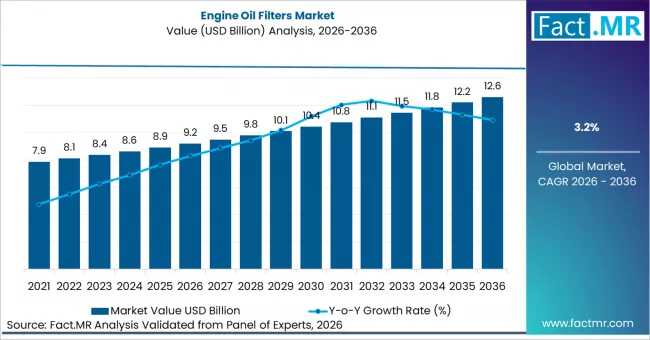

The global Engine Oil Filters Market is accelerating toward a projected valuation of USD 12.6 billion by 2036, rising from USD 9.2 billion in 2026. Navigating a steady 3.2% CAGR, the industry is undergoing a technical renaissance as automotive engineers prioritize “oil cleanliness” as the primary defense for high-performance, modern engines.

As service intervals extend and engine tolerances tighten, the humble oil filter has evolved into a sophisticated multi-layer protection module. From cold-start flow management to anti-drainback valves that maintain lubrication integrity during shutdown, today’s filtration systems are mission-critical components for both conventional and next-generation powertrains.

Quick Stats: Market at a Glance

- 2026 Estimated Value: USD 9.2 Billion

- 2036 Forecast Value: USD 12.6 Billion

- Compound Annual Growth Rate (CAGR):2%

- Leading Filter Type: Spin-On Filters (48.4% share)

- Primary Media Type: Cellulose Media (50.6% share)

- Top Growth Engine: India (4.5% CAGR)

The Engineering Edge: Spin-On Dominance and Media Evolution

Spin-On Filters continue to lead the market with a 48.4% share, favored by both OEMs and maintenance professionals for their “service efficiency” and proven sealing infrastructure. However, the internal technology is shifting; advanced housings now resist extreme pressure fluctuations while multi-layer media capture microscopic contaminants that previously bypassed standard systems.

While Cellulose Media remains the cost-effective industry standard with a 50.6% share, there is a rising trajectory for synthetic and blended media. These materials allow for “smart” flow resistance that adjusts based on oil viscosity and temperature—ensuring optimal filtration from the moment the ignition turns over.

Global Growth: Maintenance Consciousness & Regulatory Rigor

The market’s geographic momentum is increasingly dictated by regional maintenance habits and emission mandates:

- India: Leading global growth with a 5% CAGR, driven by a massive expansion in automotive manufacturing and a burgeoning middle class prioritizing vehicle longevity.

- China: Projected at a 0% CAGR, as the country’s advanced automotive infrastructure integrates specialized filtration systems to meet stricter emission standards.

- United States: Growing at 1%, where the focus is on premium aftermarket services and SAE J1858-certified performance.

- Germany & Japan: These high-precision markets focus on maintenance technology excellence, with growth tied to the integration of filters into complex, highly regulated vehicle lubrication systems.

Competitive Landscape

The market is anchored by filtration titans including MANN+HUMMEL Group, MAHLE GmbH, Robert Bosch GmbH, Denso Corporation, and Donaldson Company. These players are differentiating through “integration”—developing bypass valve systems and high-durability housings that align with Global Technical Regulations (GTR). Competition is increasingly focused on the aftermarket channel, where brand reputation for engine protection and compliance with ISO 4548 standards are the primary drivers of consumer choice.

Industry Note: Compliance is no longer optional. With certifications like ISO/TS 16949 becoming standard, the ability to demonstrate filtration efficiency under varied operational loads is the ultimate benchmark for market leaders.

Browse Full Report –

https://www.factmr.com/report/engine-oil-filters-market