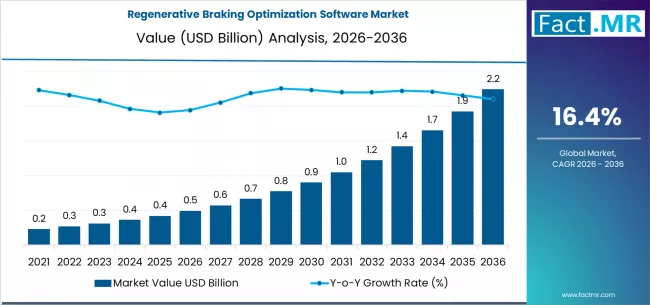

The global automotive landscape is undergoing a seismic shift toward electrification, and at the heart of this transition lies the need for unparalleled energy efficiency. A new comprehensive industry analysis reveals that the Regenerative Braking Optimization Software Market is poised for explosive growth, projected to surge from USD 0.49 billion in 2026 to USD 1.91 billion by 2036.

This trajectory represents a remarkable CAGR of 16.4%, reflecting a total market expansion of 289.8% over the next decade. As Original Equipment Manufacturers (OEMs) race to extend battery range and optimize vehicle performance, sophisticated software that fine-tunes energy recovery has moved from a “value-add” to a core engineering necessity.

The Power of Recovery: Energy Maximization Leads the Charge

Efficiency is no longer just about the battery cell; it is about the intelligence managing the halt. The Energy Recovery Maximization segment is set to dominate the market, accounting for 39.1% of the total share in 2026. These systems enable manufacturers to deliver enhanced battery efficiency and comprehensive energy management, ensuring consistent performance across diverse driving environments.

Quick Stats: Market at a Glance

-

2026 Estimated Valuation: USD 0.49 Billion

-

2036 Projected Valuation: USD 1.91 Billion

-

Compound Annual Growth Rate (CAGR): 16.4%

-

Dominant Customer Segment: OEMs (62.1% Market Share)

-

Lead Optimization Focus: Energy Recovery Maximization (39.1% Share)

Strategic Growth Drivers and Innovation Trends

The push for automotive electrification is governed by more than just consumer preference; it is driven by rigorous regulatory frameworks and the pursuit of operational excellence.

-

OEM Dominance: Vehicle manufacturers (OEMs) hold a commanding 62.1% share of the market. This underscores their critical role in integrating standardized performance procedures and advanced energy recovery protocols directly into the vehicle’s DNA.

-

Automated Configurations: A key emerging trend is the shift toward automated energy recovery configurations. These systems minimize the need for manual operational adjustments, effectively reducing deployment costs and complexity for fleet managers.

-

Multi-Parameter Compatibility: Modern software is evolving to support “Hybrid” and “Cloud Analytics” deployments, allowing for real-time adjustments based on driver behavior models, traffic prediction, and thermal data inputs.

Regional Outlook: China and Brazil Outpace Global Average

While North America and Europe remain established hubs for automotive innovation, the highest growth rates are emerging from developing infrastructures.

-

China: Projected to lead with an exceptional 19.4% CAGR. The country’s rapid EV infrastructure expansion and aggressive regulatory promoting vehicle efficiency make it a goldmine for software providers.

-

Brazil: Following closely with a 19.1% CAGR, driven by rising automotive investment and a growing consciousness regarding specialized performance equipment.

-

United States: Maintaining a steady 15.5% CAGR, fueled by a high demand for operational precision and advanced technology integration.

Competitive Landscape

The market is characterized by a high-stakes race between established automotive tech giants and specialized software innovators. Tier-1 suppliers and tech leaders are investing heavily in specialized performance platforms to secure their heritage in the electric era.

Prominent players shaping the industry include:

-

Bosch

-

Continental

-

Aptiv

-

NVIDIA

-

Siemens

-

MathWorks

-

dSPACE

-

AVL

-

ZF

-

Valeo