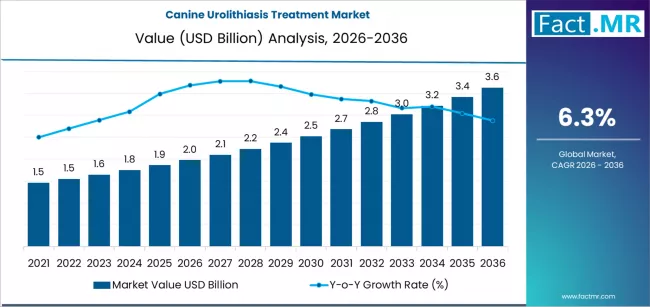

The global canine urolithiasis treatment market is entering a phase of significant clinical expansion, with its valuation projected to grow from USD 540 million in 2026 to USD 1.1 billion by 2036. According to a specialized industry analysis by Fact.MR, the market is set to expand at a 7.5% compound annual growth rate (CAGR), driven by a surge in diagnostic precision and a fundamental shift toward therapeutic diets and minimally invasive interventions.

Urolithiasis, or the formation of bladder and kidney stones, is one of the most common lower urinary tract diseases in dogs, particularly in predisposed breeds like Dalmatians, Schnauzers, and Bulldogs. For veterinary professionals and investors, the market is pivoting away from traditional invasive cystotomies toward high-tech solutions such as laser lithotripsy and precision-formulated “dissolution” diets that address the underlying metabolic imbalances of stone formation.

Summary Table: Canine Urolithiasis Treatment Outlook

| Metric | Details |

| Market Value (2026E) | USD 540 Million |

| Forecast Value (2036F) | USD 1.1 Billion |

| Projected CAGR (2026-2036) | 7.5% |

| Leading Category | Prescription Diets (45.2% Share) |

| Primary End-User | Veterinary Hospitals (58%+ Share) |

| Highest Growth Market | India (10.2% CAGR) |

Request for Sample Report | Customize Report – https://www.factmr.com/connectus/sample?flag=S&rep_id=13597

Core Market Dynamics: Answering the Strategic ‘Who,’ ‘What,’ and ‘Why’

Canine urolithiasis treatment encompasses a multi-modal approach including specialized prescription diets, pharmacological agents (such as urinary acidifiers), and surgical or interventional procedures.

-

Who is leading the sector? Industry titans including Mars Petcare (Royal Canin), Hill’s Pet Nutrition, Nestlé Purina, Boehringer Ingelheim, and Zoetis are at the forefront, leveraging clinical research to develop diets that specifically target struvite and calcium oxalate crystal formation.

-

What is the dominant treatment category? Prescription Diets command a significant 45.2% market share. These therapeutic formulations are engineered to manage urinary pH and mineral concentration, often serving as the primary tool for both the dissolution of existing stones and the prevention of recurrence.

-

Where is growth most accelerated? India is emerging as the fastest-growing market with a 10.2% CAGR, fueled by a burgeoning middle class and an explosion in pet health awareness. China follows with a 9.5% CAGR, supported by a rapid increase in advanced specialty veterinary hospitals.

-

Why is the technology shifting? The industry is moving toward Minimally Invasive Interventions.4 There is a notable surge in demand for Laser Lithotripsy and Extracorporeal Shock Wave Lithotripsy (ESWL), which currently hold a 38.5% share of the procedure segment, as they offer significantly faster recovery times and lower complication rates than open surgery.

Sector Insights: Veterinary Clinics and Specialty Centers Lead Demand

The Veterinary Hospitals and Specialty Clinics segment remains the primary end-user, projected to hold over 58% of the market share by 2026. This is largely due to the requirement for advanced diagnostic imaging, such as ultrasonography and digital radiography, to accurately identify stone composition—a critical step in determining the correct therapeutic path.

“The management of urolithiasis has evolved from a ‘wait and see’ approach to a highly proactive, data-driven discipline,” the analysis states. “We are seeing a major trend toward ‘Personalized Renal Nutrition.’ By utilizing stone analysis labs, veterinarians can now prescribe specific diets that eliminate the precise mineral precursors causing the stones. This preventative model is transforming urolithiasis from a chronic recurrence issue into a manageable long-term health plan.”

Key Market Trends and Strategic Outlook

1. Optimization through “Smart” Diagnostic Imaging

One of the most significant absolute dollar opportunities lies in the integration of AI-driven Diagnostic Software. Modern imaging tools can now assist veterinarians in predicting stone composition based on radiopacity and morphology, allowing for the immediate initiation of dissolution diets without waiting for laboratory results.5

2. The Rise of “Multi-Benefit” Therapeutic Diets

Manufacturers are increasingly developing diets that address comorbidities. For example, diets that manage both urinary health and weight management are gaining traction, as obesity remains a major risk factor for urolithiasis in several canine breeds.

3. Regulatory and Breed-Specific Tailwinds

In the United States (7.2% CAGR) and Germany (6.8% CAGR), growth is supported by a robust pet insurance market. As insurance coverage for “advanced procedures” increases, more pet owners are opting for high-cost, non-invasive lithotripsy over traditional surgery, providing a stable revenue stream for specialty equipment manufacturers.

Investment Perspective: A High-Value Veterinary Pillar

The canine urolithiasis treatment market represents a robust opportunity for both the medical device and specialty pet food sectors. As pet owners increasingly view their dogs as family members and prioritize “longevity-focused” care, the demand for high-performance health solutions—capable of managing a complex and painful condition with minimal trauma—is expected to remain a primary growth engine through 2036.

Browse Full Report: https://www.factmr.com/report/canine-urolithiasis-treatment-market