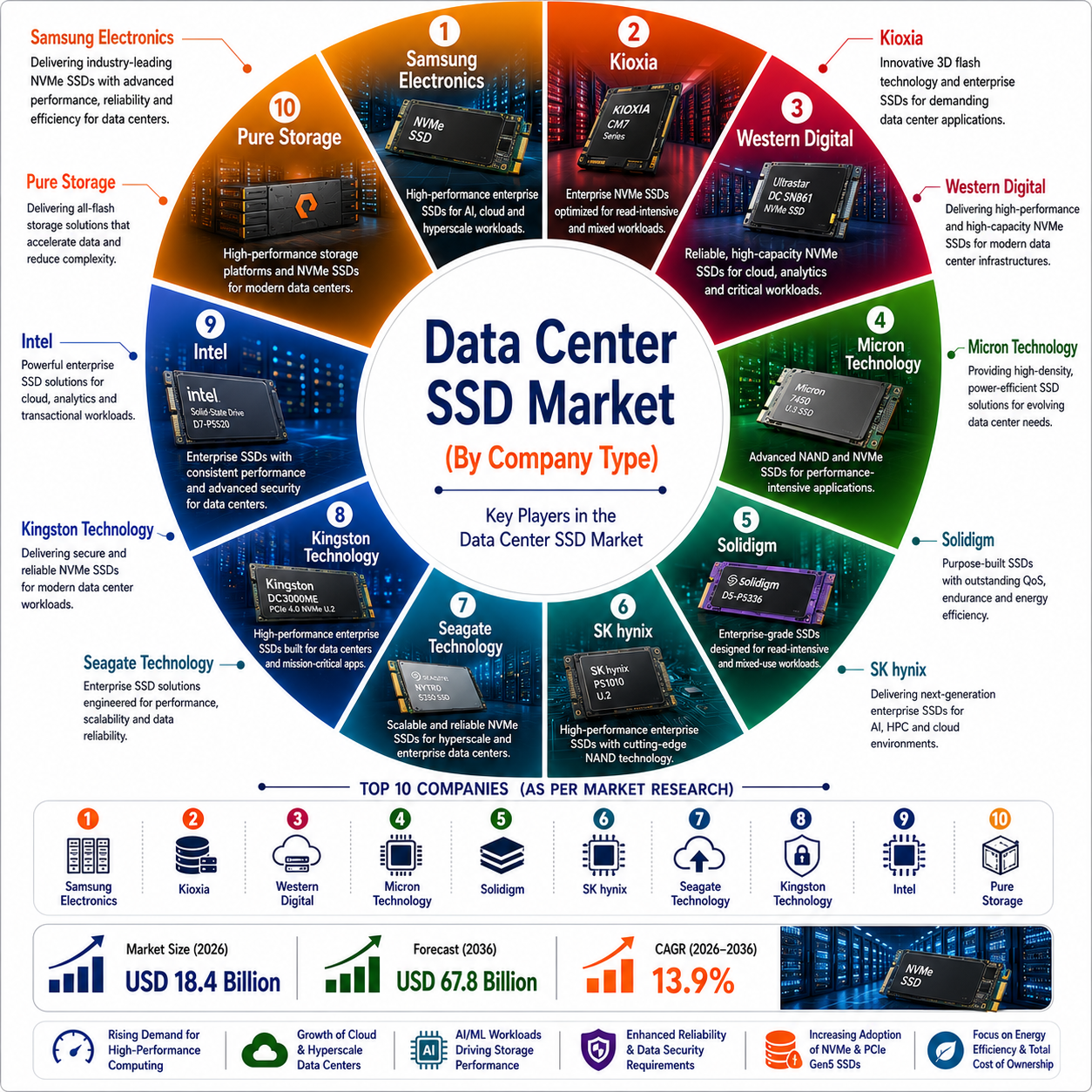

Key Companies Active in the Market

- Samsung Electronics Co., Ltd.

- Solidigm (SK hynix)

- Micron Technology, Inc.

- Kioxia Corporation

- Western Digital Corporation

- Seagate Technology Holdings plc

- Kingston Technology Corporation

- Intel Corporation (legacy enterprise SSD portfolio)

- Dell Technologies Inc.

- Hewlett Packard Enterprise (HPE)

- Lenovo Group Limited

- NetApp, Inc.

- Pure Storage, Inc.

- Huawei Technologies Co., Ltd.

- Toshiba Electronic Devices & Storage Corporation

Competitive Strategies Shaping the Market

Leading companies are investing in:

- PCIe Gen5 NVMe SSDs

- High-capacity QLC enterprise storage

- AI-optimized storage platforms

- Computational storage architectures

- Energy-efficient flash memory

- Software-defined storage integration

- Advanced controller technologies

Strategic partnerships among cloud providers, semiconductor manufacturers, enterprise server vendors, and hyperscale operators continue accelerating deployment of next-generation storage infrastructure.

Production Economy Analysis

Manufacturing of data center SSDs is concentrated in regions with advanced semiconductor fabrication, NAND flash production, and electronics manufacturing capabilities.

