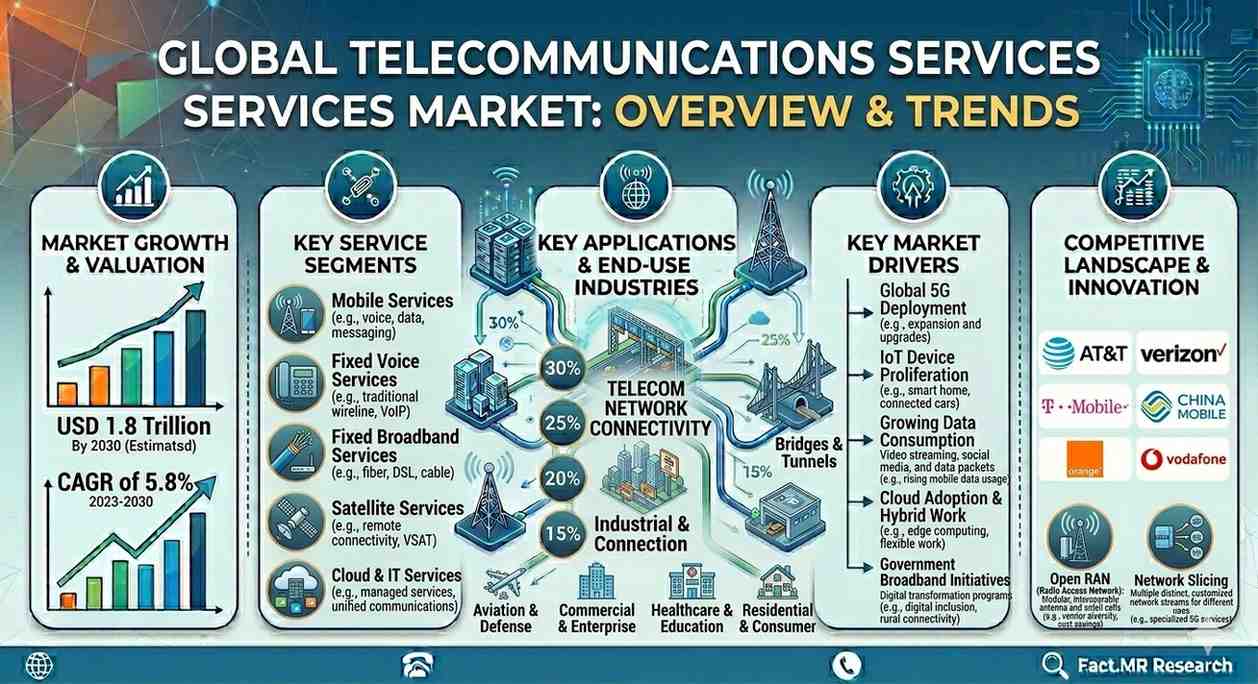

According to Fact.MR’s latest analysis, the global telecommunications services market is valued at USD 2,395.6 billion in 2026 and is projected to reach USD 2,516.3 billion in 2027, expanding to USD 4,312.8 billion by 2036. The market is expected to grow at a CAGR of 6.1% during 2026–2036, creating an incremental opportunity of USD 1,917.2 billion.

The market is undergoing a major transformation from legacy voice and fixed-line services toward 5G mobile broadband, enterprise connectivity, and IoT-enabled communication services. Increasing digitalization across industries, cloud adoption, and private 5G networks are driving telecom operators to reposition themselves as digital infrastructure providers.

Quick Stats

- Market Size (2026): USD 2,395.6 Billion

- Market Size (2027): USD 2,516.3 Billion

- Forecast Value (2036): USD 4,312.8 Billion

- CAGR (2026–2036): 6.1%

- Incremental Opportunity: USD 1,917.2 Billion

- Leading Segment: Mobile Telecom Services (64% share)

- Leading End User: BFSI (24% share)

- Leading Region: Asia Pacific

- Key Players: AT&T, Verizon Communications, China Mobile, Bharti Airtel, Vodafone Group, Deutsche Telekom

Executive Insight for Decision Makers

Telecommunications operators are transitioning from consumer voice services to enterprise connectivity, private networks, and digital infrastructure solutions. Revenue growth is increasingly driven by enterprise 5G, managed connectivity, and IoT services.

Strategic priorities

- Accelerate private 5G deployments for enterprises

- Expand fibre and backhaul infrastructure

- Develop cloud-integrated connectivity services

- Target high-value enterprise verticals

Operators that fail to shift toward enterprise connectivity risk stagnating ARPU and declining legacy service revenue.

