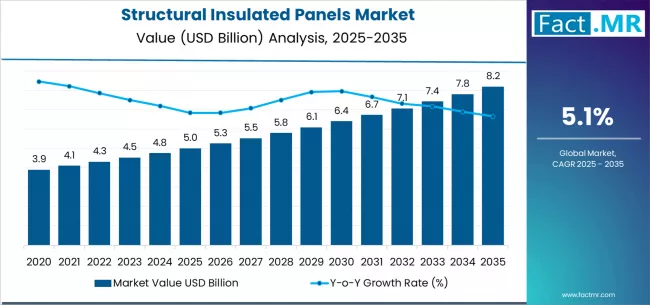

The global structural insulated panels market is poised for robust growth as the construction sector embraces sustainability, energy efficiency, and modularity. According to a recent report by Fact.MR, the market is valued at USD 5.0 billion in 2025 and is projected to reach USD 8.2 billion by 2035, recording an absolute increase of USD 3.2 billion over the forecast period. This reflects a compound annual growth rate (CAGR) of 5.1% between 2025 and 2035.

SIPs are redefining modern construction by offering high-performance insulation, reduced construction times, and superior environmental performance. As global focus intensifies on net-zero emissions and green building practices, SIPs are increasingly favored for residential, commercial, and industrial projects.

Strategic Market Drivers

- Sustainability and Energy Efficiency in Construction

The rising demand for energy-efficient and low-carbon building materials is a major growth catalyst for the SIPs market. SIPs provide superior thermal performance, reducing heating and cooling energy consumption by up to 50% compared to traditional materials.

Governments and developers are adopting SIPs to meet stringent energy codes and certification standards such as LEED and BREEAM, reinforcing their role in sustainable construction frameworks.

- Expansion of Prefabricated and Modular Construction

The growing popularity of prefabricated and modular building systems—owing to faster construction timelines, lower labor costs, and reduced waste—has significantly bolstered SIP adoption. These panels enable high-precision manufacturing and quick on-site assembly, offering design flexibility without compromising structural integrity.

- Rising Urbanization and Housing Demand

Rapid urbanization, especially in developing economies, has accelerated the need for affordable, durable, and energy-efficient housing solutions. SIPs offer a cost-effective alternative for large-scale residential projects and disaster-resilient housing, driving demand across emerging regions.

- Industrial and Cold-Chain Applications

Beyond residential and commercial use, SIPs are gaining traction in industrial cold storage and food logistics due to their excellent insulation and air-sealing properties. The expanding cold-chain infrastructure in Asia-Pacific and Latin America presents lucrative opportunities for market players.

Browse Full Report: https://www.factmr.com/report/structural-insulated-panels-market

Regional Growth Highlights

North America: Leading the Energy-Efficient Construction Revolution

North America remains the largest market for SIPs, driven by strong green building initiatives and regulatory frameworks promoting energy conservation. The U.S. and Canada are witnessing increasing adoption of SIPs in residential housing and public infrastructure projects due to their proven thermal and structural advantages.

Europe: Regulation-Driven Market Transformation

Europe’s market growth is fueled by strict environmental regulations and the region’s commitment to carbon neutrality. Countries such as Germany, the U.K., and the Netherlands are incorporating SIPs into modular and passive housing designs, supported by governmental incentives for energy-efficient materials.

East Asia: Rising Manufacturing and Smart Cities

East Asia—led by China, Japan, and South Korea—is emerging as a growth hotspot, with expanding manufacturing capabilities and smart city development. Rising disposable incomes, coupled with rapid urban infrastructure modernization, are boosting SIP adoption across commercial and residential projects.

Emerging Markets: Rapid Infrastructure Expansion

Latin America, South Asia, and the Middle East are showcasing strong potential for SIP deployment. The rise in affordable housing programs, coupled with government-backed sustainability initiatives, is driving local production and adoption of insulated panel systems.

Market Segmentation Insights

By Product Type

- EPS (Expanded Polystyrene) Panels: Most widely used for their cost-effectiveness and insulation efficiency.

- PUR/PIR (Polyurethane/Polyisocyanurate) Panels: Preferred for superior thermal resistance and moisture control.

- Mineral Wool Panels: Gaining traction in fire-resistant and soundproof applications.

By Application

- Residential Construction: Dominates the market, fueled by demand for energy-efficient and sustainable housing.

- Commercial Buildings: Growing use in office complexes, retail outlets, and educational institutions.

- Industrial and Cold Storage: Expanding utilization for temperature-controlled facilities.

Challenges and Market Considerations

Despite strong growth potential, the SIPs market faces several challenges:

- High Initial Costs: Advanced manufacturing and installation costs can deter small-scale builders.

- Design and Code Compliance: Variation in regional building codes poses integration challenges.

- Raw Material Price Fluctuations: Volatility in resin and foam prices can affect profit margins.

- Skilled Labor Shortage: Lack of expertise in SIP installation can slow adoption in emerging markets.

Competitive Landscape

The global structural insulated panels market is characterized by strategic innovations, material advancements, and growing emphasis on circular construction. Leading players are expanding production capacities, investing in automation, and developing recyclable, bio-based insulation materials to meet sustainability goals.

Key Players in the Structural Insulated Panels Market:

- Kingspan Group plc

- Owens Corning

- BASF SE

- Huntsman Corporation

- Rockwool A/S

- Armacell International S.A.

- Dow Inc.

- Alubel S.p.A.

- Metecno S.p.A.

- Puren GmbH

- Covestro AG

Recent Developments

- February 2023: Kingspan introduced a next-generation insulated panel system with integrated solar PV technology, enhancing energy generation in commercial buildings.

- October 2022: Owens Corning launched a new line of eco-friendly rigid insulation panels designed to reduce carbon footprint during production.

- September 2022: BASF unveiled high-performance polyurethane foam formulations optimized for SIP production, offering improved structural strength and fire resistance.

Future Outlook: Building the Next Era of Smart and Sustainable Construction

Over the next decade, the structural insulated panels market will play a pivotal role in shaping the future of sustainable, energy-efficient, and resilient buildings. Advancements in material science, digital design tools, and modular construction technologies will further enhance performance and scalability.

As the global construction industry transitions toward low-carbon, high-efficiency solutions, SIPs are expected to become an integral component of modern architecture.

Manufacturers prioritizing innovation, recyclability, and digital integration will lead the next phase of growth—building smarter, greener, and more energy-resilient structures worldwide.