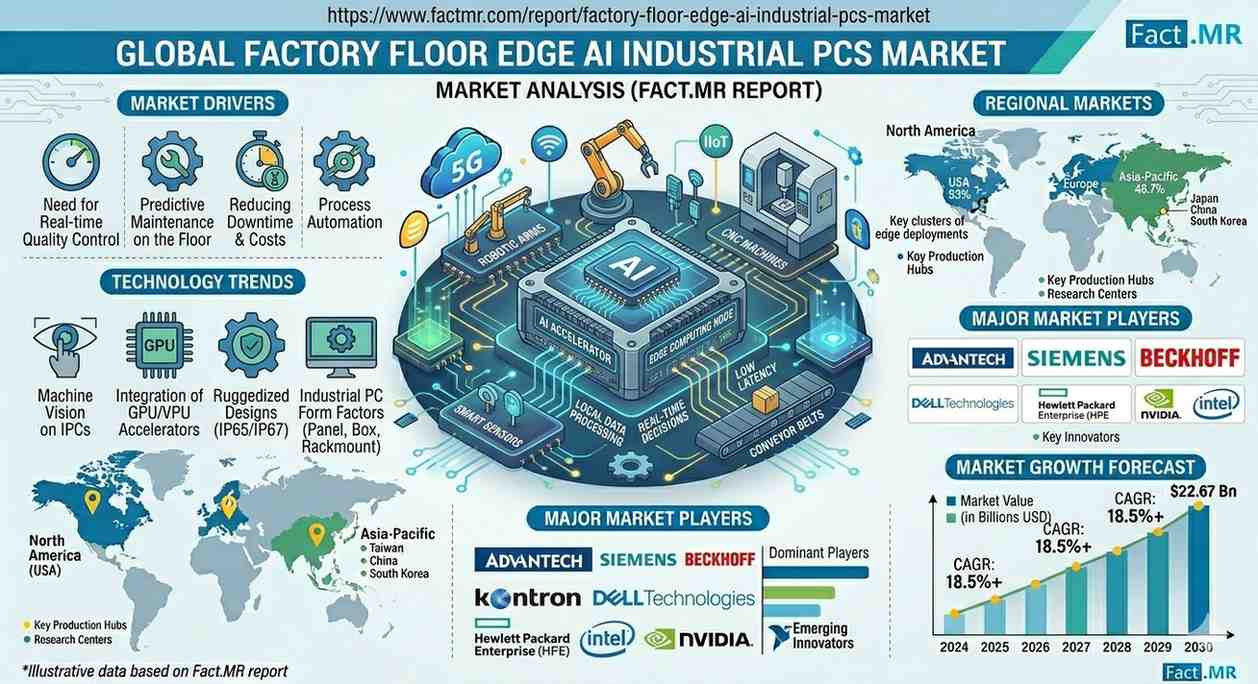

The global Factory Floor Edge AI Industrial PCs (IPCs) market is undergoing a seismic shift, projected to grow from USD 0.68 billion in 2026 to USD 1.37 billion by 2036. This trajectory represents a steady 7.3% CAGR, driven by the urgent industrial requirement for real-time, autonomous decision-making at the “Extreme Edge” of manufacturing.

As factories transition from cloud-dependent architectures to decentralized models, Edge AI IPCs have emerged as the foundational hardware for hosting complex inference models directly on the shop floor. By eliminating the latency and bandwidth bottlenecks of remote data transmission, these ruggedized platforms are enabling the next generation of robotic control and zero-defect manufacturing.

Market Snapshot: 2026–2036

- 2026 Valuation: USD 0.68 Billion

- 2036 Projection: USD 1.37 Billion

- Growth Rate:3% CAGR

- Dominant Form Factor: Box IPC (54% Market Share)

- Primary Use Case: Machine Vision (29% Market Share)

Strategic Segment Analysis

Machine Vision: The Eyes of the Edge

Machine vision remains the primary driver of edge processing, commanding a 29% market share. The integration of high-resolution cameras with local Convolutional Neural Networks (CNNs) allows for instantaneous defect detection and assembly verification, which is essential for high-speed production lines where cloud latency is unacceptable.

Box IPCs: The Modular Workhorse

With a 54% market share, Box IPCs are the preferred form factor for industrial leaders. Their modularity allows for the integration of dedicated AI acceleration chips (GPUs/VPUs) while maintaining the ruggedness required for harsh environments. This flexibility makes them ideal for “brownfield” retrofitting in existing factories.

Automotive: Leading Vertical Integration

The automotive sector remains the dominant end-user, utilizing Edge AI IPCs for real-time weld inspection, robotic vision, and predictive maintenance. The industry’s pursuit of “zero-defect” manufacturing makes low-latency edge intelligence a non-negotiable requirement.

Global Growth Engines & Regional Outlook

The market is characterized by strong regional initiatives aimed at manufacturing sovereignty and digital transformation.

| Country | Projected CAGR (2026-2036) | Primary Growth Catalyst |

| China | 7.5% | “Made in China 2026” initiatives and a massive electronics manufacturing base. |

| Germany | 7.0% | Industrie 4.0 leadership and high-precision automotive robotics. |

| USA | 7.0% | Reshoring of semiconductor fabs and focus on OT cybersecurity/data sovereignty. |

| South Korea | 6.8% | Dominance in precision electronics and cleanroom-compatible AI systems. |

Competitive Landscape & Supply Chain

The market is defined by a convergence of traditional Industrial Automation (OT) and high-performance computing (IT).

- Supply Chain Dynamics: Specialized IPC manufacturers (Advantech, Kontron) supply ruggedized hardware to Tier-1 Automation providers (Siemens, Rockwell) and System Integrators, who then deploy validated AI stacks to end-users like BMW, Samsung, and Boeing.

- Key Players: Advantech, Siemens, Beckhoff, Rockwell Automation, Kontron, and Mitsubishi Electric.

- Pricing Trends: While hardware costs are stabilizing, premium pricing is shifting toward “AI-Ready” bundles that include pre-validated software containers and dedicated NPU (Neural Processing Unit) acceleration.

Actionable Insights for Decision-Makers

Investment Opportunities

- AI-at-the-Hardware-Level: Significant ROI is found in IPCs with integrated AI accelerators that handle multiple concurrent neural streams without increasing thermal footprints.

- Standardized Stacks: There is a growing secondary market for pre-validated, containerized AI applications that simplify the “IT/OT convergence” for mid-sized manufacturers.

Market Risks

- Complexity Gap: The primary restraint remains the shortage of specialized talent capable of maintaining complex Edge AI hardware and software stacks.

- Initial CapEx: High upfront costs for high-performance edge nodes can deter adoption in price-sensitive “General Manufacturing” sectors.

Future Outlook

By 2030, the “Autonomous Factory” will move beyond simple inspection to Closed-Loop Edge Control, where IPCs not only detect defects but autonomously adjust PLC (Programmable Logic Controller) parameters in real-time to prevent them. Investors should prioritize companies offering “Cybersecurity by Design” as edge nodes become primary targets for industrial cyber-espionage.

Browse Full Report –

https://www.factmr.com/report/factory-floor-edge-ai-industrial-pcs-market