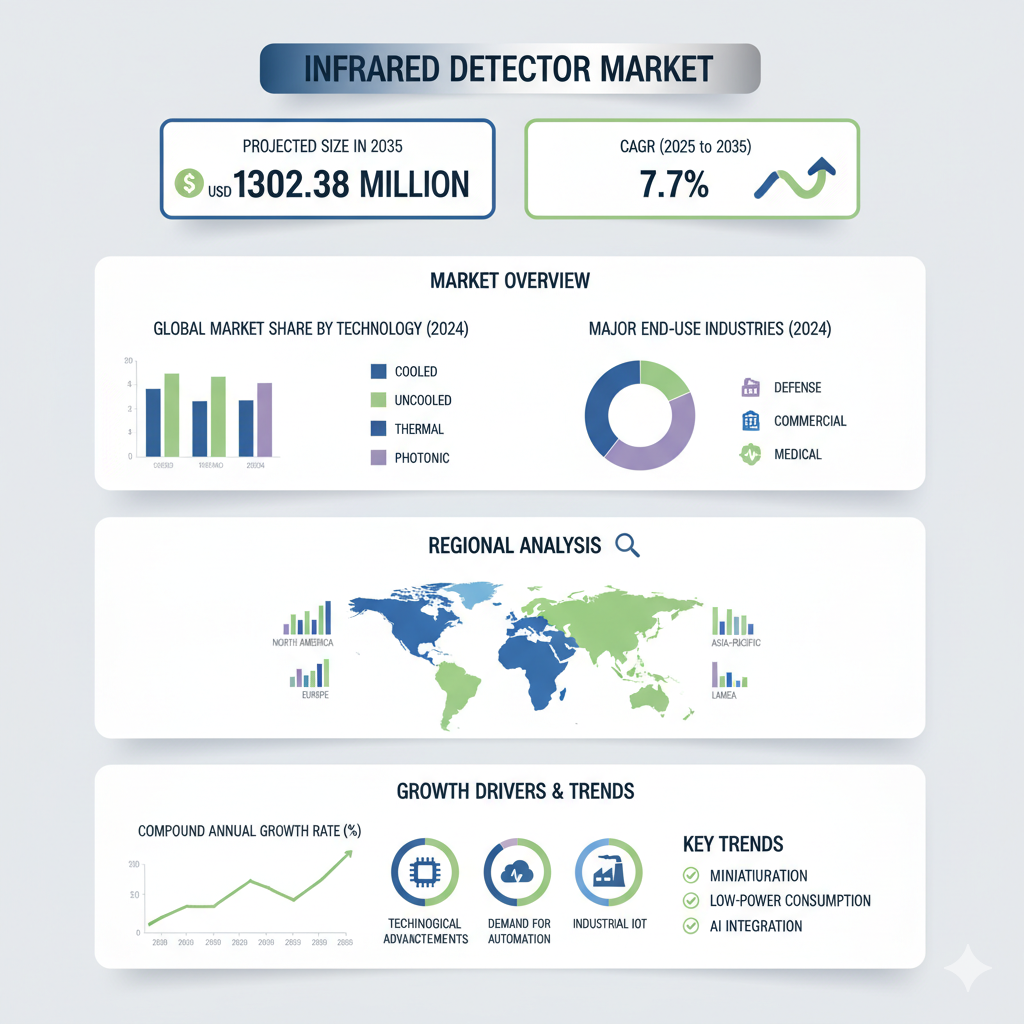

The global infrared detector market is poised for remarkable growth over the coming decade, driven by the increasing adoption of advanced sensing technologies across multiple industries such as automotive, defense, healthcare, and consumer electronics. According to Fact.MR, the global infrared detector market is valued at USD 620.27 million in 2025. It is projected to grow at a compound annual growth rate (CAGR) of 7.7%, reaching USD 1,302.38 million by 2035.

