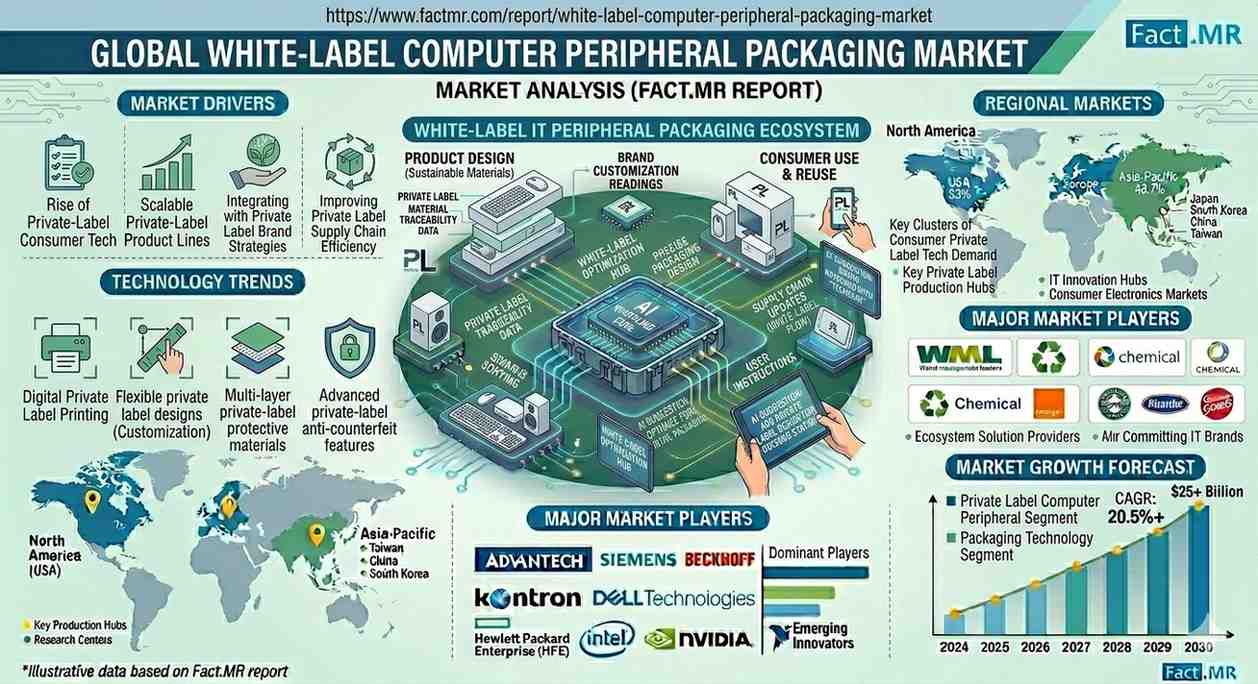

According to Fact.MR’s latest analysis, the global white-label computer peripheral packaging market is valued at USD 535.5 million in 2026 and is projected to reach USD 566.0 million in 2027, ultimately expanding to USD 932.2 million by 2036. The market is set to grow at a CAGR of 5.7% (2026–2036), creating an incremental opportunity of USD 396.7 million over the forecast period.

This market is undergoing a structural transformation driven by the rapid proliferation of OEM private-label peripherals, increasing reliance on third-party fulfillment networks, and the need for standardized, cost-efficient packaging solutions. As global electronics supply chains become more agile, packaging is evolving from a branding tool into a scalable operational asset.

Quick Stats

- Market Size (2026): USD 535.5 million

- Market Size (2027): USD 566.0 million

- Forecast Value (2036): USD 932.2 million

- CAGR (2026–2036): 5.7%

- Incremental Opportunity: USD 396.7 million

- Leading Segment: Folding Cartons (48.3%)

- Leading Customer Type: OEM Private Label (44.1%)

- Leading Region: Asia-Pacific (India, Vietnam, Indonesia, China)

- Key Players: Mondi, Berry Global, Avery Dennison, Smurfit Kappa, Amcor, WestRock, Sealed Air

Executive Insight for Decision Makers

The market is shifting toward high-volume, low-cost, and rapidly customizable packaging ecosystems. OEMs, retailers, and distributors are prioritizing packaging formats that enable fast brand switching and cross-market scalability.

Strategic Imperatives:

- Invest in standardized packaging platforms with flexible print zones

- Align packaging with automated fulfillment systems and e-commerce logistics

- Prioritize sustainable materials to meet regulatory and retailer expectations

Risk of Inaction:

Companies failing to adapt risk longer turnaround times, higher costs, and lost private-label contracts in a market increasingly driven by speed and efficiency.