Major Production Hubs

- South Korea – NAND flash manufacturing and semiconductor innovation

- Japan – flash memory technologies and semiconductor materials

- Taiwan – semiconductor fabrication and controller development

- China – electronics manufacturing and storage assembly

- United States – enterprise storage innovation and cloud infrastructure technologies

South Korea remains the global leader in enterprise NAND flash production, while Japan and Taiwan continue driving technological innovation across advanced memory and semiconductor manufacturing.

Consumption Economy Analysis

Demand for data center SSDs is increasing across regions investing heavily in cloud infrastructure, AI computing, and enterprise digital transformation.

Leading Consumption Markets

- United States

- China

- Japan

- Germany

- United Kingdom

- South Korea

- India

North America leads global consumption due to extensive hyperscale cloud deployments and AI infrastructure investments. Asia-Pacific continues experiencing rapid growth driven by expanding data center construction, while Europe benefits from increasing enterprise cloud adoption and digital economy initiatives.

Supply Chain and Value Chain Insights

The data center SSD value chain includes raw material suppliers, semiconductor foundries, NAND flash manufacturers, SSD controller developers, firmware providers, storage system manufacturers, server OEMs, cloud operators, distributors, and enterprise customers.

Core Value Chain Components

- Semiconductor wafers

- NAND flash memory

- SSD controllers

- Firmware development

- Storage module assembly

- Enterprise server integration

- Cloud infrastructure deployment

- Data center operations

Industry participants continue strengthening supply chain resilience through geographic diversification, advanced semiconductor packaging, strategic sourcing, and long-term manufacturing partnerships.

Strategic Procurement Analysis

Enterprise buyers increasingly prioritize storage solutions capable of supporting mission-critical digital infrastructure with long operational lifecycles.

Key Procurement Priorities

- Storage performance

- Endurance and reliability

- NVMe compatibility

- Power efficiency

- Scalability

- Data security

- Lifecycle management

- Total cost of ownership

Hyperscale cloud providers and enterprise IT organizations increasingly seek storage platforms optimized for AI workloads, virtualization, and software-defined infrastructure.

Distribution and Commercialization Trends

Data center SSDs are commercialized through OEM partnerships, enterprise storage vendors, cloud infrastructure providers, and specialized IT distribution networks.

Key Distribution Trends

- Direct enterprise sales

- OEM server integration

- Cloud infrastructure partnerships

- IT distributors

- Systems integrators

- Value-added resellers

- Enterprise storage solution providers

Subscription-based infrastructure services and integrated storage-as-a-service (STaaS) offerings continue reshaping enterprise procurement strategies.

Country Opportunity Assessment

United States

The United States remains the largest market owing to rapid hyperscale data center expansion, AI infrastructure investments, and strong enterprise cloud adoption.

China

China continues expanding opportunities through large-scale digital infrastructure projects, cloud computing growth, and enterprise modernization initiatives.

South Korea

South Korea maintains strategic importance through global NAND flash manufacturing leadership and continued semiconductor innovation.

Japan

Japan benefits from advanced semiconductor technologies, enterprise IT modernization, and expanding high-performance computing investments.

India

India is emerging as a high-growth market supported by increasing cloud adoption, digital economy expansion, and new hyperscale data center developments.

Technology and Innovation Outlook

Rapid innovation continues transforming enterprise storage technologies.

Emerging Technology Trends

- PCIe Gen5 NVMe SSDs

- QLC NAND flash

- Computational storage

- AI-powered storage optimization

- Storage-class memory integration

- CXL-enabled storage architectures

- Energy-efficient flash technologies

- Software-defined storage

- Intelligent data lifecycle management

Future innovation will increasingly focus on ultra-high-capacity enterprise SSDs, AI-native storage architectures, computational memory technologies, next-generation NAND processes, liquid-cooled storage systems, and autonomous storage management platforms capable of supporting exascale computing environments.

Investment Outlook

The Data Center SSD Market presents substantial investment opportunities across:

- Enterprise flash storage

- AI infrastructure

- Cloud computing

- Semiconductor manufacturing

- Data center modernization

- High-performance computing

- Enterprise storage software

- Digital infrastructure

Organizations capable of delivering high-capacity, AI-optimized, energy-efficient, and highly reliable enterprise SSD solutions are expected to strengthen their competitive position as global enterprises continue expanding digital infrastructure to support AI, cloud, and data-intensive computing workloads.

About Fact.MR

Fact.MR is a global market research and consulting firm, trusted by Fortune 500 companies and emerging businesses for reliable insights and strategic intelligence. With a presence across the U.S., UK, India, and Dubai, we deliver data-driven research and tailored consulting solutions across 30+ industries and 1,000+ markets. Backed by deep expertise and advanced analytics, Fact.MR helps organizations uncover opportunities, reduce risks, and make informed decisions for sustainable growth.

– Contact Us –

11140 Rockville Pike, Suite 400, Rockville,

MD 20852, United States

Tel: +1 (628) 251-1583 | sales@factmr.com