Market Overview and Growth Drivers

Infrared detectors are key components in systems that measure and convert infrared radiation into electrical signals, enabling functionalities such as night vision, thermal imaging, temperature monitoring, and motion sensing. Their adoption has expanded significantly due to their critical role in modern defense and security systems, automotive safety technologies, industrial automation, and medical diagnostics.

In the automotive sector, infrared detectors are used for driver assistance, pedestrian detection, and collision avoidance systems, all of which are essential for the development of autonomous vehicles. In the security and surveillance domain, governments and organizations are increasingly deploying thermal imaging systems for border control, public safety, and critical infrastructure protection. Meanwhile, in consumer electronics, the integration of infrared sensors in smartphones, smart home devices, and wearables is accelerating as consumers demand more intuitive and responsive devices.

Technological advancements such as miniaturization, higher sensitivity, and the integration of artificial intelligence (AI) for real-time image processing are reshaping the market. Additionally, the push for uncooled and low-power infrared detectors has made them more accessible for commercial applications. Increased investments in defense modernization and smart city infrastructure projects are further expected to fuel market expansion globally.

Infrared Detector Market Segmentation

By Spectral Range

Based on spectral range, the market is segmented into short-wave infrared (SWIR), mid-wave infrared (MWIR), and long-wave infrared (LWIR) detectors. SWIR detectors are expected to record robust growth as they deliver high-resolution imaging under low-light or foggy conditions, making them highly suitable for both industrial and defense applications.

By Technology

Infrared detector technology segments include mercury cadmium telluride (MCT), indium gallium arsenide (InGaAs), pyroelectric, thermopile, microbolometer, and others. Among these, MCT-based detectors hold a leading share due to their superior sensitivity and broad wavelength detection range. Microbolometers, however, are gaining popularity because they offer high performance at a lower cost, particularly in uncooled systems used in commercial and consumer markets.

By Application

In terms of applications, the market is categorized into automotive, consumer electronics, medical, military, and security segments. The automotive segment is expected to grow significantly as vehicles become increasingly equipped with infrared-based safety systems. The medical sector is also emerging as a major user of infrared detectors for non-contact temperature measurement, early disease diagnosis, and patient monitoring.

By Region

Regionally, the market covers North America, Latin America, Western Europe, East Asia, South Asia & Pacific, and the Middle East & Africa. China is projected to record one of the fastest growth rates owing to strong industrialization, rising consumer electronics demand, and increasing focus on vehicle safety. North America remains a significant market due to heavy defense spending, early adoption of autonomous vehicles, and technological leadership in sensor innovation.

Browse Full Report: https://www.factmr.com/report/infrared-detector-market

Recent Developments and Competitive Landscape

Recent years have witnessed substantial innovation in the infrared detector market. Manufacturers are increasingly integrating AI and advanced image analytics into their products to enhance real-time decision-making and automate anomaly detection. The trend toward uncooled, compact, and power-efficient infrared sensors continues to dominate, particularly for consumer and IoT applications. Companies are also focusing on vertical-specific customization, offering tailored solutions for defense, medical imaging, and smart infrastructure projects.

Mergers, acquisitions, and partnerships have become common strategies as companies aim to expand their technological expertise and geographic presence. Moreover, meeting regulatory and certification standards is becoming essential as infrared detectors are used in critical sectors such as defense and healthcare, where reliability and accuracy are paramount.

The competitive landscape of the infrared detector market is moderately consolidated, with a few global leaders holding substantial market shares. Teledyne FLIR, Raytheon Technologies, L3Harris Technologies, Leonardo S.p.A., BAE Systems, and Lynred are among the prominent players. These companies dominate through continuous product innovation, defense contracts, and strategic collaborations. Other notable participants include Northrop Grumman, Thales Group, Hamamatsu Photonics, Lockheed Martin, Honeywell, Bosch Security Systems, and Excelitas Technologies.

Competition within the market is largely defined by technology leadership, software integration capabilities, and cost efficiency. Companies that combine advanced detector hardware with AI-based analytics and robust system integration are expected to achieve a competitive edge. Additionally, regional manufacturing and certification advantages help firms gain access to lucrative defense and infrastructure projects.