The global electric vehicle (EV) infrastructure landscape is undergoing a monumental shift. According to the latest strategic analysis by Fact.MR, the EV charging cable market is being reshaped by a “perfect storm” of ultra-rapid power supply breakthroughs, massive government mandates like India’s PM E-DRIVE, and a definitive standards migration in North America.

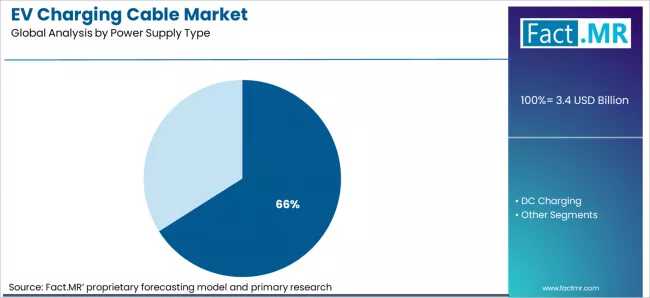

While AC charging cables are projected to maintain a dominant 66% market share in 2026 due to residential and workplace dominance, the value surge is concentrated in the high-power DC segment. The introduction of liquid-cooled cables capable of 1,000 kW boost power is officially moving EV charging out of the “overnight” phase and into the “ultra-fast” era.

Strategic Market Quick-Stats (2026)

- AC Dominance: 66% market share (Driven by home/workplace Mode 3 Type 2).

- Charging Sweet Spot: 7-22 kW fast-charging segment holds 52% share.

- Top Growth Engine: India leads with an unprecedented 4% CAGR (2026–2036).

- Innovation Peak: Commercial launch of 1,000 kW boost liquid-cooled CCS2 cables.

- Standard Migration: Largest globally recorded connector retrofit cycle (CCS1 to NACS) underway in the USA.

The Great Power Shift: From 7 kW to 1 Megawatt

The 2026 market is bifurcated between volume and value.

- AC Standard Expansion: The IEC 62196-2:2025 update has triggered a global design upgrade cycle, requiring recertification of Type 1 and Type 2 cables. This is being met by “Smart Cables” from leaders like Leoni, featuring integrated communication chips that support load balancing and the AFIR-mandated ISO 15118-20 Plug & Charge

- Ultra-Rapid DC Corridors: In May 2025, Phoenix Contact debuted its liquid-cooled CCS2 cable, delivering a continuous 800 kW output. This technology has already been integrated by Autel Energy into their MaxiCharger DT1000 series, enabling heavy-duty commercial fleets to charge at speeds once thought impossible.

Regional Growth Leaders (2026–2036)

| Country | Projected CAGR | Primary Growth Driver |

| India | 38.4% | PM E-DRIVE (INR 10,900 Cr) funding for 72,000 chargers. |

| Germany | 32.6% | AFIR (EU 2023/1804) mandatory CCS2 & smart charging by 2027. |

| Japan | 30.2% | Migration from legacy CHAdeMO to higher-power ChaoJi 3.0. |

| United States | 25.5% | $5B NEVI program and the massive NACS (SAE J3400) retrofit cycle. |

| China | 23.5% | Largest public charger base (1M+) upgrading to high-power GB/T. |

Competitive Landscape: Specialized Thermal Engineering vs. Scale

The market has split into two distinct competitive tiers. The Standard AC segment is price-driven and fragmented, with high-volume manufacturers like BESEN, DUOSIDA, and Sinbon leveraging scale.

However, the Premium DC segment is a high-moat territory dominated by Phoenix Contact, Leoni, Aptiv, and Prysmian. In this arena, the real differentiators are thermal management (liquid cooling), IEC certification depth, and deep integration with charging station platforms. For decision-makers, switching suppliers for high-power systems is technically complex, giving established players with liquid-cooled patents a long-term structural advantage.

Browse Full Report –

https://www.factmr.com/report/ev-charging-cable-market