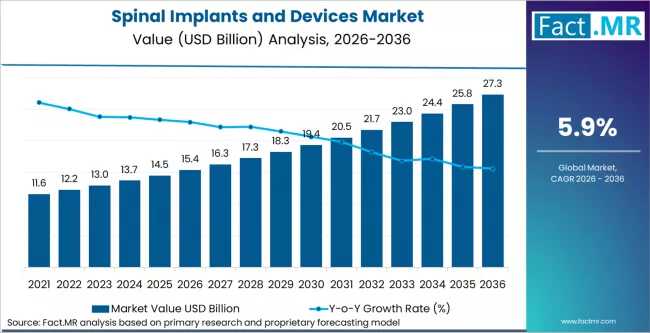

The global spinal implants and devices market is projected to be valued at USD 15.4 billion in 2026 and is expected to climb to USD 26.9 billion by 2036. This steady expansion, represented by a CAGR of 5.9%, is fueled by the rising prevalence of spinal disorders, an aging global population, and a shifting clinical preference toward advanced surgical treatments and minimally invasive procedures.

Spinal Implants and Devices Market Outlook

Market size 2026? USD 15.4 billion

Market size 2036? USD 26.9 billion

CAGR? 5.9% (2026-2036)

Leading technology segment and share? Spinal fusion and fixation technologies (67.0% share)

Leading surgery type and share? Open surgery (58.8% share)

Key growth regions? North America, Europe, and Asia-Pacific (with India and China as fastest-growing)

Top companies? Medtronic plc, Johnson & Johnson, VB Spine, LLC, NuVasive, Inc., Zimmer Biomet Holdings, Inc., Globus Medical, Inc., Alphatec Spine, Inc., Orthofix Medical Inc., RTI Surgical Holdings, Inc., and Ulrich GmbH & Co. KG.

Market Momentum (YoY Path)

The market’s trajectory is defined by a consistent upward trend in valuation. Starting at an estimated USD 15.4 billion in 2026, the market is anticipated to reach USD 17.2 billion in 2028, growing further to USD 19.3 billion by 2030. By 2031, the value is expected to hit USD 20.5 billion, followed by USD 23.0 billion in 2033, and finally achieving the forecast peak of USD 26.9 billion in 2036.

Why the Market is Growing

Growth is primarily anchored in the increasing incidence of degenerative disc disease, scoliosis, and spinal fractures. As the global demographic ages, the demand for spinal care solutions has intensified. Furthermore, the rising adoption of minimally invasive surgery (MIS) and technological breakthroughs in durable implant materials and surgical techniques are expanding the patient pool. In emerging markets, broader access to healthcare is playing a pivotal role in fueling demand for advanced spinal instrumentation.

Segment Spotlight

1) Technology Type

Spinal fusion and fixation technologies are the market’s primary engine, projected to capture a 67% market share by 2026. These technologies are critical for treating complex conditions by stabilizing the spine and promoting bone growth. Their high efficacy in providing long-term stabilization for chronic pain and injury makes them a staple in clinical practice.

2) Surgery Type

Open surgery remains the dominant approach, expected to account for 58.8% of the market share in 2026. While minimally invasive techniques are rising, open surgery is still preferred for complex spinal corrections where direct visualization and extensive access are required, such as in severe fractures or multi-level fusions.

3) Key Demographics & End Use

The market is increasingly influenced by the aging population and the move toward specialized healthcare settings. Hospitals and surgical centers are the primary end users, driven by the necessity for advanced imaging and instrumentation required to perform both open and minimally invasive spinal procedures effectively.

Drivers, Opportunities, Trends, Challenges

Drivers: The primary growth catalyst is the surge in spinal disorders and the aging population. Technological advancements, such as the development of refined surgical techniques and more durable implant materials, are significantly increasing the adoption of spinal fusion and fixation.

Opportunities: Emerging markets in South Asia and East Asia present substantial expansion opportunities due to improving healthcare infrastructure. Additionally, the development of biologic-enhanced devices and motion-preserving technologies offers a high-value growth path for manufacturers.

Trends: There is a clear shift toward digital integration in the operating room. Recent developments, such as the FDA clearance of platforms that integrate planning, navigation, and robotics, highlight a trend where surgery is becoming more precise and data-driven.

Challenges: Market growth may be hindered by the high cost associated with spinal implants and complex surgical procedures. Furthermore, a shortage of highly skilled surgeons capable of performing advanced spinal operations remains a constraint in several regions.

Country Growth Outlook (CAGR)

Country CAGR (2026-2036)

India 8.0%

China 7.8%

Japan 7.3%

USA 6.8%

UAE 6.7%

Germany 6.5%

Brazil 6.2%

Browse Full Report : https://www.factmr.com/report/spinal-implants-and-devices-market

Competitive Landscape

The Spinal Implants and Devices Market is highly competitive, led by industry giants like Medtronic plc, Johnson & Johnson, and Zimmer Biomet, who maintain extensive portfolios across cervical and lumbar solutions. Innovators like NuVasive, Inc. and Globus Medical, Inc. focus on minimally invasive technologies, while niche players like Alphatec Spine and VB Spine, LLC target specialized tech segments. Competition is currently centered on improving patient outcomes, advancing material science, and reducing surgical times.