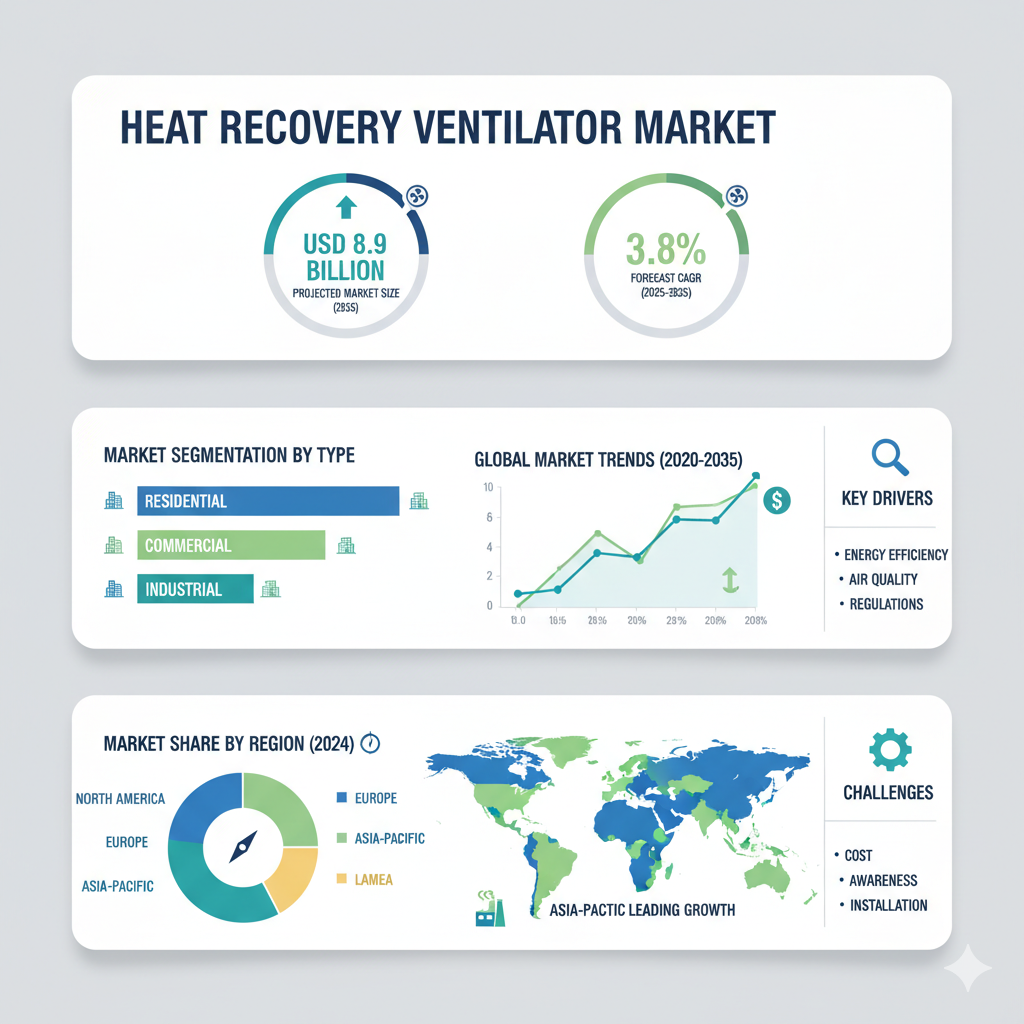

The global heat recovery ventilator market is forecast to reach USD 8.9 billion by 2035, up from USD 6.1 billion in 2025. During the forecast period, the industry is projected to register a CAGR of 3.8%.

The market is segmented based on multiple parameters including mounting, venting, operation, flow rate, heat exchanger type, end use, and region. By mounting, the market includes wall-mounted, ceiling-mounted, and cabinet-mounted systems. By venting, the classification includes horizontal and vertical systems. Based on operation, the market is divided into automatic and manual units.

