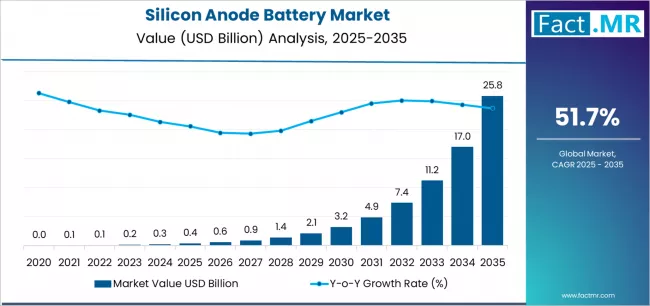

By 2035, the global market for silicon anode batteries is expected to reach USD 25.8 billion, representing an absolute rise of USD 25.4 billion during that time. The market is expected to grow at a compound annual growth rate (CAGR) of 51.7% during the assessment period, with a valuation of USD 0.4 billion in 2025.

Silicon-anode batteries – lithium-ion cells that incorporate silicon or silicon-based composites in the anode in place of, or alongside, graphite – are emerging as a major next-generation battery technology. Silicon’s theoretical capacity is far higher than graphite’s, offering the promise of substantially greater energy density, faster charging, and longer driving range for electric vehicles (EVs), as well as improved runtimes for consumer electronics and denser energy storage for grid applications. Recent advances in materials engineering and cell design have accelerated commercialization efforts, moving silicon anode technology from lab demonstrations toward scaled production.

Quick Stats (2025-2035)

Estimated Market Value 2025: Approximately USD 0.4 billion

Forecast Market Value 2035: Approximately USD 25.8 billion

Absolute Growth (2025-2035): ~ USD 25.4 billion

Forecast CAGR (2025-2035): Very high – in the range of dozens of percent annually as technology scales

Primary Early Applications (2025): Consumer electronics and specialty EV modules

Targeted Major Application by 2035: Broad EV battery packs, high-energy portable devices, and grid/storage modules

To Access the Complete Data Tables & in-depth Insights, Request a Discount on this report: https://www.factmr.com/connectus/sample?flag=S&rep_id=12409

Key Market Drivers

1. Need for Higher Energy Density & Longer Range

Automakers demand batteries that extend vehicle range without increasing pack size or weight. Silicon anodes can increase cell-level energy density, helping EVs achieve longer driving ranges or smaller, lighter battery packs.

2. Faster Charging Requirements

Silicon-based anodes can support higher charge rates in some designs, enabling shorter charging times – a critical consumer pain point for EV uptake and a key selling point for premium electronics.

3. Consumer Electronics Miniaturization

Smartphones, laptops, wearables, and portable tools benefit from every percent of energy-density improvement; silicon anodes present a pathway to thinner devices with longer battery life.

4. Renewable Integration & Energy Storage Growth

Grid-scale and behind-the-meter energy storage demand higher capacity and cost-efficient batteries; silicon-anode technologies promise eventual cost and performance benefits for storage systems.

5. Manufacturing Investment & Material Innovation

Investment into silicon composites, nano-structuring, better binders and electrolytes, and scalable electrode processes is reducing historical performance gaps and enabling pilot production lines.

Market Structure & Segment Insights

By Technology / Material Approach

Silicon-Carbon Composites: Blends that mitigate expansion and improve cycle life – dominant near-term commercial approach.

Nano-Structured Silicon: High performance at lab scale; more complex to scale but offers top-tier capacity gains.

Silicon Oxide / Silicon Alloy Variants: Offer varying tradeoffs between capacity, stability, and manufacturability.

By Application

Electric Vehicles: Long-term largest demand driver if cycle-life and cost targets are met; early adoption in premium and specialty EVs.

Consumer Electronics: Early commercial adoption for high-end devices and wearables seeking energy gains.

Energy Storage Systems: Mid-to-long term opportunity contingent on cost-per-kWh and longevity metrics.

Industrial & Tools: Power tools and industrial devices needing compact, high-power packs will use silicon-enhanced cells.

By Region

Asia-Pacific: Leading in manufacturing scale and early deployment given established battery supply chains.

North America & Europe: Strong demand from EV makers, policy incentives, and R&D investment; likely early adopters for automotive integration.

Rest of World: Adoption follows global EV and electronics market growth patterns.

Challenges & Restraints

Volume Expansion & Mechanical Degradation: Silicon swells during lithiation, causing particle fracture and capacity fade – the most significant technical hurdle.

Cycle Life & Calendar Life: Matching graphite’s multi-thousand cycle durability remains challenging for many silicon formulations.

Manufacturing Complexity & Cost: High-purity silicon materials, advanced binders, and intricate electrode architectures can add cost and process complexity.

Electrolyte Compatibility & SEI Formation: Stable solid-electrolyte interphase control is essential; electrolyte formulations require optimization for silicon chemistry.

Scale-Up Risk: Moving from pilot lines to gigafactory production demands reproducible processes, supply of precursors, and quality control investments.

Opportunities & Strategic Directions

Composite & Hybrid Anode Strategies – Combining silicon fractions with graphite to balance capacity and longevity for near-term commercial cells.

Advanced Binders & Electrolytes – Proprietary chemistries that stabilize silicon particles and extend cycle life.

Cell-to-Pack and Modular Designs – Architectural improvements that leverage silicon’s advantages with minimal system redesign.

Vertical Integration & Supply Partnerships – Securing high-quality silicon feedstocks and scaling pilot plants to control costs.

Niche Early Markets – Premium electronics, aerospace, and specialty EV segments where price can be justified by performance gains.

Outlook

Silicon-anode batteries are poised for transformative growth as technical challenges are progressively solved and manufacturing scales. From a modest market presence in 2025, silicon-enhanced cells could become mainstream in multiple sectors by 2035, delivering meaningful increases in energy density, faster charge rates, and new form-factor possibilities. Success hinges on continued materials innovation, cost reductions through scale, and demonstrable cycle-life parity in targeted applications. Companies that master reliable, scalable silicon anode supply chains and offer proven cell longevity will capture the most value as the market shifts toward higher-performance battery chemistries.

Browse Full Report: https://www.factmr.com/report/silicon-anode-battery-market