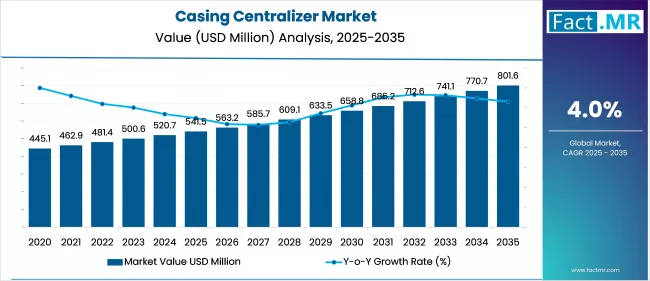

The global Casing Centralizer Market is poised for steady growth from 2026 through 2036, underpinned by expanding oil and gas exploration, technological innovations, and increasingly stringent regulatory standards. The market value is projected to rise from approximately USD 541.5 million in 2025 to USD 801.6 million by 2035, representing a CAGR of around 4% over the forecast period.

Market Overview & Growth Dynamics

Casing centralizers serve a critical function in drilling operations by ensuring that casing strings remain centralized within wellbores, thereby improving cement placement and zonal isolation. These devices are essential components in both onshore and offshore drilling, particularly in complex well geometries such as horizontal and deepwater wells.

Global drilling activity has grown in response to rising energy demand—fueled by industrial expansion and sustained fossil fuel reliance—while also integrating with emerging low‑carbon applications such as carbon capture and storage (CCS) wells. In this context, the demand for robust and high‑performance casing centralizers continues to rise, reflecting a convergence of operational, technological, and regulatory drivers.

Innovation Catalysts Shaping the Market

Technological innovation is a central growth driver in the casing centralizer sector. Manufacturers are increasingly investing in R&D to support next‑generation solutions that enhance well integrity, durability, and drilling efficiency.

1. Advanced Materials and Performance Enhancements:

New materials such as corrosion‑resistant polymers, composite alloys, and high‑grade steels are being adopted to withstand high-pressure, high-temperature (HPHT) environments prevalent in deepwater drilling and ultra-deep wells. These materials reduce friction, drag, and wear, while improving long-term durability in challenging downhole conditions.

2. Smart & Digital Integration:

Digitalization is transforming traditional centralizers into intelligent tools. Integration of sensors, Internet of Things (IoT) connectivity, and real-time monitoring technologies allows operators to track centralizer performance during installation, providing insights that can improve cementing outcomes and reduce operational risk. Early adopters report enhanced quality verification in cement placement with smart tools.

3. Customization & Application-Specific Designs:

Centralizers tailored to specific well types—such as hybrid designs combining features of bow-spring and rigid centralizers—are gaining traction. These customized solutions optimize performance for deviations, high-angle trajectories, and extended-reach drilling. Additionally, lightweight and eco-friendly composites are being explored to reduce environmental impact and operational costs.

Regulatory Impact and Compliance Trends

Regulatory frameworks across oil and gas producing regions are exerting a significant influence on market dynamics. Increasingly stringent standards on well construction, zonal isolation integrity, and environmental safety are compelling operators to adopt higher-quality centralizers that meet international certifications such as API 10D and ISO 10427 compliance.

In North America, tightening well construction regulations have elevated the importance of high-performance casing centralizers in shale and unconventional well contexts. Meanwhile, in the Middle East, regulatory criteria for centralizers in HPHT and offshore projects are raising the bar for supplier qualification, with preference given to designs that fulfill rigorous performance and safety standards.

Additionally, compliance mandates in CCS wells—where long-term containment integrity is vital—are driving demand for robust centralizer technologies that can support CO₂ injection and storage operations without compromise.

Regional Market Trends

Asia-Pacific Dominance: Fueled by extensive drilling programs in China, India, and Southeast Asia, the Asia-Pacific region continues to lead global centralizer demand. National oil companies are expanding both onshore and offshore exploration, with centralizers playing a pivotal role in enhancing cementing efficiency in deepwater projects.

North America’s Technological Emphasis: The United States and Canada remain key markets due to mature drilling infrastructures and increased shale operations. The proliferation of horizontal wells and multi-stage hydraulic fracturing processes has intensified requirements for advanced centralizers that maintain casing concentricity across complex well profiles.

Europe and CCS Opportunities: In Europe, redevelopment initiatives in the North Sea and investment toward CCS projects are encouraging the adoption of next-generation centralizers suited to HPHT environments.

Middle East & Africa: National oil companies in the region are focusing on field optimization and enhanced recovery. Projects in Saudi Arabia and the UAE emphasize performance and compliance, with investments directed at local manufacturing capabilities to alleviate supply chain constraints.

Segment Insights: Product, Material, & Application

Product Types:

-

Bow-spring centralizers continue to dominate due to their flexibility and restoring force, especially in deviated and horizontal wells.

-

Rigid-blade centralizers are experiencing rapid growth in offshore environments where strong standoff and reduced drag are essential for deepwater operations.

Materials:

-

Steel centralizers remain prevalent for their strength and reliability across conventional wells.

-

Polymers and composite variants are gaining market share due to their lightweight and corrosion-resistant properties, particularly in offshore and HPHT applications.

Application:

-

Onshore drilling accounts for the largest portion of centralizer demand, driven by extensive unconventional plays across North America and Asia-Pacific.

-

Offshore drilling exhibits the fastest growth rate, driven by deepwater projects that require specialized centralizers with advanced material properties and regulatory compliance.

Key Market Challenges

Despite positive growth drivers, the casing centralizer market faces several constraints:

-

Performance inconsistency across diverse well conditions remains a concern, particularly in deepwater and highly deviated wells, where improper selection can jeopardize cementing quality and well integrity.

-

Raw material price volatility and supply chain disruptions influence manufacturing cost structures and delivery timelines.

-

Access to advanced testing facilities for validating new designs under extreme conditions is limited, hindering innovation and regulatory approval processes in some regions.

Browse Full Report : https://www.factmr.com/report/2788/casing-centralizer-market

Competitive Landscape & Strategic Developments

The market is highly competitive, with key players emphasizing product differentiation through performance, compliance, and innovation. Leading suppliers are investing in technologies that enhance durability and wellbore performance under HPHT conditions. Strategic partnerships, capacity expansion, and automated manufacturing platforms are shaping competitive positioning.

Outlook & Revenue Forecasts (2026-2036)

Market projections indicate a continued upward trajectory through 2036, supported by:

-

Expanding global drilling activity to meet rising energy demand.

-

Technological breakthroughs, particularly in smart and composite centralizers.

-

Regulatory imperatives driving adoption of higher-performance, compliant solutions.

-

Growing offshore and CCS projects requiring advanced casing support tools.

With a projected CAGR of ~4% through 2035, and ongoing innovations and regulatory influences, the casing centralizer market is expected to deliver sustainable revenue growth through 2036 as industry stakeholders align with evolving drilling complexities and well integrity standards.