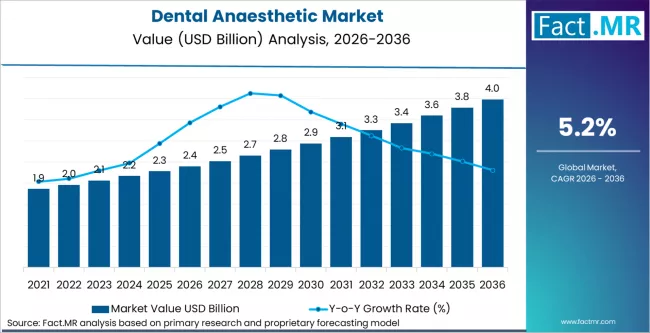

The global dental anaesthetic market is projected to reach a valuation of USD 2.4 billion in 2026, expanding to USD 3.9 billion by 2036. This steady growth, represented by a CAGR of 5.2%, is fueled by rising dental procedure volumes among aging global populations and a shift toward premium articaine formulations. The market is expected to generate an absolute dollar opportunity of USD 1.5 billion over the ten-year forecast period.

Dental Anaesthetic Market Quick Stats :

- Market size 2026? Estimated at USD 2.4 billion.

- Market size 2036? Forecasted to reach USD 3.9 billion.

- CAGR? A steady compound annual growth rate of 5.2% from 2026 to 2036.

- Leading product segment and share? Lidocaine holds the primary share at 31% in 2026.

- Leading administration method and share? Local infiltration leads the market with a 38% share.

- Leading duration of action and share? Medium-duration agents dominate with a 52% share.

- Key growth regions? Asia Pacific (led by China and India), North America, and Europe.

- Top companies? Dentsply Sirona, Laboratorios Inibsa, Pierre Pharma, Septodont, Laboratorios Normon, Primex Pharmaceuticals, Aspen Group, Dentalhitec, and Zeyco.

Market Momentum (YoY Path)

The trajectory of the Dental Anaesthetic Market shows consistent value appreciation through the next decade. Starting at USD 2.4 billion in 2026, the market is anticipated to climb to USD 2.6 billion by 2028. By 2030, the valuation is expected to hit USD 2.9 billion, reaching USD 3.1 billion in 2031. Continued adoption of advanced delivery systems will push the market to USD 3.4 billion by 2033, finally achieving the USD 3.9 billion mark by the end of 2036.

Why the Market is Growing

Expansion is primarily driven by the rising prevalence of dental diseases and an aging global demographic requiring more frequent restorative and surgical interventions. Government-led oral health initiatives, particularly in emerging economies, are broadening access to care. Furthermore, the clinical transition from legacy lidocaine to premium agents like articaine, alongside the integration of computer-controlled anaesthetic delivery systems (CCLAD), is increasing the average spend per dental procedure.

Segment Spotlight

1) Product Type

Lidocaine is estimated to maintain a 31% share in 2026. Its dominance is rooted in a long clinical history, wide formulary inclusion, and cost-effectiveness for large-scale procurement. However, articaine is seeing rapid growth as European and Asian dental associations increasingly favor its use in complex procedures like implantology.

2) Mode of Administration

Local infiltration accounts for 38% of the market share in 2026. As the standard technique for routine restorative work, its high volume is bolstered by the rise of needle-free and safety-engineered injection systems designed to improve patient comfort and clinical safety.

3) Duration of Action

Medium-duration agents hold a 52% share, as they align perfectly with the timeframe of typical dental treatments. This segment remains the staple for endodontic and periodontal procedures where sustained pain management is required without the prolonged recovery time of long-acting alternatives.

Drivers, Opportunities, Trends, Challenges

Drivers: The WHO Global Oral Health Action Plan (2023-2030) and national programs in China and India are fundamental catalysts. These initiatives aim for universal access to pain-free treatment, significantly increasing the institutional procurement of anaesthetic cartridges for public healthcare facilities.

Opportunities: The rise of Dental Service Organisations (DSOs) in North America, now managing 25% of US dental offices, presents a major opportunity for centralized supply agreements. Manufacturers can secure long-term growth by aligning with these consolidated procurement entities.

Trends: A significant shift toward Digital Dentistry is emerging. Recent innovations include AI-enabled workflows and buffering systems, such as the single-use sodium bicarbonate capsules launched in 2025, which reduce injection discomfort and improve the overall patient experience.

Challenges: The market faces structural constraints including intense generic competition that compresses cartridge pricing. Additionally, a shortage of dentists in low-income regions and medical concerns regarding epinephrine vasoconstrictors in compromised patients can moderate potential uptake.

Country Growth Outlook (CAGR)

| Country | CAGR (2026-2036) |

| China | 7.5% |

| India | 6.9% |

| Germany | 6.2% |

| Brazil | 5.8% |

| USA | 5.0% |

| UK | 4.8% |

Browse Full Report : https://www.factmr.com/report/dental-anaesthetic-market

Competitive Landscape

The global dental anaesthetic market is moderately concentrated, with Septodont, Dentsply Sirona, and Laboratorios Inibsa collectively controlling 55-60% of branded revenue. Competition is increasingly defined by vertical integration; manufacturers like Septodont and Inibsa utilize dedicated pharmaceutical facilities to ensure supply reliability. Dentsply Sirona leverages a unique advantage by bundling its anaesthetic consumables with advanced hardware and digital dentistry platforms.