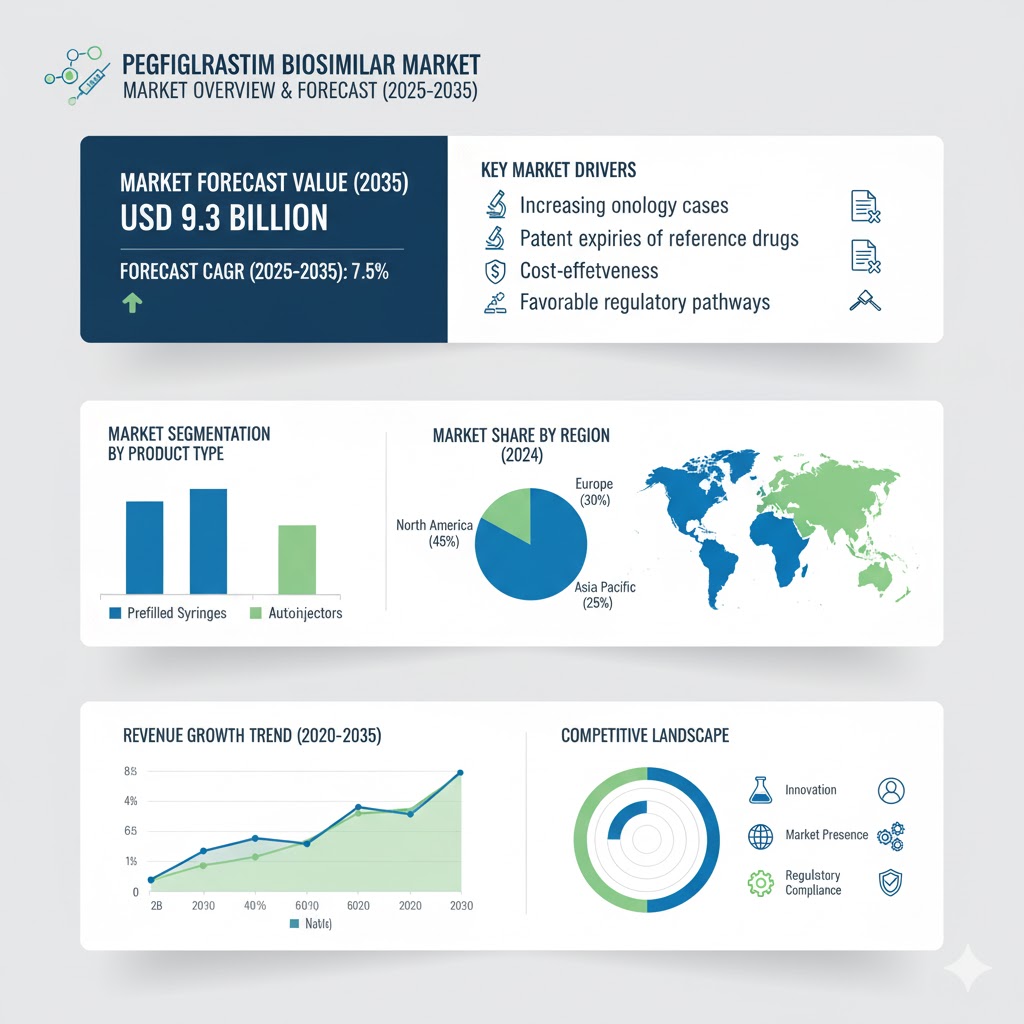

The global pegfilgrastim biosimilar market is on a strong growth trajectory, fueled by increasing demand for cost-effective biologics in oncology, rising cancer prevalence, and broader adoption of supportive care therapies. Valued at USD 4.5 billion in 2025, the market is projected to reach USD 9.3 billion by 2035, recording an absolute increase of USD 4.8 billion and reflecting a CAGR of 7.5% over the forecast period.

Market Drivers: Rising Cancer Incidence, Cost-Efficient Therapeutics, and Biosimilar Acceptance

Expanding Oncology Treatments and Supportive Care Needs

The increasing prevalence of cancer globally has created significant demand for granulocyte colony-stimulating factors (G-CSFs) like pegfilgrastim to reduce chemotherapy-induced neutropenia. Biosimilars offer equivalent efficacy at lower costs, enhancing patient access and enabling hospitals and clinics to optimize oncology treatment protocols.

Regulatory Approvals and Market Penetration

Regulatory bodies across North America, Europe, and Asia-Pacific are progressively approving pegfilgrastim biosimilars, allowing faster market penetration. Healthcare providers are increasingly adopting biosimilars due to proven clinical equivalence, affordability, and insurance reimbursement support.

Technological Advancements and Manufacturing Efficiencies

Advances in biologic production, including enhanced cell line engineering and process optimization, are improving biosimilar quality and reducing production costs. Coupled with strategic partnerships, licensing, and collaborations, these innovations are accelerating the adoption of pegfilgrastim biosimilars in both developed and emerging markets.

Competitive Landscape

The pegfilgrastim biosimilar market is highly competitive, with leading pharmaceutical and biotech companies focusing on product innovation, global regulatory approvals, and expansion into new markets.

Key Players in the Pegfilgrastim Biosimilar Market include:

- Viatris Inc./Biocon Biologics Ltd.

- Sandoz International GmbH

- Coherus BioSciences Inc.

- Fresenius Kabi AG

- Pfizer Inc.

- Teva Pharmaceutical Industries Ltd.

- Celltrion Inc.

- Samsung Bioepis Co. Ltd.

- Mundipharma International Ltd.

These companies are advancing product pipelines, strengthening manufacturing capabilities, and expanding collaborations with hospitals and oncology centers to enhance clinical adoption and patient reach. Strategic initiatives include regulatory clearances, acquisitions, and partnerships with telemedicine platforms.

Recent Developments

- 2025 – FDA approved additional pegfilgrastim biosimilars with reduced dosing schedules, improving patient convenience and adherence.

- 2024 – European Medicines Agency (EMA) granted market authorization to multiple pegfilgrastim biosimilars, expanding access across EU countries.

Segmentation of the Pegfilgrastim Biosimilar Market

The market is segmented by product type, patient type, distribution channel, and region. By product, the market is dominated by prefilled syringes and on-body injector devices, designed for ease of administration. In terms of patient type, oncology patients undergoing chemotherapy represent the primary end-users. Distribution channels include hospitals, specialty pharmacies, and online channels, with hospitals leading adoption due to clinical oversight, while pharmacies and e-commerce platforms are expanding market accessibility.

Regional Outlook

- North America – Leading the market due to high cancer prevalence, robust healthcare infrastructure, and early adoption of biosimilars.

- Europe – Growth driven by favorable reimbursement policies, regulatory support, and clinical adoption.

- Asia-Pacific – Fastest-growing region, fueled by rising cancer incidence, improving healthcare access, and affordability.

Future Outlook: Advanced and Accessible Biosimilar Therapies

Over the next decade, the pegfilgrastim biosimilar market will witness:

- Expanded patient access through cost-effective and convenient delivery systems.

- Enhanced clinical outcomes with longer-acting and user-friendly devices.

- Broader adoption in emerging markets via regulatory support and partnerships.

By 2035, the pegfilgrastim biosimilar market will transform supportive oncology care, offering safer, more affordable, and patient-centric treatment solutions.