The Selective Catalytic Reduction (SCR) catalyst market is poised for transformative growth through 2036, fueled by increasingly stringent global emission regulations, industrial expansion, and a strong push for cleaner combustion technologies. SCR catalysts, essential for reducing nitrogen oxides (NOx) emissions across automotive, industrial, power generation, and marine sectors, are becoming central to decarbonization and regulatory compliance strategies worldwide.

At the core of this growth is the role of SCR catalysts in mitigating NOx emissions, which are among the most harmful byproducts of fossil fuel combustion. These catalysts facilitate the conversion of NOx into nitrogen and water using reductants such as ammonia or urea, making them indispensable for controlling environmental pollution from engines and industrial combustion sources.

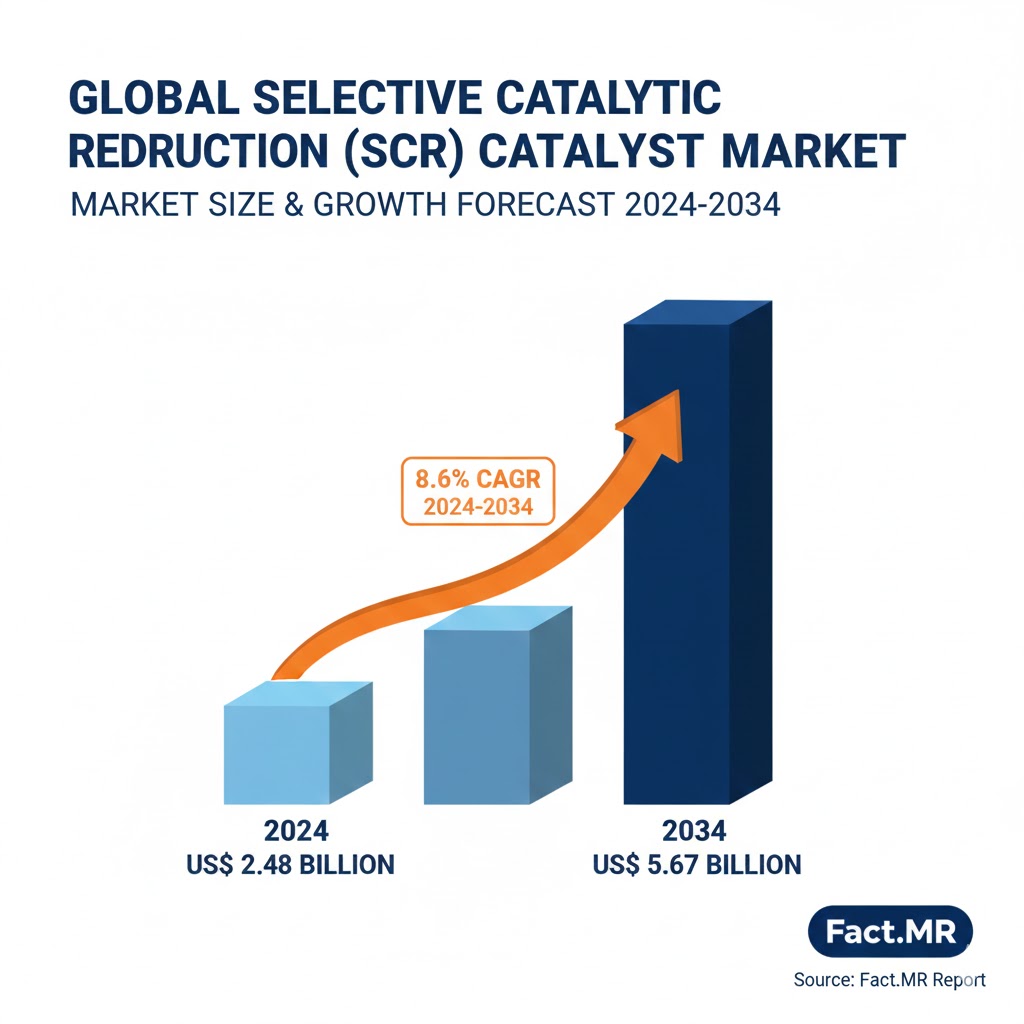

Market Growth Trajectory (2024–2036)

The global SCR catalyst market is projected to witness robust growth between 2024 and 2036, with the market size expected to more than double over this period, representing a compound annual growth rate (CAGR) of approximately 8–9%.

