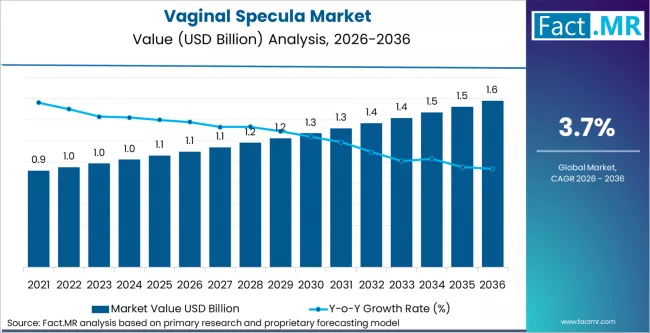

The global Vaginal Specula Market is projected to reach a valuation of USD 1.1 billion in 2026, expanding to USD 1.6 billion by 2036. This growth, representing a CAGR of 3.7%, is driven by non-discretionary gynecological examination volumes and the expansion of national cervical cancer screening programs. As healthcare systems prioritize infection control, the market is seeing a significant shift toward disposable, high-performance instruments.

Vaginal Specula Market Quick Stats

-

Market size 2026? USD 1.1 billion.

-

Market size 2036? USD 1.6 billion.

-

CAGR? 3.7% (2026–2036).

-

Leading product segment(s) and shares? General examination leads by volume; disposable specula hold a 35% share in 2026.

-

Leading material type and share? Disposable specula (35% share) are rapidly growing due to infection control protocols.

-

Leading end use and share? Hospitals and clinics hold approximately 60% of market value.

-

Key growth regions? North America (value leader) and Asia Pacific (fastest procedure volume growth).

-

Top companies? CooperSurgical Inc., Welch Allyn (Hillrom/Baxter), OBP Medical Corporation, MedGyn Products Inc., Integra LifeSciences Holdings Corp., Sklar Surgical Instruments, Amsino International Inc., SurgiLogix LLC, Pelican Feminine Healthcare Ltd., and Delasco LLC.

Market Momentum (YoY Path)

The Vaginal Specula Market is characterized by steady incremental expansion. Following a 2025 valuation of USD 1.0 billion, the market reaches USD 1.1 billion in 2026. Consistent demand for preventive care pushes values to an estimated USD 1.18 billion in 2028 and USD 1.27 billion in 2030. By 2031, the market scales to USD 1.32 billion, continuing to USD 1.42 billion in 2033. By the end of the forecast period in 2036, the market achieves its projected USD 1.6 billion peak, generating an absolute dollar opportunity of USD 0.5 billion.

Why the Market is Growing

Growth in the Vaginal Specula Market is fueled by the WHO’s target of 70% cervical screening coverage by 2030, increasing procurement across 45 countries. Rising sterilization costs and strict infection control mandates are accelerating the transition from reusable stainless steel to disposable alternatives. Furthermore, the expansion of outpatient and office-based gynecological procedures is significantly raising instrument consumption in ambulatory settings.

Segment Spotlight

1) Product Type

General examination remains the dominant procedure type for the Vaginal Specula Market. While routine screenings generate consistent demand, specialized segments such as vaginal specula with smoke evacuators are gaining traction for electrosurgical interventions, commanding higher price points and supporting market value growth.

2) Material Type (Disposable 35%)

Disposable specula are expected to hold a 35% share in 2026. This segment is bolstered by the elimination of sterilization processing and improved patient safety perceptions. Major players like OBP Medical and CooperSurgical have recently expanded their illuminated disposable lines to meet this demand.

3) End Use (Hospitals and Clinics 60%)

Hospitals and clinics represent roughly 60% of the market value. These entities benefit from high procedure volumes and centralized procurement systems. In regions like North America, Group Purchasing Organization (GPO) contracts are the primary mechanism for these end users to access premium disposable technologies.

Drivers, Opportunities, Trends, Challenges

Drivers: The primary engine for the Vaginal Specula Market is the surge in national health programs, such as India’s 42 million screenings in FY2023-24. Increased government funding for women’s health and the expansion of screening eligibility in countries like South Korea are creating a stable foundation for volume growth.

Opportunities: Manufacturers have a major opportunity in the development of ergonomic and illuminated designs. These advanced instruments solve mechanical visualization challenges and allow providers to focus on better clinical techniques, especially in private clinics and ASCs where patient comfort is a competitive differentiator.

Trends: There is a clear trend toward single-use instrument penetration in developed markets. NHS England and US-based GPOs are increasingly favoring disposable specula to comply with infection control frameworks and reduce the liability associated with healthcare-acquired infections (HAIs).

Challenges: The market faces structural constraints from reimbursement pressures in public health systems. Additionally, intense average selling price competition from low-cost reusable manufacturers in China and India remains a hurdle for premium segment expansion in cost-sensitive regions.

Country Growth Outlook (CAGR)

| Country | CAGR (2026-2036) |

| United States | 4.8% |

| South Korea | 4.3% |

| United Kingdom | 4.1% |

| Japan | 3.8% |

| India | 3.5% |

Browse Full Report : https://www.factmr.com/report/vaginal-specula-market

Competitive Landscape

The Vaginal Specula Market is moderately fragmented, with the top five manufacturers accounting for 40% to 45% of global revenue. CooperSurgical Inc. and OBP Medical Corporation lead the North American premium segment through innovative illuminated and ergonomic designs. Welch Allyn (Hillrom/Baxter) and Pelican Feminine Healthcare maintain strong supply relationships within major hospital networks and the UK’s NHS. Competition is defined by procurement access, with established GPO and government tender partnerships serving as the primary barrier to entry.