Flow rate categories include below 50 L/min, 50 to 200 L/min, 201 to 500 L/min, 501 to 1,000 L/min, and above 1,000 L/min. Heat exchanger types comprise cross flow plates, counterflow plate heat exchangers, and rotating heat exchangers. In terms of end use, the market serves residential, commercial, and industrial applications. Regionally, the market covers North America, Europe, Asia Pacific, Latin America, and the Middle East & Africa.

This segmentation enables manufacturers and stakeholders to identify targeted opportunities across technical, operational, and application-based dimensions.

Recent Market Developments and Competitive Landscape

In recent years, the heat recovery ventilator (HRV) market has witnessed notable advancements as the demand for energy-efficient and environmentally sustainable ventilation solutions continues to rise. The growing emphasis on indoor air quality, combined with the need to reduce energy consumption in modern buildings, has accelerated innovation within the industry.

Smart and connected ventilation systems are increasingly shaping market growth. These systems are now equipped with sensors that monitor air quality and temperature, allowing for real-time adjustments through automated controls or integration with smart home and building management systems. This shift towards intelligent ventilation is particularly prominent in urban regions and commercial buildings, where maintaining optimal indoor environments is crucial.

Retrofit installations have also become an important area of development. As sustainability initiatives push for reduced carbon footprints, many property owners are opting to upgrade existing buildings rather than construct new ones. Heat recovery ventilators that can be easily integrated into older HVAC systems are therefore gaining attention, particularly in North America and Europe.

From a competitive standpoint, several global leaders are driving technological innovation and strategic expansion. Companies such as Honeywell International Inc., Johnson Controls, Nortek Air Solutions, Greenheck Fan Corporation, Lennox International, and Trane continue to dominate the market. In addition, Asian manufacturers like Panasonic Corporation, Mitsubishi Electric, and Daikin Industries, Ltd. are strengthening their international presence through energy-efficient product lines and strategic partnerships.

Competition in the market is becoming increasingly centered on product efficiency, automation, and regional service capabilities. Manufacturers are investing in research and development to create compact, high-performance systems suitable for both new installations and retrofits. Many are also expanding their product portfolios with ultra-low energy HRVs and units capable of both heat and humidity recovery. Compliance with green building certifications and energy-efficiency standards has emerged as a key differentiator, especially in developed markets with stringent environmental regulations

Segment-Specific Insights

Mounting Type: Wall-mounted units continue to dominate due to their ease of installation and suitability for residential use.

Venting Configuration: Horizontal venting remains the most common configuration, particularly in low-rise and residential structures.

Operation Mode: Automatic heat recovery ventilators are increasingly preferred over manual ones due to their ability to adjust airflow dynamically and maintain consistent air quality.

Flow Rate: The 50 to 200 L/min range is expected to dominate the market, catering to residential and small commercial applications. Higher flow rate units, particularly those above 1,000 L/min, are typically used in large industrial facilities and public buildings where air volume requirements are significant.

Heat Exchanger Type: Cross flow plate heat exchangers remain the most widely used due to their simplicity and cost-effectiveness. However, counterflow plate and rotating heat exchangers are becoming more prominent as end users seek higher thermal efficiency and lower energy losses.

End Use: The residential segment accounts for the largest share of the market, supported by rising awareness of indoor air quality and energy-efficient homes. Commercial buildings such as offices, hospitals, and schools are emerging as fast-growing segments due to stricter ventilation standards.

Regional Trends: North America and Europe continue to lead the global market due to strong environmental policies and high adoption of energy-efficient technologies.

Outlook and Strategic Implications

The heat recovery ventilator market is on a steady growth path, with sustainability, energy efficiency, and technology integration serving as its key drivers. The transition from conventional ventilation systems to intelligent, automated, and eco-friendly alternatives presents significant opportunities for both established manufacturers and new entrants.

To remain competitive, companies must focus on continuous innovation, particularly in the areas of smart controls, sensor integration, and modular system design. Expanding into emerging markets with retrofit-friendly and cost-effective solutions will be essential to capture the next wave of demand. Additionally, aligning products with evolving building energy codes and air-quality regulations will be crucial for long-term success.