The $91 Billion Shift: How Hybridization and Urbanization are Redefining the Global Automotive Transmission Landscape

Electrification and Shifting Consumer Preferences in Emerging Markets Fuel a Projected 6.2% CAGR as the Transmission Sector Transitions Toward High-Value Architectures.

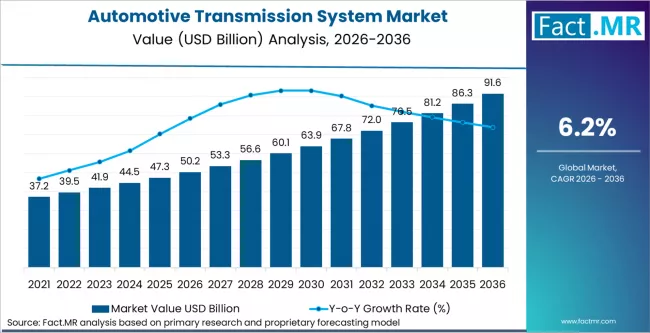

The global automotive transmission system market is entering a period of profound structural transformation. Valued at USD 50.23 billion in 2026, the industry is on a trajectory to hit USD 91.67 billion by 2036, expanding at a steady 6.2% CAGR, according to the latest strategic analysis by Fact.MR.

This growth represents more than just volume; it signals a “”technology bifurcation.”” While traditional manual gearboxes face headwinds, the surge in hybrid vehicle production and the demand for driving comfort in congested urban hubs are creating a massive USD 41.44 billion absolute dollar opportunity over the next decade.

The Value Migration: From Gears to Gadgets

The traditional image of the automotive gearbox is being replaced by sophisticated power-management systems. The report identifies that the market’s expansion is increasingly driven by the per-system value uplift found in hybrid drivetrains.

Dedicated Hybrid Transmissions (DHTs), electronic CVTs, and power-split devices often cost two to three times more than the conventional gearboxes they replace. As OEMs pivot toward hybridized fleets to meet stringent global emission standards like Euro 7 and CAFE, the transmission becomes a primary lever for efficiency, offsetting the volume loss seen in pure Battery Electric Vehicle (BEV) segments.

Key Market Catalysts

- The “”Comfort”” Conversion: In historically manual-dominant regions like India, Southeast Asia, and Latin America, rising urban congestion is flipping the script. Consumers are increasingly opting for Automatic (AT) and Automated Manual Transmissions (AMT) to combat driver fatigue, moving these technologies from premium add-ons to mass-market essentials.

- Regulatory Rigor: To comply with tightening CO2 targets, engineers are specifying high-ratio systems—such as 8-speed and 9-speed automatics and Dual-Clutch Transmissions (DCTs). These systems optimize engine operating points, providing the fractional efficiency gains necessary for fleet-wide compliance.

- The Hybrid Bridge: With gasoline vehicles still commanding 58.6% of the fuel type segment, the transition to full electric is being bridged by mild and full hybrids. This middle ground is where the most intensive transmission innovation is currently concentrated.

Regional Powerhouses: China and Japan Lead the Charge

The geography of the transmission market is shifting toward the East, where production scale meets rapid technological adoption.

| Region | Projected CAGR (2026-2036) | Primary Growth Drivers |

| China | 7.0% | Transition to DCT and AT configurations across domestic brands; world’s largest hybrid production base. |

| Japan | 6.8% | Dominance in advanced CVT and hybrid power-split systems for a global OEM base. |

| Germany | 6.2% | High-spec DCT investment for premium hybrid platforms and performance-oriented EVs. |

| United States | 6.1% | Sustained demand for heavy-duty automatic systems in the SUV and pickup truck segments. |

Strategic Outlook: The Industry at a Crossroads

“”The automotive transmission market is no longer a commodity business; it is a high-tech engineering battleground,”” states a lead analyst at Fact.MR. “”The manufacturers winning today are those who viewed the DCT as a bridge to hybridization rather than just an alternative to the manual stick. We are seeing a clear trend where transmission complexity is rising to meet the needs of 48V mild-hybrid systems, positioning these components as the ‘brain’ of the powertrain.””

For investors and decision-makers, the report highlights a critical window: the nomination cycles for next-generation hybrid platforms are happening now. Companies specializing in cost-competitive automatics for emerging markets and high-efficiency DHTs for the West are best positioned to capture the impending value migration.

Browse Full Report : https://www.factmr.com/report/11/autmotive-transmission-system-market

Competitive Landscape

The global market is defined by a mix of specialized Tier-1 suppliers and OEM in-house production, including:

Aisin Seiki, ZF Friedrichshafen AG, Jatco Ltd., Getrag (Magna), Eaton Corporation, Continental AG, Allison Transmission, BorgWarner Inc., GKN Automotive, and Marelli.

About the Research

This latest market analysis by Fact.MR provides an exhaustive look at the transmission systems of tomorrow, covering everything from 10-speed hydraulic automatics to specialized EV reduction gears. The study excludes heavy truck and motorcycle segments to provide a laser-focused view of the passenger and light commercial vehicle landscape through 2036.