This sustained growth is underpinned by:

-

Tightening emission norms globally, including advanced standards for automotive and industrial NOx limits.

-

Industrial sector adoption, particularly in power plants, refineries, cement, and steel industries.

-

Accelerated adoption in marine engines due to stricter maritime emission regulations.

SCR catalysts will continue to see strong demand due to their critical role in NOx abatement, with technological advancements enhancing efficiency and durability.

Key Adoption Trends Shaping the Market

1. Regulatory Pressure and Compliance

The primary driver for SCR catalyst adoption is government regulations on NOx emissions. Manufacturers increasingly integrate SCR catalysts to meet these environmental compliance targets, particularly in heavy-duty diesel vehicles, power plants, and industrial units. Regulatory frameworks create a stable demand base that persists regardless of economic fluctuations.

2. Sectoral Demand Diversification

While automotive applications remain dominant, other sectors are rapidly adopting SCR catalysts:

-

Power plants are installing SCR systems to control NOx from boilers, turbines, and generators.

-

Petroleum refineries are enhancing denitrification to comply with stringent emissions standards.

-

Marine and rail applications are emerging as strong growth pockets, driven by sector-specific emission limits.

This diversification reduces dependency on a single vertical and reinforces market resilience.

3. Geographic Expansion

Market expansion is geographically varied:

-

Asia Pacific is expected to exhibit the fastest growth, fueled by industrialization and regulatory stringency.

-

North America maintains steady adoption due to environmental awareness and compliance initiatives.

-

Europe continues to be a critical market owing to stringent emission standards and an advanced automotive manufacturing ecosystem.

The global footprint ensures broad and sustained demand through 2036.

Portfolio Priorities: Innovation & Differentiation

Manufacturers are focusing on portfolio strategies to maintain competitive advantage:

1. Advanced Catalyst Formulations

Investments in advanced materials deliver:

-

Higher NOx conversion efficiencies

-

Improved durability under extreme conditions

-

Lower lifecycle costs

Emerging catalysts increasingly integrate predictive maintenance and sensor technologies for real-time performance optimization.

2. Sustainable and Circular Solutions

Companies are embedding sustainability across the catalyst lifecycle:

-

Recycling of precious metals

-

Reduction of raw material usage

-

Energy-efficient manufacturing processes

These initiatives reduce environmental impact while creating long-term operational efficiencies.

3. Customization for Sectoral Needs

Catalyst products are being tailored for specific sectors — automotive, marine, and power generation — reflecting segment-specific performance optimization and increasing adoption.

Competitive Landscape & Strategic Positioning

The SCR catalyst market is moderately consolidated, with leading manufacturers investing in:

-

Research and development for next-generation catalysts

-

Strategic partnerships and alliances with industrial and automotive players

-

Global production capacity expansion

-

Sustainability and circular economy initiatives

Collaborative innovation, such as partnerships between OEMs and catalyst producers, is becoming a key differentiator for long-term market leadership.

Future Demand Outlook to 2036

The SCR catalyst market is expected to remain highly attractive through 2036, driven by regulatory enforcement, industrial deployment, and technological evolution. Key trends include:

-

Continued focus on NOx reduction, even as renewable energy penetration increases, as legacy and hybrid combustion units require efficient emission control.

-

Maritime and rail applications continue to demand SCR solutions as alternative propulsion coexists with traditional engines.

-

Digital integration with real-time monitoring and analytics is set to enhance catalyst performance and compliance assurance.

Overall, long-term growth is expected to sustain a healthy CAGR, driven by environmental imperatives, industrial growth, and technological innovation.

Browse Full Report : https://www.factmr.com/report/4968/selective-catalytic-reduction-scr-catalyst-market

Conclusion

The SCR catalyst market represents a critical node in global emission control infrastructure. With strategic portfolio investments, sectoral adoption, and regulatory momentum, the market is on track for robust expansion through 2036. Companies focusing on advanced technologies, sustainability, and global reach are best positioned to lead in this evolving and impactful industry.