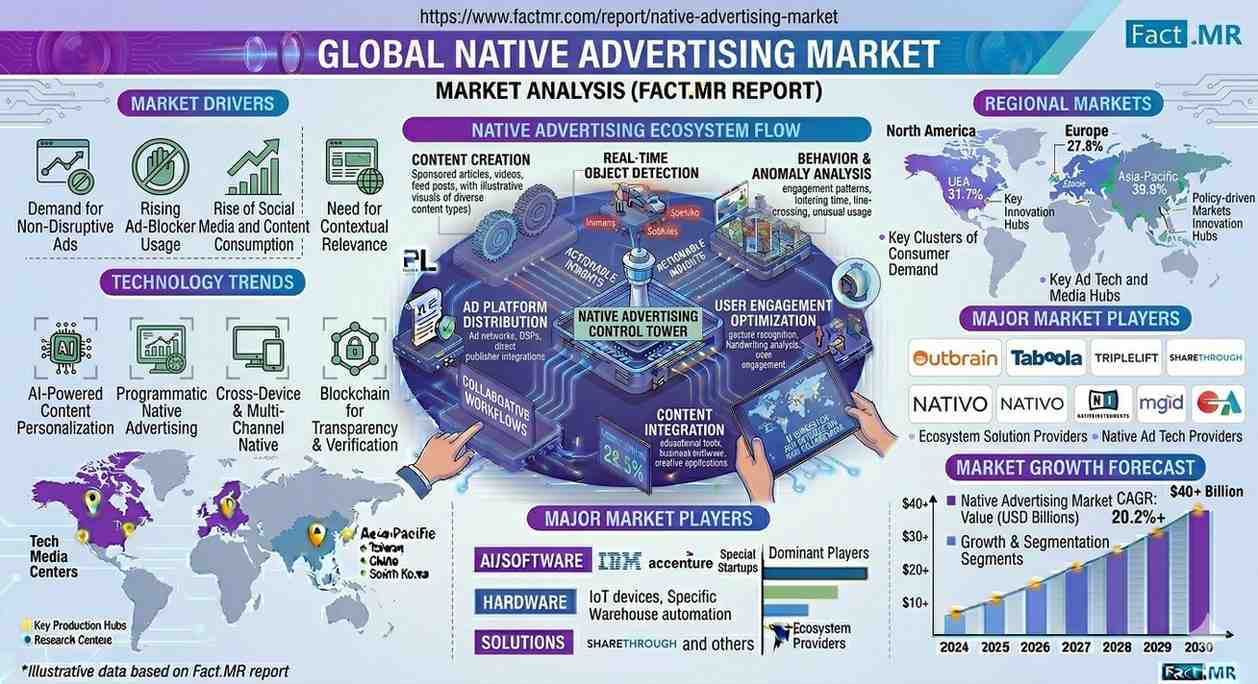

According to Fact MR’s latest analysis, the Global Native Advertising Market is undergoing rapid structural transformation as advertisers shift toward content-integrated formats that enhance engagement and improve campaign performance. The market is valued at USD 125.6 billion in 2026, projected to reach USD 154.9 billion in 2027, and is forecast to expand to USD 892.2 billion by 2036, growing at a CAGR of 21.7%. The industry is expected to generate an incremental opportunity of USD 766.6 billion during the forecast period.

The market transformation is driven by declining effectiveness of traditional display advertising, increased adoption of mobile-first content consumption, and the expansion of programmatic distribution technologies. Native advertising formats—integrated within editorial feeds, search results, and digital platforms—are increasingly preferred by brands seeking higher engagement rates and contextual relevance.

Quick Stats

- Market Size (2026): USD 125.6 Billion

- Market Size (2027): USD 154.9 Billion

- Forecast Value (2036): USD 892.2 Billion

- CAGR (2026–2036): 21.7%

- Incremental Opportunity: USD 766.6 Billion

- Leading Segment: Hybrid Platforms (34.9% share)

- Leading Region: North America

- Fastest Growing Country: United States

- Key Players: Taboola, Outbrain, TripleLift, StackAdapt, Nativo, Revcontent

Executive Insight for Decision Makers

The native advertising ecosystem is shifting from banner-based exposure models toward performance-driven content integration strategies. Digital advertisers are prioritizing contextual placements within editorial and social environments to improve audience engagement and conversion efficiency.

