The global vocational trucks market is set for consistent expansion over the next decade, supported by rising infrastructure development, urbanization, and increasing demand for application-specific commercial vehicles. According to an analysis by Fact.MR, the market is valued at USD 94.0 billion in 2025 and is projected to reach USD 126.0 billion by 2035, reflecting an absolute growth of USD 32.0 billion during the forecast period. This represents total growth of 34.0%, with the market advancing at a CAGR of 3.0% from 2025 to 2035.

Vocational trucks—designed for specialized tasks such as construction, mining, waste management, utilities, and emergency services—are becoming indispensable as governments and private enterprises invest heavily in infrastructure modernization and industrial productivity.

Strategic Market Drivers

Infrastructure Development Fuels Demand

Large-scale investments in road construction, smart cities, housing, and public utilities are significantly boosting demand for dump trucks, concrete mixers, refuse trucks, and utility vehicles. Emerging economies, in particular, are witnessing heightened procurement of vocational trucks to support rapid urban expansion and industrialization.

Browse Full Report: https://www.factmr.com/report/4064/vocational-trucks-market

Construction & Mining Activities Drive Fleet Expansion

The resurgence of construction, mining, and quarrying activities globally is a key growth engine. Vocational trucks provide high load capacity, durability, and off-road performance, making them essential for heavy-duty operations in challenging environments.

Municipal & Waste Management Growth

Increasing urban populations are accelerating demand for waste collection, sanitation, and municipal service trucks. Governments are upgrading fleets with modern vocational trucks to improve efficiency, reduce emissions, and comply with environmental regulations.

Technological Advancements in Truck Design

OEMs are integrating telematics, advanced driver assistance systems (ADAS), fuel-efficient powertrains, and electric drivetrains into vocational trucks. These innovations enhance safety, optimize fleet operations, and reduce total cost of ownership for operators.

Regional Growth Highlights

North America: Infrastructure Renewal & Fleet Modernization

North America remains a leading market, driven by aging infrastructure replacement, strong construction activity, and municipal fleet upgrades. The U.S. continues to invest in highway development, utilities, and public works, sustaining demand for vocational trucks.

Europe: Sustainability & Regulatory Compliance

European demand is supported by stringent emission norms, growing adoption of electric and low-emission vocational trucks, and smart city initiatives. Countries such as Germany, France, and the U.K. are at the forefront of fleet electrification.

East Asia: Industrial Growth & Urban Expansion

China, Japan, and South Korea are witnessing steady growth due to industrial development, infrastructure investments, and expanding municipal services. China dominates regional demand with large-scale construction and mining activities.

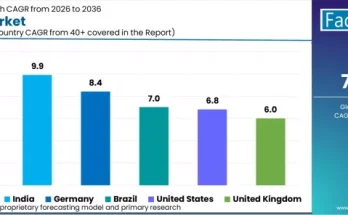

Emerging Markets: High Potential Growth

India, Southeast Asia, Latin America, and the Middle East offer strong growth opportunities, fueled by:

- Rapid urbanization

- Government-backed infrastructure projects

- Expansion of mining, oil & gas, and construction sectors

Market Segmentation Insights

By Truck Type

- Dump Trucks – Largest segment due to extensive use in construction and mining

- Refuse Trucks – Growing rapidly with urban waste management needs

- Concrete Mixers – Strong demand from infrastructure and housing projects

- Utility & Service Trucks – Rising adoption in power, telecom, and municipal services

By Propulsion

- Diesel Trucks – Dominant due to high torque and long-haul capability

- Electric & Hybrid Trucks – Gaining traction amid emission regulations and sustainability goals

By Application

- Construction – Leading segment globally

- Municipal Services – Fast-growing due to smart city initiatives

- Mining & Oil & Gas – Stable demand for heavy-duty applications

- Utilities & Emergency Services – Increasing fleet investments

Challenges Impacting Market Growth

High Acquisition & Maintenance Costs

Vocational trucks require significant upfront investment and maintenance, which can deter small and mid-sized fleet operators.

Emission Regulations & Compliance Costs

Stricter emission standards increase R&D and manufacturing costs for OEMs, impacting pricing and margins.

Electrification Challenges

While electric vocational trucks are gaining interest, limited charging infrastructure and high battery costs remain key barriers in many regions.

Competitive Landscape

The vocational trucks market is moderately consolidated, with manufacturers focusing on product customization, durability, fuel efficiency, and electrification to gain a competitive edge.

Key Companies Profiled

- Daimler Truck AG

- Volvo Group

- PACCAR Inc.

- Tata Motors

- Ashok Leyland

- Navistar International

- MAN Truck & Bus

- Scania AB

- Isuzu Motors

- Hino Motors

Recent Developments

- 2024: OEMs introduced electric refuse and utility trucks for urban fleets

- 2023: Increased deployment of telematics-enabled vocational trucks for fleet optimization

- 2022: Major construction firms upgraded fleets with fuel-efficient and low-emission trucks

Future Outlook: Steady Growth Through Specialized Innovation

Over the next decade, the vocational trucks market will evolve through:

- Expansion of global infrastructure projects

- Gradual electrification of municipal and utility fleets

- Integration of smart fleet management technologies

- Rising demand for application-specific, high-durability vehicles

As infrastructure, construction, and municipal services remain core pillars of economic development, the global vocational trucks market is positioned for stable, long-term growth through 2035, driven by reliability, specialization, and technological advancement.