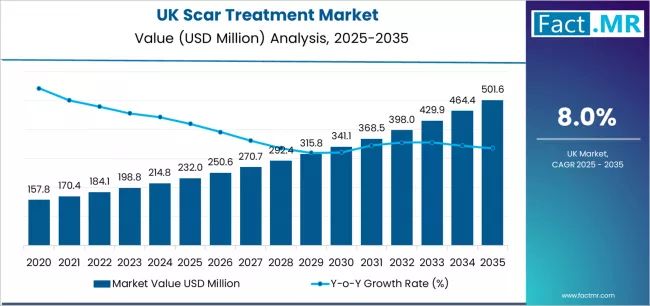

The market for scar therapy in the UK is expected to increase at a compound annual growth rate (CAGR) of 8.0% between 2025 and 2035, from USD 232.0 million in 2025 to over USD 501.6 million by that time.

The demand for scar treatment products in the United Kingdom is rising steadily, driven by growing aesthetic awareness, increasing incidence of surgical procedures, trauma injuries, acne-related scarring, and burns, along with rising acceptance of dermatological and cosmetic treatments. Scar treatment solutions are no longer viewed only as cosmetic products; they are increasingly recognized as part of holistic skin health and post-procedure recovery.

In the UK, both medical and cosmetic dermatology markets contribute to the expansion of scar treatment demand. Patients and consumers are actively seeking effective, non-invasive, and clinically supported solutions to improve skin appearance, texture, and confidence. This trend is supported by strong healthcare infrastructure, widespread access to dermatology services, and increasing self-care awareness.

Quick Market Overview (2025–2035)

- UK Scar Treatment Sales Value (2025): USD 232.0 million

- UK Scar Treatment Forecast Value (2035): USD 501.6 million

- UK Scar Treatment Forecast CAGR: 8.0%

- Leading Product Type in UK Scar Treatment Industry: Topical (67.3%)

- Key Growth Regions in UK Scar Treatment Industry: England, Scotland, Wales, and Northern Ireland

- Regional Leadership: England holds the leading position in demand

- Key Players in UK Scar Treatment Industry: Smith & Nephew plc, Lumenis Ltd., Merz Pharmaceuticals GmbH, Sonoma Pharmaceuticals Inc., Cynosure LLC, CCA Industries Inc., Mölnlycke Health Care AB, Suneva Medical Inc., Scar Heal Inc., Perrigo Company plc

To access the complete data tables and in-depth insights, request a Discount On The Report here: https://www.factmr.com/connectus/sample?flag=S&rep_id=12584

Market Overview

Scar treatment products are designed to reduce the appearance, thickness, discoloration, and texture of scars caused by surgery, acne, burns, injuries, or medical conditions. Common product formats include silicone sheets and gels, creams, ointments, oils, serums, and advanced dermatological therapies such as laser treatments, microneedling, and injectable fillers.

In the UK, demand spans both over-the-counter and prescription-based solutions. Consumers increasingly prefer evidence-backed products that are easy to use and suitable for long-term application. Additionally, dermatologists and plastic surgeons routinely recommend scar management as part of post-procedure care, reinforcing consistent market demand.

Key Market Drivers

1. Increasing Number of Surgical and Cosmetic Procedures

The UK continues to see growth in both medical and aesthetic surgeries.

-

Rising volume of orthopedic, cardiovascular, and general surgeries

-

Growth in cosmetic procedures such as tummy tucks, breast surgeries, and skin resurfacing

-

Post-operative scar management becoming standard care

This directly fuels demand for effective scar treatment solutions.

2. High Prevalence of Acne and Acne Scarring

Acne remains one of the most common skin conditions across all age groups.

-

Adolescents and young adults are major consumers

-

Persistent acne scarring drives long-term product usage

-

Increasing dermatological consultations for scar reduction

This supports sustained demand in the topical and clinical treatment segments.

3. Growing Aesthetic Consciousness and Self-Care Culture

Consumers in the UK are increasingly focused on appearance and skin health.

-

Greater acceptance of dermatological treatments

-

Influence of social media and beauty standards

-

Rising willingness to invest in skin improvement products

Scar treatment products benefit strongly from this trend.

4. Advancements in Dermatological Technologies

Innovation is expanding treatment effectiveness and options.

-

Improved silicone-based formulations

-

Non-invasive procedures like laser therapy and microneedling

-

Combination therapies for enhanced outcomes

These advancements increase adoption across both clinical and home-use segments.

Market Segmentation Analysis

By Product Type

-

Topical Scar Treatments:

Includes creams, gels, oils, and silicone sheets; widely used due to ease of application and affordability. -

Medical and Device-Based Treatments:

Laser therapy, microneedling, and radiofrequency treatments used in clinical settings. -

Injectable and Advanced Therapies:

Corticosteroid injections and fillers for severe or raised scars.

By Scar Type

-

Surgical Scars:

Largest segment due to routine post-operative scar management. -

Acne Scars:

High demand among teenagers and adults seeking cosmetic improvement. -

Burn and Trauma Scars:

Require long-term and specialized treatment approaches. -

Stretch Marks:

Often included within the broader scar treatment category.

By End User

-

Consumers (Home Use):

Major users of OTC creams, gels, and silicone products. -

Hospitals and Clinics:

Utilize scar treatment protocols for post-surgical recovery. -

Dermatology and Aesthetic Clinics:

Provide advanced procedures and combination therapies.

By Distribution Channel

-

Pharmacies and Drug Stores:

Trusted source for OTC scar treatment products. -

Online Retail Platforms:

Fast-growing channel offering convenience and product variety. -

Clinical Settings:

Prescription-based and procedural treatments delivered by professionals.

Regional Demand Trends within the UK

-

Urban Areas:

Higher demand due to concentration of clinics and cosmetic services. -

Metropolitan Regions:

Strong adoption driven by aesthetic awareness and disposable income. -

Healthcare-Centric Areas:

Increased usage linked to hospital-based surgeries.

Challenges and Market Restraints

1. Variable Treatment Outcomes

-

Results depend on scar type, age, and skin condition

-

Consumer expectations may not always align with results

2. High Cost of Advanced Treatments

-

Laser and injectable procedures can be expensive

-

Cost sensitivity limits access for some consumers

3. Long Treatment Duration

-

Many scar treatments require prolonged use

-

Slow visible improvement may affect compliance

Opportunities and Strategic Trends

1. Growth of Silicone-Based and Clinically Proven Products

Strong preference for dermatologist-recommended solutions.

2. Combination Therapy Approaches

Blending topical products with clinical procedures for better outcomes.

3. Expansion of E-Commerce and Direct-to-Consumer Brands

Online channels improving accessibility and education.

4. Increasing Focus on Preventive Scar Care

Early intervention post-injury or surgery to minimize scar formation.

Future Outlook

The UK scar treatment market is expected to grow steadily through 2035, supported by rising surgical volumes, strong aesthetic awareness, and ongoing innovation in dermatological treatments. While challenges such as cost and treatment variability remain, expanding product options and improved clinical protocols will continue to enhance adoption.

As scar management becomes an integral part of post-procedure care and personal skincare routines, demand for both topical and advanced scar treatment solutions will remain robust. Companies focusing on clinical efficacy, consumer education, and accessible treatment options will be best positioned to capitalize on future growth opportunities in the UK market.

Browse Full Report: https://www.factmr.com/report/united-kingdom-scar-treatment-market