As global air mobility evolves with advanced aircraft design, sustainability goals, and digital integration, the aerostructure equipment market is emerging as a critical enabler of the modern aerospace manufacturing ecosystem. These systems form the backbone of aircraft assembly and structural integrity — ensuring precision, safety, and efficiency in every stage of production.

With growing investments in commercial aviation, defense modernization, and next-generation aircraft platforms, demand for highly automated and flexible aerostructure manufacturing equipment is gaining remarkable momentum. The market’s evolution is being defined by smarter production lines, robotics, and composite material technologies that collectively enhance the overall lifecycle performance of aircraft.

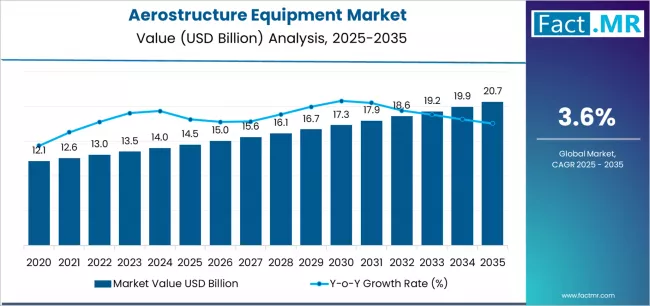

Market Overview

Aerostructure equipment comprises specialized machinery and systems used to manufacture and assemble the structural components of aircraft — such as wings, fuselage sections, and empennages. These tools are vital to maintain dimensional accuracy, reduce weight, and improve aerodynamic performance while optimizing production throughput.

The aerospace industry is undergoing a transition from conventional metal fabrication to advanced composites, driving the adoption of equipment capable of handling carbon fiber and hybrid materials. Manufacturers are focusing on precision assembly solutions, digital monitoring, and automated fastening systems that improve productivity and consistency across production lines.

Additionally, the shift toward electric and hybrid aircraft is prompting a re-evaluation of traditional aerostructure manufacturing methods. The result is a surge in demand for modular, reconfigurable, and AI-assisted equipment capable of meeting the unique structural demands of next-generation airframes.

Key Market Drivers

Several pivotal forces are shaping the trajectory of the aerostructure equipment market:

- Rising Aircraft Production: The growing global fleet and replacement of aging aircraft are fueling the need for efficient manufacturing solutions and scalable assembly systems.

- Adoption of Advanced Materials: Increasing use of composites and lightweight alloys is driving demand for adaptable equipment designed for new material handling techniques.

- Automation and Digitalization: Integration of robotics, AI, and digital twins in manufacturing lines enhances precision and reduces operational costs.

- Focus on Sustainability: Aerospace OEMs are investing in energy-efficient equipment and waste-reduction technologies to meet sustainability goals.

- Defense Modernization Programs: Global defense initiatives and new fighter aircraft projects are expanding the use of high-precision aerostructure equipment across military platforms.

These drivers collectively underscore a strategic market shift from traditional assembly operations toward smart, data-driven, and modular manufacturing ecosystems.

Regional Insights

North America remains at the forefront of the aerostructure equipment market, driven by strong aerospace manufacturing bases, continuous R&D investment, and collaborations between major OEMs and suppliers. The region’s emphasis on advanced production systems, coupled with digital factory initiatives, reinforces its leadership position.

Europe follows closely, supported by the presence of global aircraft manufacturers and a robust focus on sustainable manufacturing. Automation and the integration of green technologies in aerostructure production are prominent themes across European facilities.

Asia-Pacific is emerging as a high-growth region, propelled by rapid industrialization, expanding airline fleets, and government initiatives promoting local aircraft manufacturing. The growing participation of regional suppliers in the global aerospace supply chain is boosting demand for advanced aerostructure assembly tools and systems.

The Middle East and Latin America are gradually expanding their aerospace manufacturing footprints, especially through joint ventures and technology transfer programs. This regional diversification is widening the overall market base for aerostructure equipment globally.

Key Trends and Future Outlook

The aerostructure equipment market is undergoing a transformation shaped by innovation, automation, and the digital enterprise model. Some of the most notable trends include:

- Rise of Automated Fastening Systems: Automated drilling and riveting machines are becoming integral to improving accuracy, reducing cycle time, and minimizing human error in aircraft assembly.

- Digital Twin Integration: Virtual modeling of aerostructure production processes enables real-time monitoring, predictive maintenance, and performance optimization.

- Collaborative Robotics: Cobots are enhancing safety and flexibility in assembly operations, supporting human-machine collaboration on complex tasks.

- Composite Material Handling Systems: Specialized equipment is being developed to manage temperature-sensitive, lightweight composite materials with high precision.

- Additive Manufacturing Influence: Integration of 3D printing for tooling and component prototyping is accelerating design flexibility and reducing development costs.

These technological shifts highlight the industry’s move toward a fully connected, intelligent manufacturing environment that enhances quality assurance, efficiency, and scalability.

Applications and End-Use Outlook

Aerostructure equipment finds extensive application across both commercial and military aviation segments. In commercial aircraft manufacturing, the demand for high production rates and lightweight structures is driving the need for automated assembly lines and advanced joining technologies.

The defense sector continues to invest in precision assembly equipment to support the production of high-performance aircraft, drones, and rotary-wing platforms. Meanwhile, maintenance, repair, and overhaul (MRO) facilities are also adopting adaptable equipment systems to extend the lifecycle and performance of existing fleets.

OEMs, tier-1 suppliers, and component manufacturers are increasingly focusing on integrated solutions that combine mechanical systems with digital analytics and machine learning for optimized production management.

Challenges and Strategic Outlook

Despite its promising growth potential, the aerostructure equipment market faces challenges such as high capital investment requirements, complex integration processes, and the need for skilled labor to manage advanced manufacturing systems. However, collaborative R&D initiatives between equipment suppliers, aerospace OEMs, and digital technology providers are helping to overcome these barriers.

As aerospace companies continue to prioritize cost efficiency, supply chain resilience, and sustainable operations, investments in aerostructure equipment are expected to accelerate. Industry players are focusing on strategic partnerships, automation upgrades, and flexible manufacturing layouts to stay ahead in a highly competitive environment.

Conclusion

The aerostructure equipment market is at the heart of the aerospace industry’s modernization journey. As the world moves toward advanced air mobility, autonomous systems, and greener aviation, the demand for innovative, automated, and digitally enabled aerostructure manufacturing solutions will continue to rise.

For stakeholders across the aerospace value chain, understanding market trends and aligning investments with the next wave of technological advancement will be key to capturing future opportunities and ensuring long-term competitiveness in this rapidly evolving sector.

Browse Full Report – https://www.factmr.com/report/4069/aerostructure-equipment-market