Global Automotive Mats Market to Surpass USD 54 Billion as Precision-Fit ‘5D’ Systems and Premiumization Redefine Vehicle Interiors

Rising Vehicle Ownership in Emerging Economies and a Structural Shift Toward High-Value Fitted Configurations Drive USD 18.67 Billion Absolute Dollar Expansion Through 2036

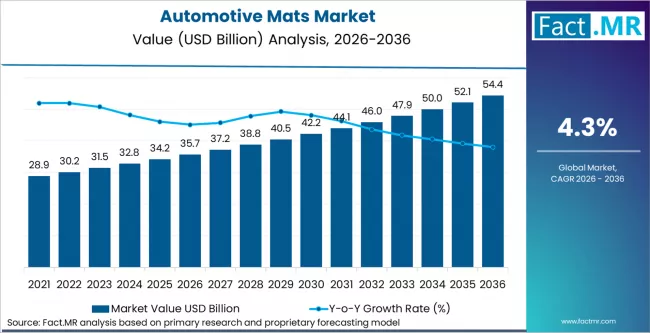

PIMPRI-CHINCHWAD, March 12, 2026 — The global automotive mats market is undergoing a significant transformation, evolving from a basic functional commodity into a high-margin segment of the vehicle personalization movement. According to latest industry analysis, the market is valued at USD 35.67 billion in 2026 and is projected to reach USD 54.34 billion by 2036, expanding at a steady 4.3% CAGR.

The surge is primarily attributed to a dual-speed market dynamic: sustained volume in rubber and standard mats within commercial fleets and emerging markets, contrasted by a rapid value-driven shift toward precision-fit 3D and 5D systems in the passenger vehicle sector.

Material Innovation and the Rise of “”Precision Fit””

While Rubber remains the dominant material—holding a 46.7% share in 2026 due to its unmatched durability and moisture resistance—the industry is witnessing an aggressive pivot toward advanced polymers. The transition from standard flat mats to vehicle-specific, laser-cut 3D and 5D configurations is significantly elevating average selling prices (ASPs).

“”We are seeing a structural bifurcation in the market,”” notes a senior analyst. “”Standard rubber and flat carpet mats continue to anchor volume, particularly in the LCV segment. However, the 5D mats category is the fastest-growing segment, as online retail and digital configurators make premium, multi-layered protection accessible to a broader consumer base.””

Key Market Drivers and Trends

- The Premiumization Effect: In mature markets like the United States, pickup truck and SUV dominance is driving a demand for heavy-duty, vehicle-specific fit profiles that command prices two to four times higher than generic alternatives.

- Emerging Market Acceleration: Expanding middle-class ownership in India and China is creating a massive secondary market. First-time buyers are increasingly viewing floor protection as an essential investment to preserve vehicle resale value.

- Commercial Fleet Cycles: Light Commercial Vehicles (LCVs) represent the fastest-growing vehicle segment. High daily wear in logistics and last-mile delivery necessitates regular replacement cycles, providing a stable foundation of recurring revenue.

Regional Performance Highlights

- China: Leads global growth with a 4.9% CAGR. As the world’s largest automotive producer, China’s market is fueled by rapid urbanization and a consumer culture that increasingly prioritizes interior aesthetics and hygiene.

- India: Projected at a 4.5% CAGR, the market is supported by rising ownership rates and an expanding aftermarket network serving consumers in monsoon-prone regions where moisture-resistant mats are a necessity.

- United States: Growing at a 4.1% CAGR, the U.S. remains a stronghold for “”all-weather”” rugged systems, with a high concentration of personal luxury vehicles and large-displacement trucks.

- Japan: Maintaining a 3.7% CAGR, the Japanese market is characterized by a preference for high-quality needle-punched designs and OEM-integrated accessory packages.

Market Breakdown at a Glance

| Metric | Details |

| Industry Size (2026) | USD 35.67 Billion |

| Projected Value (2036) | USD 54.34 Billion |

| CAGR (2026-2036) | 4.3% |

| Dominant Material | Rubber (46.7% Share) |

| Primary Vehicle Type | Passenger Cars (64.8% Share) |

| Leading Design | Needle-punched (55.4% Share) |

Strategic Outlook: The Digital Shift

The industry is moving toward a Direct-to-Consumer (D2C) model. Leading manufacturers are investing heavily in digital vehicle configurator tools, allowing consumers to identify precise-fit sets by make and model. This digital infrastructure is expected to reduce friction in the premium segment, moving sales away from traditional brick-and-mortar dependency.

Furthermore, sustainability is no longer optional. The rise of Thermoplastic Elastomers (TPE) and recycled materials is aligning product development with global circular economy goals, particularly in Europe and North America, where regulatory pressure on non-recyclable plastics is intensifying.

Competitive Landscape

The global market is defined by a blend of established OEM suppliers and innovative aftermarket brands. Key players driving innovation include:

- Auto Custom Carpets Inc., ExactMats, LLOYD MATS, Truck Hero Inc., BDK Auto, Shanghai Jun-Da Auto Decoration Co. Ltd., Lund International, Covercraft Industries LLC, Kraco Enterprise LLC, MacNeil Automotive Products Limited (WeatherTech), Husky Liners Inc., Intro-tech Automotive Inc., and Maxliner USA.

Browse Full Report : https://www.factmr.com/report/2/automotive-mats-market

About the Research Firm

Fact.MR is a distinguished market research firm and editorial powerhouse specializing in technical and industrial market sectors. With a focus on the circular economy and sustainable material innovation, the firm provides executive-level insights and data-driven frameworks to help industry leaders navigate complex global value chains.