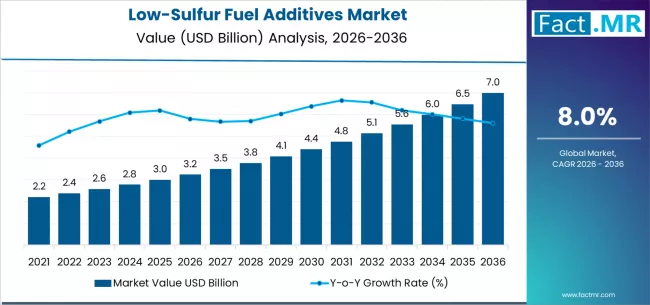

The low-sulfur fuel additives market is experiencing rapid transformation, fueled by stringent global regulations on sulfur content in fuels and increasing demand for cleaner energy solutions. These additives play a critical role in improving fuel performance while minimizing environmental impact. By enhancing lubricity, preventing injector fouling, and stabilizing ultra-low sulfur fuels, these products are crucial for maintaining engine efficiency and compliance with modern emission standards.

Market Overview

Low-sulfur fuel additives are essential for diesel, marine, aviation, and industrial fuel applications. The adoption of ultra-low sulfur fuels reduces harmful sulfur oxide emissions but also diminishes natural lubricity, potentially causing wear in fuel injection systems. Additives such as lubricity improvers, cetane enhancers, cold flow additives, and detergents address these challenges, ensuring optimal engine performance and durability.

Diesel fuels represent the largest consumption base due to their widespread use in transportation, power generation, and industrial machinery. On-road transportation remains the leading application segment, driven by fleet operators’ need for reliability, reduced maintenance costs, and adherence to strict emission regulations.

Technological Insights

Lubricity improvers dominate the additive type segment, addressing the critical performance gap left by sulfur removal during refining. These additives, often based on fatty acid esters or amides, prevent excessive wear in fuel injectors and pumps. Other technologies focus on enhancing cold flow properties, improving combustion efficiency, and controlling deposits, making additive formulations increasingly multifunctional.

Innovation is also focusing on hybrid fuels and renewable diesel blends, where additives must stabilize diverse fuel compositions and maintain compatibility with modern exhaust after-treatment systems like diesel particulate filters and selective catalytic reduction devices.

Regional Insights

North America and Europe are key markets due to advanced infrastructure, stringent environmental regulations, and established diesel and marine fleets. Asia-Pacific, particularly India and China, is emerging as a high-growth region. India’s implementation of Bharat Stage VI standards and China’s strict port emission regulations are driving demand for high-performance additives, ensuring fuel system protection and regulatory compliance.

The USA continues to maintain demand due to its large diesel fleet and integration of renewable fuel blends, while Germany and Japan focus on emission compliance and performance optimization of modern engines.

Market Drivers

The primary growth driver is the global tightening of sulfur regulations across marine, on-road, and off-road fuels. Policies such as IMO 2020 for marine fuels and Euro/BS-VI standards for road fuels have created widespread adoption of additive-treated fuels. Additionally, the growing emphasis on extending the operational life of internal combustion engines in a transitioning energy landscape reinforces the demand for performance-enhancing additives.

Multifunctional additive packages are gaining popularity, combining lubricity improvement, detergency, corrosion inhibition, and demulsification properties. These innovations address complex fuel challenges, including cold weather performance for biodiesel blends and long-term storage stability in marine fuels.

Market Restraints

Despite strong growth, the market faces challenges. Electrification of road transport, the rise of alternative marine fuels, and price volatility in base fuels may limit future demand. Furthermore, formulating additives for diverse fuel blends containing biofuels or synthetic fuels presents technical and cost challenges for manufacturers.

Emerging Trends

Emerging trends in the low-sulfur fuel additives market include digital monitoring for optimized dosing, formulations tailored to renewable fuel blends, and enhanced focus on multifunctional additives. Manufacturers are increasingly offering solutions that combine fuel efficiency, engine protection, and emission compliance in a single package. The use of direct injection system analysis to personalize additive treatment for specific fleets is also gaining traction, ensuring operational efficiency while reducing environmental impact.

Competitive Landscape

Key market players include BASF SE, Chevron Oronite, Afton Chemical, Infineum International, and Lubrizol Corporation. These companies are investing in R&D to develop advanced additive solutions that cater to ultra-low sulfur fuels and renewable fuel blends. Strategic partnerships and technological advancements are helping manufacturers address the growing complexities of global fuel standards while delivering high-performance additive systems.

Conclusion

The low-sulfur fuel additives market is pivotal for supporting the global shift toward cleaner, more efficient fuel solutions. By addressing performance deficits in ultra-low sulfur fuels, these additives ensure engine longevity, emission compliance, and operational efficiency across diesel, marine, and industrial applications. Ongoing innovation in multifunctional additives, renewable fuel compatibility, and digital monitoring is poised to further strengthen the market, making these products indispensable in a decarbonizing world.

Browse Full Report – https://www.factmr.com/report/low-sulfur-fuel-additives-market