Market Dynamics

Key Growth Drivers

- Rapid global 5G deployment and premium data plans

- Increasing enterprise demand for private networks

- Expansion of fibre broadband infrastructure

- Growth in IoT and connected devices

Key Restraints

- High capital expenditure for network rollout

- Spectrum licensing and regulatory costs

- Competitive pricing pressure in consumer markets

Emerging Trends

- Private 5G networks for enterprises

- Convergence of telecom and cloud services

- Network slicing for industry-specific use cases

- Expansion of managed connectivity services

Segment Analysis

Leading Segment

Mobile telecom services dominate with 64% market share in 2026, driven by rising smartphone adoption and 5G upgrades.

Fastest-Growing Segment

Enterprise private 5G networks are projected to grow fastest due to demand from manufacturing, healthcare, and BFSI sectors.

End-Use Breakdown

- BFSI – 24% share

- IT & Telecom – rapidly expanding

- Healthcare – strong adoption

- Manufacturing – private 5G deployments

- Government – smart infrastructure

Enterprise segments offer higher margins compared to consumer connectivity services.

Supply Chain Analysis

Raw Material Suppliers

- Network equipment manufacturers

- Semiconductor and telecom hardware suppliers

- Fibre optic cable manufacturers

Manufacturers / Producers

- Telecom network operators

- Mobile service providers

- Internet service providers

Distributors

- Enterprise connectivity resellers

- Managed service providers

- System integrators

End Users

- Consumers (mobile and broadband users)

- Enterprises (private networks, SD-WAN)

- Government agencies

- Financial institutions

Who Supplies Whom

- Equipment vendors supply network hardware to telecom operators

- Operators deploy infrastructure and provide connectivity services

- Managed service providers deliver customized enterprise solutions

- Enterprises and consumers subscribe to telecom services

Pricing Trends

Telecommunications pricing varies between consumer broadband packages and premium enterprise connectivity services.

Commodity Segment

- Consumer voice and data plans

- Competitive pricing pressure

- Lower margins

Premium Segment

- Private 5G networks

- Enterprise managed connectivity

- Guaranteed service-level agreements

Pricing drivers:

- Spectrum acquisition costs

- Infrastructure investments

- Data consumption demand

- Regulatory compliance requirements

- Service-level agreements

Enterprise connectivity services typically generate 30–45% higher margins compared to consumer services.

Regional Analysis

Top Countries by CAGR (2026–2036)

- India – 8.5%

- China – 7.1%

- United States – 6.4%

- South Korea – 5.8%

- Germany – 5.0%

Regional Insights

- Asia Pacific: Largest and fastest-growing due to massive subscriber base and 5G investment

- North America: Highest ARPU driven by enterprise connectivity

- Europe: Growth supported by private 5G and regulatory frameworks

Developed vs Emerging Markets

- Developed markets focus on enterprise connectivity and premium services

- Emerging markets prioritize mobile broadband expansion

Competitive Landscape

The global telecommunications services market is competitive but country-concentrated, with major operators dominating domestic markets.

Key Players

- AT&T

- Verizon Communications

- China Mobile

- Bharti Airtel

- Vodafone Group

- Deutsche Telekom

- Telefonica

- Orange S.A.

- T-Mobile

- Telecom Egypt

Competitive Strategies

- Expansion of 5G coverage

- Private network deployments

- Fibre infrastructure investment

- Enterprise service bundling

- Strategic partnerships with cloud providers

Strategic Takeaways

For Manufacturers / Operators

- Invest in enterprise private 5G networks

- Expand fibre backbone infrastructure

- Develop value-added digital services

For Investors

- Focus on enterprise connectivity and IoT services

- Target high-growth Asia Pacific markets

For Marketers / Distributors

- Offer vertical-specific connectivity solutions

- Promote managed network services

Future Outlook

The telecommunications services market is evolving into digital connectivity ecosystems supporting smart cities, Industry 4.0, and cloud computing.

Future developments include:

- 5G-Advanced deployment

- Edge computing integration

- Network slicing services

- Satellite-5G hybrid connectivity

Conclusion

The global telecommunications services market is transitioning from traditional voice services to advanced digital connectivity platforms. With enterprise private networks, IoT adoption, and 5G rollout accelerating, telecom operators that invest in infrastructure and enterprise solutions will capture substantial growth opportunities.

Why This Market Matters

Telecommunications services form the backbone of the digital economy, enabling cloud computing, financial services, smart cities, and connected industries, making this market critical for global economic and technological transformation.

Browse Full Report –

https://www.factmr.com/report/telecommunications-services-market