The global tractor market continues to demonstrate resilient growth amid rapid agricultural mechanization, technological innovation, and increasing demand for productivity enhancements across farms and allied sectors. The market’s transformation from conventional agricultural implements to advanced, multi-purpose machinery is reshaping competitive dynamics and creating strategic value opportunities worldwide.

Market Growth Trajectory: A Decade to 2036

The tractor market is poised to undergo robust expansion through 2036, driven by a convergence of favorable factors including rising global food demand, enhanced farm mechanization initiatives, and cross-sectoral applications such as construction, mining, and utility services. Historical data indicate that the global market expanded from approximately USD 80 billion in 2024 and is projected to surge to nearly USD 148 billion by 2034 — reflecting a strong compound annual growth rate (CAGR) of around 6.3% through the decade. Broader industry projections suggest sustained momentum beyond that horizon, with extended growth likely through 2036, underpinned by technology adoption, rising farm incomes, and infrastructure development in emerging regions.

Strategic Benchmarking: Competitive Landscape & Innovation

Industry leaders are strategically positioning themselves to capture growth opportunities through product portfolio expansion, digital integrations, and market-specific adaptations:

• Product Diversification: Manufacturers are increasingly offering tractors optimized for diverse end-use applications — from small-scale utility units to high-horsepower agricultural machines. Product line extensions include electric, hybrid, and GPS-enabled tractors that cater to precision agriculture and sustainability goals.

• Technology & Digital Integration: Precision farming capabilities, such as telematics, autonomous operation modules, and remote sensing systems, are becoming standard in premium segments — enabling farmers to maximize efficiency, lower operational costs, and improve crop outcomes.

• Strategic Partnerships: OEMs are collaborating with engine manufacturers and technology companies to deliver localized solutions. Joint ventures in Asia and cross-border R&D investments are accelerating product innovation and regional penetration.

Key players like Deere & Co., Mahindra & Mahindra, Kubota Corporation, New Holland, AGCO, Escorts Limited, and JCB are widely recognized for their robust global footprints and innovation pipelines. These companies invest heavily in supply chain resilience, dealer networks, and after-sales services to maintain competitiveness and loyalty across established and emerging markets.

Pricing Trends: Affordability Meets Value

Pricing dynamics in the tractor market reflect a balance between value offerings for small-scale farmers and premium pricing for advanced, high-tech configurations:

• Competitive Pricing & Subsidy Influence: Government subsidies, favorable financing instruments, and reduced tariffs in key markets have moderated upfront equipment costs, enabling a broader user base to access modern tractors. Subsidy-led affordability has been a key driver, particularly in Asia Pacific and Latin America.

• Technology Premiums: Smart, connected, and electrified tractors command higher pricing tiers due to the embedded technology and associated lifecycle benefits. Buyers are increasingly willing to pay premiums for features that reduce fuel use, improve productivity, and facilitate remote diagnostics.

• Regional Pricing Disparity: Tractor pricing varies significantly across regions depending on import duties, local manufacturing scale, and currency fluctuations. Emerging regions often see lower per-unit costs for entry-level models, while mature markets sustain higher price points for technologically advanced and high-horsepower units.

Regional Hotspots: Where Growth Is Most Dynamic

The tractor market’s growth is not uniform — specific regions are emerging as strategic hotspots due to demographic, economic, and policy-oriented drivers.

Asia Pacific: The Leading Growth Engine

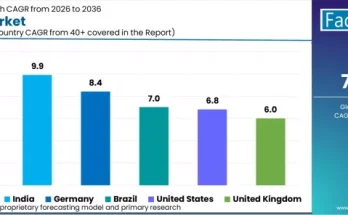

Asia Pacific remains the most dynamic and fastest-growing region in the global tractor landscape. Supported by intensive mechanization programs, government subsidies, and robust demand from smallholder farmers, this region commands a leading share of global adoption. India and China are pivotal markets:

-

India continues to be the largest tractor market by unit volumes, with domestic sales crossing historic milestones, marking continued demand resilience.

-

Mechanization levels have surged, particularly in sub-70 HP segments which represent the bulk of demand for small and mid-sized farms.

The region is forecasted to hold around 38–52% share globally, emphasizing its strategic importance for OEMs and investors alike.

North America: Technology and Scale

North America — led by the United States — stands as a mature, high-value tractor market. With advanced precision farming adoption, larger operational land use, and a growing lease/rental segment, this region emphasizes productivity and innovation. The U.S. market alone holds a substantial share of North America’s tractor revenues and continues to see traction in above-100 HP categories.

Europe: Sustainability Focus & Smart Machinery

European markets are characterized by strong regulatory support for sustainability, electrification, and emission reductions. Adoption of high-end tractors with intelligent farming features is accelerating in countries like Germany, France, and Italy, reflecting a premium market that prioritizes performance and compliance with environmental goals.

Latin America & Middle East/Africa: Emerging Potential

Latin America and the Middle East & Africa are emerging as next-wave growth arenas with improving mechanization and agricultural investments. Brazil and Argentina, for instance, are witnessing steady expansion in tractor demand across both commercial and family-owned farms.

Browse Full Report : https://www.factmr.com/report/510/tractors-market

Outlook to 2036: Strategic Imperatives

As the tractor market charts its course to 2036, several strategic themes will shape competitive advantage:

• Sustainability & Electrification: With increasing global emphasis on reducing carbon footprints, electric and hybrid tractors are set for accelerated adoption — appealing to eco-conscious farmers and regulatory frameworks.

• Smart Farming Ecosystems: Integrating tractors into digital farm ecosystems — combining data analytics, sensor networks, and autonomous operations — will differentiate leading manufacturers from laggards.

• Inclusive Financing Models: Innovative financing solutions, including leasing, pay-per-use, and microcredit structures, will unlock demand in lower-income segments and rural economies.

• Regional Customization: OEMs that tailor products to specific regional requirements — such as soil types, crop patterns, and labor availability — will outperform generic market approaches.

In conclusion, the tractor market’s journey to 2036 is defined by strategic innovation, pricing evolution, and regional diversification. As agriculture and allied sectors pursue greater productivity, efficiency, and sustainability, the tractor industry stands poised to be a cornerstone of global mechanization and economic advancement — providing fertile ground for investors, manufacturers, and policy makers to cultivate long-term value.