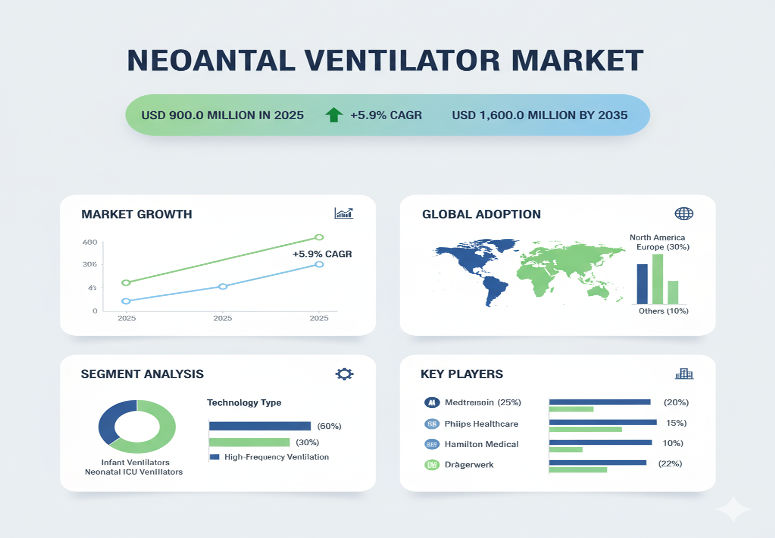

The global neonatal ventilator market is at an inflection point. In 2025, the market is estimated at US$ 900 million, and by 2035 it is forecast to reach approximately US$ 1.60 billion, growing at a compound annual growth rate (CAGR) of about 5.9% over the decade. This growth reflects expanding neonatal intensive-care unit (NICU) capacity, rising incidence of pre-term births and respiratory distress in newborns, and accelerating innovation in ventilation technologies tailored for neonates.

Driving Forces Behind the Growth

Several key trends are driving this market forward. First, the incidence of neonatal respiratory conditions—including respiratory distress syndrome (RDS), bronchopulmonary dysplasia (BPD), and other complications of prematurity—is increasing, particularly in emerging economies. Having access to advanced ventilation equipment is becoming a priority for neonatal care.

Second, healthcare infrastructure investment is rising globally, especially in NICUs and tertiary care centres. Hospitals are upgrading from generic ventilators to dedicated neonatal ventilator systems with fine-tuned compliance, small tidal-volume support, advanced alarms and monitoring—creating demand for specialist devices rather than off-the-shelf adult systems.

Third, technological innovation is accelerating. Features such as non-invasive ventilation modes, high-frequency oscillatory ventilation, advanced sensors and analytics, real-time monitoring, and modular designs for twin/quad care are gaining ground. These allow better safety, lower lung-injury risk and improved outcomes in neonates.

Finally, regulatory and quality-care benchmarks are becoming more stringent. Hospitals and care systems are under pressure to reduce neonatal morbidity and mortality, driving investment in ventilator technologies that offer precision, reliability and integration with modern NICU infrastructure.

Segmentation & Key Market Insights

By type of ventilation: Invasive ventilation remains dominant, accounting for ~58% of the market share in 2025, as many preterm or critically ill neonates require endotracheal intubation and controlled ventilation. However, non-invasive ventilation systems (nasal CPAP, nasal high-flow, non-invasive ventilators) are growing faster as lung-protective strategies become standard.

By end-use setting: Hospitals, particularly NICUs in tertiary and main hospitals, hold the lion’s share—around 72% in 2025—pointing to the predominance of institutional care settings for neonatal ventilation. Clinics and smaller outpatient settings play a smaller role but are gaining relevance in some regional markets.

By region: Strong growth is expected across multiple geographies. North America and Europe remain mature and continue to invest in upgrading NICU infrastructure. Asia-Pacific is a key high-growth region, owing to expanding healthcare investment, rising birth rates (including pre-term births), and increasing availability of advanced neonatal technologies in hospitals. Within Europe, countries such as Germany, France and the UK are leading in adoption, while in Asia-Pacific, China and India stand out.