Market Dynamics

Key Growth Drivers

- Rapid expansion of OEM and retailer private-label peripherals

- Growth in e-commerce and 3PL fulfillment ecosystems

- Demand for cost-efficient, scalable packaging formats

- Rising adoption of paperboard-based sustainable packaging

Key Restraints

- High pressure on cost optimization limiting design innovation

- Need to balance protection, compliance, and low-cost production

- Limited differentiation due to neutral branding requirements

Emerging Trends

- Standardized packaging structures with customizable print zones

- Increased use of recyclable paperboard and hybrid materials

- Integration with automated warehousing and fulfillment systems

- Growth of minimalist, compliance-focused packaging designs

Segment Analysis

- Leading Segment: Folding cartons hold 48.3% share, driven by cost efficiency, print flexibility, and scalability

- Fastest-Growing Segment: Mailers and bags, fueled by e-commerce shipments

Breakdown:

- Packaging Type: Folding cartons, mailers, blister packs, rigid boxes

- Customer Type: OEM private label (44.1%), retailer private label, 3PL brands

- Material: Paperboard (56.7%), plastics, recycled plastics, hybrid structures

Strategic Importance:

Folding cartons remain the backbone of the market, enabling high-volume production with minimal structural redesign, while mailers support last-mile delivery efficiency.

Supply Chain Analysis (Critical Insight)

Value Chain Structure

- Raw Material Suppliers:

Paperboard producers, plastic resin manufacturers, recycled material suppliers - Packaging Manufacturers:

Convert raw materials into cartons, mailers, and protective formats - Distributors & Integrators:

Supply packaging to OEMs, retailers, and fulfillment centers - End-Users:

- OEM peripheral manufacturers (keyboards, mice, cables)

- Retail private-label brands

- E-commerce and 3PL fulfillment providers

Who Supplies Whom

- Paper mills supply paperboard to converters like Mondi and International Paper

- Packaging firms deliver standardized formats to OEMs and retailers

- 3PL providers integrate packaging into automated fulfillment workflows

Insight:

The supply chain prioritizes speed, repeatability, and global scalability, with minimal customization at structural levels.

Pricing Trends

- Commodity-driven pricing dominates folding cartons and mailers

- Premium pricing applies to rigid boxes and specialty protective packaging

Key Influencers

- Raw material costs (paperboard, plastics)

- Volume contracts with OEMs

- Sustainability certifications and compliance

- Logistics and fulfillment integration costs

Margin Insight:

Margins remain moderate but stable, with profitability driven by scale and operational efficiency rather than product differentiation.

Regional Analysis

Top Growth Countries (CAGR)

- India: 7.4%

- Vietnam: 6.8%

- Indonesia: 6.4%

- China: 5.7%

- Mexico: 5.3%

Regional Insights

- Asia-Pacific: Manufacturing hub with fastest growth due to OEM production

- North America: Mature market driven by replacement demand and fulfillment efficiency

- Europe: Focus on sustainability and standardized packaging

- Emerging Markets: High growth driven by private-label expansion and retail penetration

Developed vs Emerging Markets:

- Developed markets emphasize compliance and efficiency

- Emerging markets prioritize cost scalability and production growth

Competitive Landscape

- Market Structure: Moderately fragmented with global and regional players

Key Companies

- Mondi

- Berry Global

- Avery Dennison

- Ranpak

- NEFAB

- Smurfit Kappa

- WestRock

- International Paper

- Amcor

- Sealed Air

Competitive Strategies

- Standardized packaging platforms

- Global sourcing and supply chain optimization

- Sustainable material innovation

- Fast turnaround and fulfillment integration

Strategic Takeaways

For Manufacturers

- Focus on high-volume standardized production

- Invest in sustainable and recyclable materials

For Investors

- Target Asia-Pacific growth hubs and OEM-driven ecosystems

- Back companies with strong logistics integration capabilities

For Marketers & Distributors

- Emphasize speed, scalability, and compliance over branding

- Align offerings with private-label and e-commerce trends

Future Outlook

The market is expected to evolve toward automation-driven packaging ecosystems, where AI-enabled supply chains and smart logistics dictate packaging requirements. Sustainability will play a central role, with increasing adoption of recyclable and lightweight materials.

Long-term opportunities lie in:

- Integration with smart warehouses and robotics

- Development of modular packaging systems

- Expansion of cross-border private-label supply chains

Conclusion

The global white-label computer peripheral packaging market is transitioning into a high-efficiency, scale-driven industry where speed, cost control, and operational flexibility outweigh traditional branding priorities. Companies that align with these dynamics will unlock significant growth opportunities, while those that fail to adapt risk losing relevance in a rapidly evolving private-label ecosystem.

Why This Market Matters

As private-label electronics reshape global retail and e-commerce, packaging becomes a strategic enabler of scalability and efficiency. This market sits at the intersection of manufacturing, logistics, and retail transformation, making it critical for stakeholders aiming to capture value in the next phase of global trade evolution.

Browse Full Report –

https://www.factmr.com/report/white-label-computer-peripheral-packaging-market