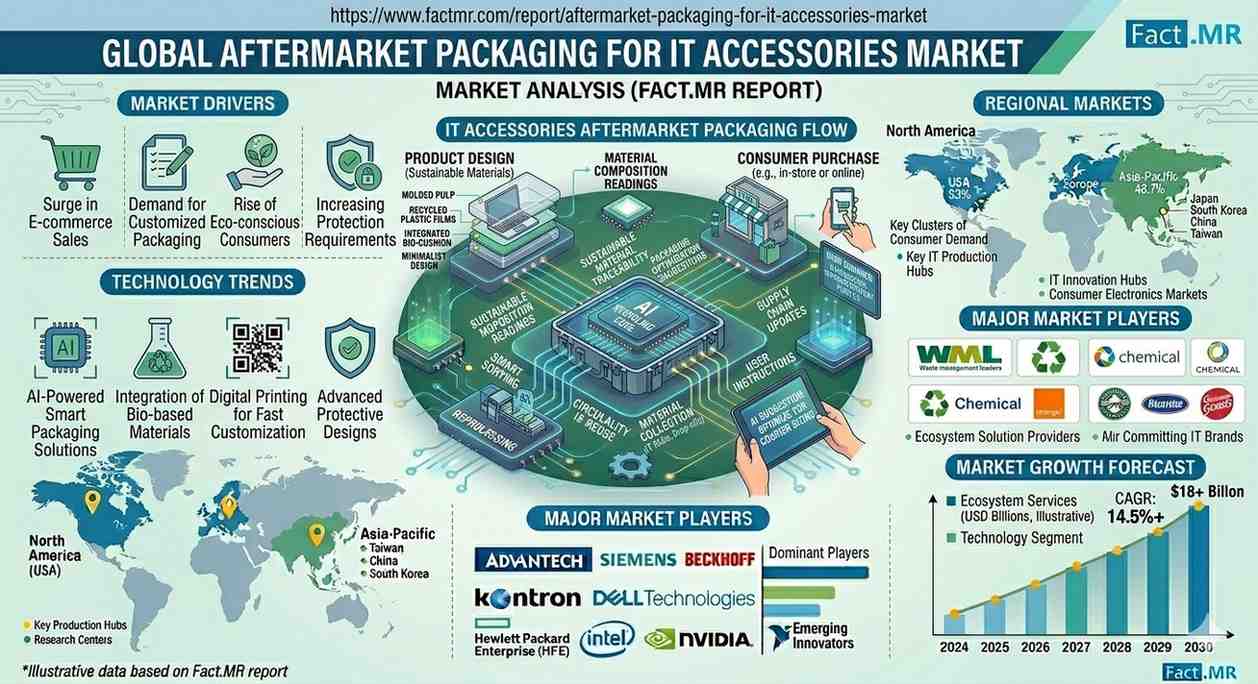

The global market for aftermarket packaging for IT accessories is entering a period of steady expansion, projected to grow from USD 451.5 million in 2026 to USD 763.9 million by 2036. This growth, representing a compound annual growth rate (CAGR) of 5.4%, is being driven by the rapid intensification of repair-and-replace cycles and the global surge in e-commerce fulfillment for IT peripherals.

As consumers and enterprises extend the lifespans of their hardware, the demand for protective, right-sized packaging for individual components—such as chargers, adapters, cables, and sensitive internal spares—has become a critical link in the global IT supply chain.

Executive Market Summary (2026–2036)

- 2026 Valuation: USD 451.5 Million

- 2036 Projection: USD 763.9 Million

- CAGR:4%

- Dominant Channel: E-commerce Replacement Parts (48.3% Market Share)

- Primary Packaging Type: Mailers and Small Boxes (35.7% Market Share)

- Leading Protection Feature: Drop or Impact Protection (42.0% Market Share)

Strategic Segment Insights

E-commerce: The Aftermarket Powerhouse

The E-commerce Replacement Parts channel dominates the landscape with a 48.3% share. Unlike bulk primary shipments to retailers, the aftermarket requires packaging optimized for “single-unit” parcel networks. This shift has necessitated a move away from heavy outer cartons toward high-performance, lightweight Mailers and Small Boxes (35.7% share) that minimize dimensional weight while maximizing structural integrity.

Critical Protection: Engineering for the “Last Mile”

Because aftermarket accessories often travel individually through high-touch courier networks, Drop and Impact Protection is the leading design priority, accounting for 42.0% of market focus. Advanced solutions now integrate ESD (Electrostatic Discharge) protection and Moisture Barriers to safeguard sensitive circuitry in adapters and internal components during unpredictable transit conditions.

Regional Outlook: Asia-Pacific Outpaces Global Average

While the U.S. and Europe remain stable markets, the fastest growth is concentrated in regions with rapidly expanding IT service ecosystems and high e-commerce penetration.

| Country | Projected CAGR (2026-2036) | Primary Growth Driver |

| India | 7.1% | Exploding demand for mobile/laptop spares in fragmented online markets. |

| Vietnam | 6.5% | Rising domestic distribution and export of replacement IT components. |

| Indonesia | 6.2% | High growth in walk-in service centers and retail spare part visibility. |

| China | 5.4% | Massive turnover of accessories through standardized distributor channels. |

| Brazil | 5.0% | Growth in B2B IT Asset Disposition (ITAD) and secondary markets. |

| USA | 3.3% | Mature, automated fulfillment systems focusing on material efficiency. |

Competitive Landscape & Supply Chain

The competitive frontier is defined by the ability to offer “Aftermarket-Ready” formats—standardized, low-waste, and highly protective packaging that can be integrated into automated fulfillment lines.

- Market Leaders: Sealed Air, Berry Global, and Ranpak are leading in the development of engineered foam and paper-based cushioning.

- Integrated Solutions: Companies like Smurfit Kappa, WestRock, and International Paper are leveraging their global footprint to supply corrugated and folding carton solutions for service centers and retail spares.

- Technical Specialists: NEFAB and Amcor focus on specialized ESD and moisture-barrier materials for high-value or sensitive ITAD (IT Asset Disposition) flows.

Actionable Intelligence for Decision-Makers

Investment Opportunities

- Eco-Friendly Inserts: There is significant ROI in replacing plastic-based protective inserts with Recycled Plastics or Engineered Paper Foam to meet tightening regional environmental regulations, particularly in Europe.

- Tamper-Evident Logic: With the rise of high-value “open-box” and refurbished accessories, Tamper-Evident features are becoming a premium requirement to reduce fraudulent returns and maintain brand integrity.

Market Risks

- Shipping Bulk vs. Protection: The primary challenge remains the “protection-to-weight” ratio. Excessive packaging increases shipping costs, while insufficient protection leads to high return rates in the fragile aftermarket segment.

- Standardization Hurdles: Aftermarket packaging must accommodate a vast variety of accessory shapes and sizes, which can limit the economies of scale typically found in primary production packaging.

Future Outlook: Circularity in the Aftermarket

By 2036, the market will move toward “Circular Aftermarket Systems” where packaging is designed for both the outbound journey of a new spare part and the return journey of the defective component (Reverse Logistics). Suppliers that can provide durable, re-sealable packaging optimized for this dual-purpose lifecycle will capture significant market share in the growing IT circular economy.

Browse Full Report –

https://www.factmr.com/report/aftermarket-packaging-for-it-accessories-market