The global industrial landscape is witnessing a quiet but essential shift toward chemical efficiency and environmental compliance. At the heart of this movement is Ferrous Sulfate, a versatile workhorse driving innovation in water treatment, sustainable agriculture, and pharmaceuticals.

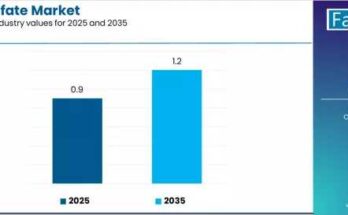

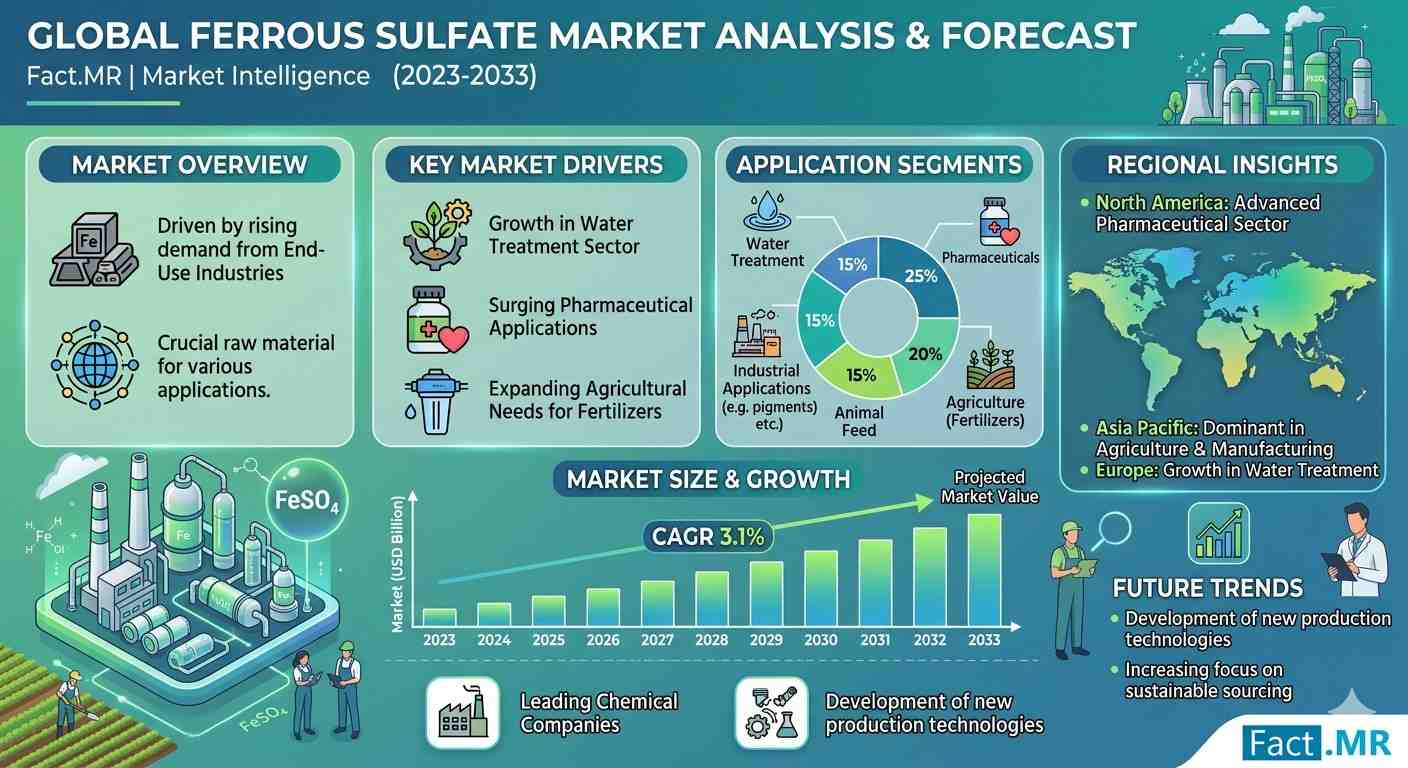

According to the latest market outlook, the global ferrous sulfate market is valued at USD 0.9 billion in 2025 and is projected to reach USD 1.2 billion by 2035. This represents a steady 2.9% CAGR, underpinned by a 33.3% absolute increase in market value over the next decade. For decision-makers, this 1.33X growth trajectory signals a robust demand for high-purity chemical solutions that balance operational performance with increasingly stringent environmental mandates.

Quick Stats: Market Vitality (2025–2035)

| Metric | Details |

| Market Value (2025E) | USD 0.9 Billion |

| Projected Value (2035F) | USD 1.2 Billion |

| Total Growth (10-Year) | 33.3% |

| Dominant Form | Heptahydrate (58% Market Share) |

| Primary Distribution | B2B Bulk (74% Market Share) |

| Top Growth Region | USA (3.3% CAGR) |

Strategic Drivers: Water, Wealth, and Wellness

The expansion of the ferrous sulfate market is being carved out by three distinct industrial imperatives:

- The Water Treatment Standard (37% Share): As urbanization accelerates, municipal and industrial wastewater facilities are pivoting to ferrous sulfate as a primary coagulant. Its exceptional reactivity and ability to remove contaminants while maintaining pH balance make it indispensable for environmental compliance.

- Precision Agriculture & Animal Nutrition: There is a growing emphasis on “iron-rich” additives to combat soil depletion and livestock health issues. Modern producers are integrating ferrous sulfate into specialized feed formulations to ensure consistent nutritional outcomes.

- Pharmaceutical Grade Innovation: Beyond industrial use, the development of high-purity pharmaceutical formulations for iron deficiency treatment is creating a premium market segment with higher margins and differentiated chemical propositions.

Segmental Leadership: Heptahydrate & Bulk Distribution

- Heptahydrate (The Preferred Form): Projected to maintain a 58% market share in 2025, the heptahydrate form remains the industry favorite due to its superior solubility and stability in demanding processing environments.

- B2B Bulk (The Supply Backbone): Commanding 74% of sales, bulk distribution is the engine of the market. Large-scale industrial buyers prioritize the cost advantages and supply reliability that only integrated bulk logistics can provide.

Global Analysis: The 3.3% American Surge

While growth is global, the USA is leading the charge with a 3.3% CAGR. This is driven by a dual-track strategy: the modernization of aging water infrastructure and a booming agricultural sector in the Midwest.

- Mexico (3.0% CAGR): Rapidly emerging as a North American chemical processing hub.

- Germany (2.7% CAGR): Leading the way in “Environmental Technology,” focusing on high-specification grades for European compliance.

- East Asia: South Korea (2.4%) and Japan (2.3%) are prioritizing “Quality Excellence,” focusing on specialized chemical applications in the tech and pharma sectors.

Browse Full Report –

https://www.factmr.com/report/1954/ferrous-sulfate-market