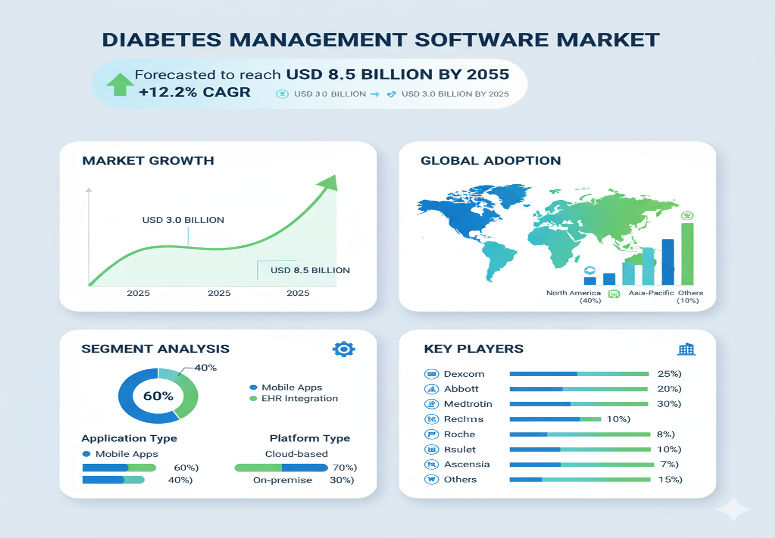

The global diabetes management software market is estimated at US$ 25.85 billion in 2022, and is projected to reach approximately US$ 66.26 billion by 2032, reflecting a compound annual growth rate (CAGR) of about 9.9%. This robust expansion underscores how the intersection of rising diabetes prevalence, digital health innovation, consumer-centric care, and value-based healthcare models is reshaping diabetes management—from reactive clinic visits to continuous, data-driven care.

Why the Market Is Accelerating

Multiple converging forces are driving growth in diabetes management software. First and foremost is the very large and growing global burden of diabetes—both Type 1 and Type 2—as personalized care models seek to reduce complications, hospitalizations, and costs.

Second, the proliferation of connected and wearable technologies (continuous glucose monitors, insulin pumps, smart pens, mobile apps) and cloud-based platforms enables real-time data collection, trend analysis, and remote monitoring. These digital tools go hand-in-hand with software platforms that provide feedback loops for patients and clinicians.

Third, patient expectations have shifted: modern users demand convenience, self-management capability, seamless connectivity, and actionable insights—especially in home and ambulatory settings.

Fourth, healthcare systems and payers are increasingly recognizing that software-driven management can improve outcomes and reduce long-term costs, which supports adoption and reimbursement.

Segmentation & Core Applications

By device type, the market is broadly segmented into wearable devices and handheld devices. Wearables—such as continuous glucose monitors and smart delivery systems—tend to dominate because they offer continuous monitoring, remote connectivity, and integration with software platforms. Handheld devices (glucometers, mobile apps) retain relevance, especially in self-care and lower-cost segments where simplicity and affordability matter most.

In terms of application, the two major categories are diabetes & blood-glucose tracking and obesity & diet-management. The glucose-tracking segment remains the largest share, as maintaining glycemic control is foundational in diabetes care. The diet & obesity segment is gaining traction, given the rise of metabolic syndrome, pre-diabetes, and lifestyle-oriented management. Usage is increasingly moving beyond simply monitoring to proactive management—alerts, analytics, behavioral nudges, and integrated care pathways.

From the end-user perspective, the major segments include self/home healthcare, hospitals & specialty diabetes clinics, and academic & research institutes. Self-care/home use is growing rapidly as digital health matures and patients seek more autonomy. Hospitals and specialty clinics continue to drive enterprise deployments of connected software platforms linked to device ecosystems.

Regional Insights: North America & Europe Take Early Lead

North America leads the market, representing roughly 32.6% share in 2022. Mature healthcare ecosystems, favorable reimbursement policies, high smartphone and wearable penetration, and strong digital health investment underpin growth in the U.S. and Canada.

Europe follows with about 28.6% share, supported by rising incidence of diabetes, strong consumer awareness, and increasing adoption of digital health solutions in Western Europe. Growth is robust but slightly constrained by regulatory complexity and diverse healthcare systems across countries.

Asia-Pacific, Latin America, and the Middle East & Africa represent high-potential growth zones going forward. In these regions, rising diabetes prevalence, expanding healthcare infrastructure, increasing smartphone penetration, and policy initiatives around e-health are creating favorable conditions for market growth.

Key Players & Competitive Dynamics

The competitive landscape of the diabetes management software market features specialist digital-health providers, device ecosystem players, and large medical-technology and pharmaceutical companies. Among the leading firms are Glooko, Tidepool, LifeScan, Inc., Ascensia Diabetes Care Holdings AG, Abbott Diabetes Care, Acon Diabetes Care International, BIONIME, CustoMed, and Dexcom.

These companies differentiate by software capabilities (analytics, AI-based prediction, trend modeling), device integration (glucose monitors, insulin delivery, mobile apps), engagement features (alerts, coaching, remote clinician connectivity), regulatory approval (medical-grade software), and business models (subscription, device-software bundles, platform licensing).

Partnerships and strategic acquisitions are common: smaller digital-health start-ups often join forces with larger med-tech firms to scale distribution and access to clinical data.

Trends & Innovation Highlights

Several emerging trends are shaping market evolution.

-

Predictive analytics and digital biomarkers: Software platforms increasingly use large datasets to forecast glycemic excursions, risk of hypoglycemia, and to personalize care pathways.

-

Closed-loop systems: Integration of monitoring, analytics, and insulin delivery into automated systems is advancing.

-

Remote monitoring and telehealth integration: Software that links patients, clinicians, and devices at home is growing rapidly, especially post-COVID.

-

Subscription-based care models: Software is evolving from a one-time purchase to a continuous service supporting diabetes management, adherence, and outcomes.

Challenges & Restraints

Despite promising growth, there are notable barriers. The cost of advanced software and connected devices can limit uptake in price-sensitive markets. Data-security and privacy concerns, regulatory compliance for medical-grade software, interoperability across devices and platforms, and clinician workflow integration remain complex.

In many emerging markets, awareness and digital-health infrastructure are still developing, slowing adoption. Furthermore, demonstrating clinical-outcome improvements and convincing payers of cost savings remain ongoing challenges.

Strategic Outlook & Recommendations

Looking ahead to 2032 and beyond, the diabetes management software market is poised for sustained growth. Companies and stakeholders should prioritize:

-

Building platforms that support end-to-end diabetes care—monitoring, analytics, intervention, adherence tracking, and outcomes measurement.

-

Expanding footprints in emerging markets via affordable solutions, mobile-first approaches, and partnerships with local healthcare systems.

-

Strengthening interoperability—ensuring software can work with diverse devices and data sources (wearables, glucometers, electronic medical records).

-

Leveraging AI and predictive analytics to deliver more personalized and proactive diabetes care.

-

Focusing on value-based models to demonstrate improved outcomes and cost savings from software interventions.

Browse Full Report: https://www.factmr.com/report/431/diabetes-management-software-market

Editorial Perspective

The diabetes management software market exemplifies how digital health is transforming chronic-care management from episodic to continuous models. For patients living with diabetes, real-time feedback, trend insights, and connected care mean better control, fewer complications, and higher quality of life.

For healthcare systems, the promise is improved outcomes and cost containment. The companies that succeed will be those offering seamless, scalable, clinically validated platforms that patients and clinicians trust—and that deliver measurable value. In a world where the diabetes burden continues to grow, digital tools are not optional—they are increasingly essential.