Competitive Landscape & Major Players

The neonatal ventilator market is moderately concentrated, with top players accounting for approximately 45-50% of global volume. Leading companies include Dräger, GE HealthCare, Medtronic, Vyaire, Mindray, Philips, Hamilton Medical, Fritz Stephan, Inspiration Healthcare and Nihon Kohden.

These companies differentiate on key dimensions: ventilation precision for neonates, small-volume tidal support, compact footprint, user-friendly interface, connectivity with NICU systems, service/support infrastructure and regional presence. They are also increasingly focusing on partnerships with hospitals for training, monitoring and lifecycle management of ventilation systems.

Recent Developments & Innovation Highlights

Recent years have introduced several noteworthy developments in neonatal ventilation. Some manufacturers are releasing true twin-patient ventilators enabling one ventilator to serve two neonates safely—a relevant innovation for cost-constrained hospitals. Others are introducing non-invasive ventilators with improved synchrony and lower lung-injury risk, aligning with modern neonatal ventilation protocols. Tele-monitoring, integration of ventilation data into NICU dashboards and analytics to predict weaning readiness or detect adverse events are also gaining traction.

From a service perspective, companies are offering bundled solutions: ventilator equipment, training, maintenance contracts, consumables tracking and remote diagnostics—helping hospitals manage total cost of ownership. On the geographic front, manufacturers are strengthening distribution and support in emerging markets (Southeast Asia, Latin America, Middle East) where neonatal care upgrades are underway.

Challenges & Market Barriers

Despite the positive outlook, some obstacles remain. The high cost of advanced neonatal ventilators is a barrier in low-income and many middle-income countries. Also, skilled personnel and training for neonatal ventilation are lacking in some regions, limiting uptake. Variability in reimbursement and procurement cycles in hospitals adds complexity. Technical challenges such as ensuring ultra-low tidal-volume precision, minimizing ventilator-associated lung injury, and designing for multiple ventilation modes (invasive, non-invasive, high-frequency) increase R&D cost. Finally, regulatory requirements vary across regions—compliance with neonatal-specific standards adds time and cost to product launch.

Forecast & Strategic Implications

From 2025 to 2035, the neonatal ventilator market is set to grow from US$ 900 million to US$ 1.60 billion—an increase of approximately US$ 700 million. This nearly doubling of market size underscores steady expansion rather than explosive growth, making this a mature-but-growing segment of critical-care devices.

For manufacturers and stakeholders, strategic imperatives include:

-

Targeting emerging markets where NICU expansion offers most growth potential—not just mature economies.

-

Developing modular, cost-effective ventilator systems that meet neonatal requirements while lowering total cost of ownership.

-

Offering service and training bundles to support hospitals with neonatal ventilation expertise and lifecycle management.

-

Focusing on lung-protective, non-invasive ventilator modes and data-analytics integration, to align with evolving clinical protocols and differentiate offerings.

-

Localizing production or service support in key growth regions to reduce cost, speed delivery and enhance support.

Browse Full Report: https://www.factmr.com/report/758/neonatal-ventilator-market

Editorial Perspective

While the neonatal ventilator market may not enjoy the massive headline growth of some other medical-device segments, it occupies a critical and indispensable niche. For the most vulnerable patients—newborns with compromised lungs—the right ventilator system can mean better survival, fewer complications and faster recovery. Hospitals and health systems are increasingly focused on outcomes metrics, NICU performance and neonatal care standards—and that focus filters into device procurement decisions.

In this context, companies that combine neonatal-specific ventilation innovation, excellent clinical support, service reliability and global market reach will lead. The coming decade offers meaningful growth, and although the figures may not skyrocket, steady expansion and improved clinical outcomes make this market one of the most socially important in medical devices.