What industry stakeholders must do:

- Invest in AI-driven audience targeting and analytics

- Expand hybrid distribution capabilities across publishers

- Develop in-house content creation aligned with editorial tone

- Strengthen compliance with advertising disclosure regulations

Risks of not adapting:

- Declining campaign ROI due to banner fatigue

- Reduced visibility in mobile-first environments

- Loss of competitive positioning in programmatic ecosystems

Market Dynamics

Key Growth Drivers

- Migration of marketing budgets toward content-integrated digital formats

- Rising mobile internet consumption and social media engagement

- Expansion of programmatic advertising technologies

- Higher click-through rates compared with display advertising

Key Restraints

- Increasing regulatory scrutiny on sponsored content disclosure

- Dependence on publisher network partnerships

- Measurement complexity across multiple content platforms

Emerging Trends

- AI-powered contextual targeting and recommendation engines

- Growth of in-feed video native advertising

- Expansion of hybrid native advertising platforms

- Integration of commerce-enabled native content

Segment Analysis

Leading Segment:

Hybrid platforms account for 34.9% market share, driven by their ability to distribute campaigns across multiple publisher ecosystems while maintaining centralized campaign management.

Fastest-Growing Segment:

Search-based native ads, representing 27.1% share, are expanding rapidly due to alignment with consumer search intent and contextual placement.

Key Segment Breakdown

- Platform: Closed, Open, Hybrid

- Type: In-feed ads, Search ads, Promoted listings, Recommendation units

- Environment: Social media, news portals, mobile apps, marketplaces

Strategic Importance

Hybrid platforms provide scalability, while search-native formats offer high conversion efficiency, making both critical for long-term growth strategies.

Supply Chain Analysis (Value Chain Structure)

Raw Inputs

- Audience data providers

- Content creators and editorial teams

- Ad tech infrastructure providers

Manufacturers / Producers

- Native advertising technology platforms

- Programmatic distribution engines

- Content recommendation systems

Distributors

- Publisher networks

- Media websites and digital platforms

- Social media and mobile applications

End Users

- Brands and advertisers

- Digital marketing agencies

- E-commerce platforms

Who Supplies Whom

Ad tech providers supply native advertising platforms with targeting algorithms → Platforms integrate with publisher networks → Publishers provide inventory → Advertisers purchase placements → End users consume integrated promotional content.

Pricing Trends

- Native advertising pricing varies between performance-based CPC models and premium content placement packages

- Premium pricing commanded by high-traffic publishers and contextual relevance

- Key influencing factors:

- Audience targeting accuracy

- Publisher network reach

- Content production costs

- Regulatory compliance requirements

- Margin Insights:

- Platforms maintain higher margins through proprietary algorithms

- Publishers earn premium rates for integrated placements

Regional Analysis

Top 5 Countries by CAGR (2026–2036)

- United States — 20.6%

- South Korea — 18.7%

- Germany — 15.6%

- China — 13.2%

- United Kingdom — Emerging high-growth market

Regional Growth Drivers

- North America: Mature programmatic ecosystem and content marketing adoption

- East Asia: Mobile-first digital consumption and social commerce growth

- Europe: Strong publishing networks and regulatory transparency

- Emerging Markets: Rapid digital media expansion and SME adoption

Developed vs Emerging Markets

Developed markets lead in technology adoption, while emerging markets drive volume growth through mobile advertising expansion.

Competitive Landscape

The market structure is moderately concentrated, with leading platform providers controlling large publisher networks.

Key Companies

- Taboola

- Outbrain

- TripleLift

- StackAdapt

- Nativo

- Revcontent

- AdPushup

- Instinctive

Competitive Strategies

- Expansion of publisher partnerships

- AI-driven targeting innovation

- Programmatic distribution capabilities

- Performance-based pricing models

- Cross-platform campaign integration

Strategic Takeaways

For Manufacturers / Platforms

- Invest in AI and personalization technologies

- Expand hybrid distribution infrastructure

For Investors

- Focus on companies with strong publisher networks

- Prioritize platforms with programmatic capabilities

For Marketers / Distributors

- Adopt multi-platform native advertising strategies

- Align branded content with editorial environments

Future Outlook

The native advertising market is expected to evolve into AI-powered, contextual content ecosystems. Automation, personalization, and commerce integration will redefine digital advertising efficiency. Sustainability in advertising—through reduced intrusive formats—will further drive adoption.

Long-term opportunities include:

- AI-driven content recommendations

- Commerce-integrated native ads

- Cross-device personalization

- Voice and AR native advertising formats

Conclusion

The Global Native Advertising Market is entering a high-growth phase fueled by digital content integration, programmatic targeting, and mobile-first engagement strategies. Companies that invest in advanced analytics, hybrid platforms, and contextual content capabilities will capture significant market share. Decision-makers who adapt early will benefit from expanding revenue opportunities and stronger consumer engagement.

Why This Market Matters

Native advertising represents the future of digital marketing—blending content, commerce, and technology to deliver measurable engagement. As traditional advertising loses effectiveness, integrated promotional formats are becoming essential for brands seeking relevance, performance, and scalability in a rapidly evolving digital economy.

Browse Full Report –

https://www.factmr.com/report/native-advertising-market