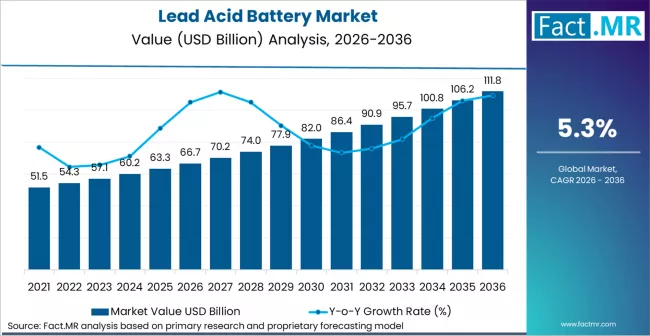

According to Fact.MR’s latest analysis, the global lead-acid battery market is valued at approximately USD 58 billion in 2025, projected to reach USD 60.5 billion in 2026, and expand to USD 85 billion by 2035. The market is expected to grow at a CAGR of 3.5%, creating an incremental opportunity of USD 27 billion.

Japan remains a key contributor within Asia, with a projected CAGR of 3.8%, driven by strong automotive manufacturing, demand for reliable backup power systems, and advanced battery recycling infrastructure. The market is evolving with increased focus on hybrid vehicles, energy storage systems, and sustainability practices.

Quick Stats (Japan Focus)

- Market Size (2025): ~USD 5.6 Billion

- Market Size (2026): ~USD 5.8 Billion

- Forecast Value (2035): ~USD 8.4 Billion

- CAGR (2025–2035): 3.8%

- Incremental Opportunity: ~USD 2.8 Billion

- Leading Segment: SLI Batteries (Automotive)

- Leading Country (Asia): Japan (technology-driven segment)

- Key Players: GS Yuasa, Panasonic, EnerSys, Exide Industries, East Penn Manufacturing

Executive Insight for Decision Makers

Japan’s lead-acid battery market is transitioning from traditional automotive dependency to diversified energy storage applications.

- Manufacturers must invest in enhanced battery efficiency and lifecycle improvements

- OEMs should integrate lead-acid batteries with hybrid and backup systems

- Investors should focus on companies with strong recycling and circular economy models

Risk of inaction: Losing relevance amid rapid growth of lithium-ion alternatives and stricter environmental standards.

Market Dynamics

Key Growth Drivers

- Stable demand from automotive SLI (starting, lighting, ignition) batteries

- Growth in UPS and backup power systems

- Japan’s leadership in battery recycling technologies

- Rising use in renewable energy storage (secondary role)

Key Restraints

- Competition from lithium-ion batteries

- Environmental concerns related to lead usage

- Limited innovation compared to next-gen battery technologies

Emerging Trends

- Development of advanced lead-carbon batteries

- Integration with hybrid energy storage systems

- Increased focus on closed-loop recycling systems

- Use in telecom and data center backup power

Segment Analysis

- Leading Segment: SLI Batteries (~60% share in Japan)

- Fastest-Growing Segment: Industrial batteries (UPS, telecom, energy storage)

Breakdown

- Product Type: SLI, stationary, motive batteries

- Application: Automotive, industrial, renewable energy, telecom

- End-use: Automotive OEMs, utilities, telecom operators, industrial users

Strategic Importance:

SLI batteries dominate due to Japan’s strong automotive base, while industrial applications are gaining traction due to data infrastructure expansion.

Supply Chain Analysis (Critical Insight)

Value Chain Structure

- Raw Material Suppliers

- Lead mining and recycling companies

- Electrolyte and separator material providers

- Manufacturers / Producers

- Battery manufacturers and assemblers

- Distributors

- Automotive suppliers, industrial equipment distributors

- End-Users

- Automotive OEMs, telecom companies, utilities, consumers

Who Supplies Whom

- Lead suppliers (primary & recycled) → Battery manufacturers → OEMs/distributors → End-users

Insight:

Japan’s supply chain is highly recycling-driven, with over 95% of lead reused, making it one of the most circular battery ecosystems globally.

Pricing Trends

- Market follows a commodity-linked pricing model

- Key Influencing Factors:

- Global lead prices

- Demand from automotive and industrial sectors

- Recycling efficiency and cost optimization

Margin Insight:

- Stable but moderate margins in automotive batteries

- Higher margins in industrial and specialty applications

Regional Analysis

Top 5 Countries by Growth

- Japan (CAGR ~3.8%) – Technology and recycling leadership

- China (CAGR ~4.2%) – Volume-driven demand

- India (CAGR ~4.5%) – Rapid automotive growth

- USA (CAGR ~3.4%) – Replacement demand

- Germany (CAGR ~3.3%) – Industrial applications

Insights

- Japan: High-tech, efficiency-driven market

- Asia-Pacific: Fastest-growing region

- Western markets: Replacement-driven demand

Developed vs Emerging

- Developed markets: Sustainability and efficiency focus

- Emerging markets: Volume and cost-driven demand

Competitive Landscape

- Market is moderately consolidated in Japan

- Key players:

- GS Yuasa

- Panasonic

- EnerSys

- Exide Industries

- East Penn Manufacturing

- Amara Raja Energy

- Clarios

Strategies

- Investment in advanced battery technologies

- Expansion of recycling capabilities

- Partnerships with automotive OEMs

- Focus on industrial and energy storage applications

Strategic Takeaways

For Manufacturers

- Enhance battery performance and lifecycle

- Invest in recycling and sustainability initiatives

For Investors

- Focus on companies with strong circular economy models

- Target firms expanding into industrial energy storage

For Marketers / Distributors

- Highlight reliability and cost-effectiveness

- Target automotive and industrial sectors

Future Outlook

Japan’s lead-acid battery market will continue evolving as a reliable, cost-effective energy storage solution.

- Growth in hybrid energy systems

- Increasing demand for backup power infrastructure

- Continued leadership in battery recycling technologies

Long-term Opportunity:

Positioning lead-acid batteries as a complementary solution to lithium-ion in hybrid energy ecosystems

Conclusion

The lead-acid battery market in Japan is transitioning toward a balanced model of traditional demand and modern energy applications.

Stakeholders who leverage recycling efficiency, industrial demand, and hybrid integration strategies will maintain a competitive edge in a changing energy landscape.

Why This Market Matters

- Essential for automotive reliability and backup power

- Key contributor to circular economy in batteries

- Supports energy resilience and infrastructure stability