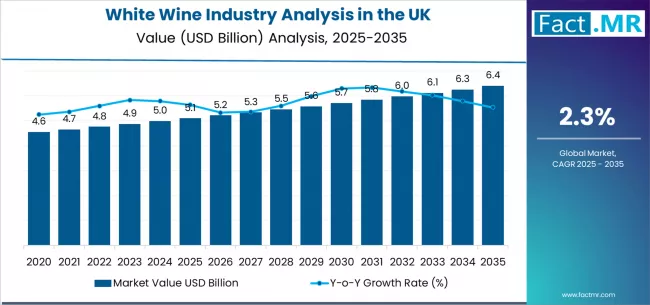

The UK white wine market is estimated to be worth USD 5.1 billion in 2025. Over the decade to 2035, this market is forecast to grow to about USD 6.5 billion, implying a compound annual growth rate (CAGR) of roughly 2.3% for the period 2025–2035. This represents an absolute increase of about USD 1.4 billion over the forecast period.

In short — the UK white wine segment is not expected to boom dramatically, but rather to grow steadily and moderately over the next decade, supported by consumer demand and retail market structure.

Key Segments & Market Structure

By Variety (Grape/Wine Type):

-

The leading variety among white wines is Chardonnay, capturing about 26.3% of total white-wine demand in 2025.

-

Other notable categories include Sauvignon Blanc, Pinot Grigio, and a grouping of “Others.”

By Sales Channel:

-

The dominant channel for white-wine sales is off-trade (retail outlets, supermarkets, specialist wine merchants, etc.), which accounts for approximately 76.8% of white-wine demand in 2025.

-

The remaining share is with on-trade channels (restaurants, bars, hospitality venues).

By Region (within the UK):

-

Demand is spread across all UK nations — England, Scotland, Wales, and Northern Ireland.

-

England leads in terms of volume and growth potential, driven by larger consumer base, retail density, and premium-wine demand concentration.

Thus the white-wine market in the UK is structured around a few major varieties, heavily supported by retail channels, with greatest demand concentration in England.

To access the complete data tables and in-depth insights, request a Discount On The Report here: https://www.factmr.com/connectus/sample?flag=S&rep_id=12031

Drivers of Growth

Several factors underpin the modest but steady growth forecast:

-

Rising interest in premium and varietal wines. There’s growing consumer preference for recognized grape varieties and better-quality wines rather than generic table wines.

-

Retail-led distribution and accessibility. The dominance of off-trade channels makes white wine widely available at various price points, encouraging repeat purchasing.

-

Variety and quality awareness. As wine culture deepens in the UK, more consumers and retailers seek variety and reliable quality.

-

Stable import-dominated supply and strong distribution networks. The UK remains heavily reliant on imported wine, ensuring consistent supply from major wine-producing regions worldwide.

These drivers together reinforce a stable base demand and modest growth potential for white wine in the UK.

Challenges & Headwinds

However, growth faces some structural headwinds:

-

Strong dependence on imports. Domestic wine production in the UK is minimal relative to overall demand, leading to vulnerability to global supply dynamics, currency fluctuations, and import costs.

-

Competition from alternative beverages and shifting consumer preferences. Shifts toward beers, spirits, low-alcohol drinks, or non-alcoholic beverages can reduce wine consumption volumes.

-

Price sensitivity and cost pressures. Import, distribution, and retail markups can push up bottle prices; economic uncertainty may reduce spending on wine.

-

Mature market with modest growth. With a relatively small projected CAGR (~2.3%), competition among brands, varieties, and price segments remains intense.

Strategic Implications

For stakeholders — producers, distributors, retailers, or investors — the following strategic takeaways emerge:

-

Focus on varietal wines with strong brand positioning such as Chardonnay, Sauvignon Blanc, and Pinot Grigio.

-

Strengthen presence in off-trade retail channels, given their dominant share.

-

Build supply-chain resilience, especially considering the UK’s dependence on imported wines.

-

Offer multiple price-quality tiers to capture both premium and value-driven segments.

-

Use marketing and educational initiatives to increase consumer awareness and loyalty.

Outlook to 2035

By 2035, the UK white wine market is expected to grow steadily from USD 5.1 billion in 2025 to USD 6.5 billion, supported by varietal demand, accessible retail channels, and evolving consumer interest in quality wines.

Chardonnay is expected to remain the leading variety, while Sauvignon Blanc, Pinot Grigio, and other varietals continue gaining attention. Off-trade channels will maintain dominance, while on-trade venues will support brand exposure and sampling.

For industry stakeholders who invest in quality, branding, and efficient supply chains, the UK white wine market offers stable, long-term opportunity and manageable growth potential through 2035.

Browse Full Report: https://www.factmr.com/report/united-kingdom-white-wine-industry-analysis