The global automotive oil pans market is set for steady expansion over the next decade, supported by consistent vehicle production, rising emphasis on engine protection, and the gradual shift toward lightweight and durable materials. According to an analysis by Fact.MR, the market is projected to grow from USD 1.7 billion in 2025 to USD 2.0 billion by 2035, registering a CAGR of 1.6% during the forecast period.

This measured growth reflects sustained adoption of advanced oil pan technologies across aluminum applications, steel formulations, and composite material systems.

Modern powertrains, stricter emission norms, and OEM focus on durability and thermal efficiency are reinforcing the importance of high-performance oil pans in both passenger and commercial vehicles.

Strategic Market Drivers

Engine Protection and Thermal Management Remain Core Demand Factors

Automotive oil pans play a critical role in:

- Protecting engines from debris and road impact

- Supporting efficient lubrication and oil circulation

- Aiding thermal dissipation in modern engines

With increasing engine downsizing and higher operating temperatures, demand for robust and thermally efficient oil pan designs continues to rise.

Lightweighting Trends Support Aluminum Oil Pan Adoption

Automakers are increasingly replacing traditional steel oil pans with aluminum and composite variants to:

- Reduce overall vehicle weight

- Improve fuel efficiency

- Meet tightening emission and efficiency regulations

Aluminum oil pans, in particular, are gaining traction in passenger vehicles due to their corrosion resistance and superior heat dissipation.

Browse Full Report: https://www.factmr.com/report/3621/automotive-oil-pan-market

Growth in ICE and Hybrid Vehicle Production

Despite the long-term rise of EVs, internal combustion engine (ICE) and hybrid vehicles will remain dominant through 2035. These platforms continue to rely on advanced oil pan systems, sustaining long-term market demand.

Material and Technology Trends

Advancements in Oil Pan Design

Manufacturers are focusing on:

- Integrated baffles for improved oil control

- Noise and vibration reduction (NVH optimization)

- Crash-resistant and reinforced structures

Such innovations enhance engine longevity and overall vehicle reliability.

Composite Materials Gain Selective Adoption

Composite oil pans are emerging in premium and performance vehicles, offering:

- Weight reduction benefits

- Design flexibility

- Improved noise insulation

However, cost sensitivity limits large-scale adoption in mass-market vehicles.

Regional Growth Highlights

North America: Stable Demand from Pickup and SUV Segments

Strong production of pickup trucks, SUVs, and light commercial vehicles in the U.S. supports continued demand for durable and high-capacity oil pan systems.

Europe: Lightweight Materials and Emission Norms Drive Innovation

Stringent EU emission standards are pushing automakers toward aluminum and advanced steel oil pans, particularly in passenger cars and hybrid vehicles.

East Asia: Manufacturing Strength Supports Volume Growth

China, Japan, and South Korea remain key production hubs, benefiting from:

- Large automotive manufacturing bases

- Cost-efficient steel and aluminum processing

- Strong OEM–supplier ecosystems

Emerging Markets: Gradual Expansion with Vehicle Ownership Growth

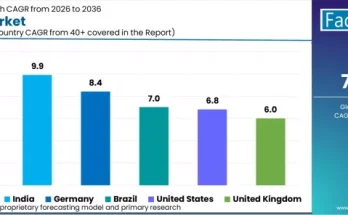

India, Southeast Asia, and Latin America are witnessing moderate demand growth due to:

- Rising vehicle parc

- Expansion of local automotive manufacturing

- Increasing focus on engine durability and cost efficiency

Market Segmentation Insights

By Material Type

- Steel Oil Pans – Widely used due to cost-effectiveness and durability

- Aluminum Oil Pans – Growing adoption for lightweighting and heat dissipation

- Composite Oil Pans – Niche but rising use in premium applications

By Vehicle Type

- Passenger Vehicles – Largest share due to high production volumes

- Light Commercial Vehicles (LCVs) – Steady demand driven by logistics and fleet growth

- Heavy Commercial Vehicles (HCVs) – Durable steel oil pans remain dominant

By Sales Channel

- OEMs – Primary demand source tied to new vehicle production

- Aftermarket – Replacement demand driven by wear, damage, and maintenance cycles

Challenges Impacting Market Growth

Limited Growth Pace Compared to Powertrain Innovations

Unlike electrified components, oil pans face slower innovation cycles, resulting in modest CAGR growth.

Raw Material Price Volatility

Fluctuations in aluminum and steel prices can impact production costs and supplier margins.

EV Transition in the Long Term

Pure electric vehicles eliminate the need for traditional oil pans, posing a long-term structural challenge—though impact remains limited through 2035.

Competitive Landscape

The automotive oil pans market is moderately consolidated, with manufacturers focusing on:

- Lightweight material integration

- Cost-optimized designs

- Long-term OEM supply contracts

Key Companies Profiled

- MAHLE GmbH

- Montaplast GmbH

- Röchling Group

- Dana Incorporated

- Benteler International

- Mann+Hummel

- Denso Corporation

Future Outlook: Stable Growth Anchored in ICE and Hybrid Vehicles

While electrification is reshaping the automotive industry, ICE and hybrid vehicles will continue to dominate global fleets over the next decade, ensuring steady demand for automotive oil pans. Ongoing improvements in materials, engine protection solutions, and thermal management will sustain market relevance.

As automakers balance cost efficiency, durability, and lightweighting, the global automotive oil pans market is positioned for consistent, long-term growth through 2035, reinforcing its role as a critical engine protection component across global vehicle platforms.