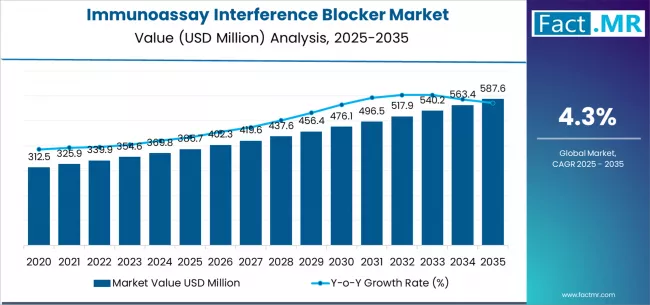

The global immunoassay interference blocker market is set for steady expansion over the next decade, driven by increasing demand for accurate diagnostic testing, rising prevalence of chronic and autoimmune diseases, and growing adoption of advanced immunoassay platforms in clinical laboratories. According to a new analysis by Fact.MR, the market is projected to grow from USD 385.7 million in 2025 to approximately USD 587.6 million by 2035, registering a total growth of 53.0% and an absolute increase of USD 204.4 million over the forecast period. This expansion reflects a CAGR of 4.3% from 2025 to 2035.

The increasing occurrence of heterophilic antibodies, rheumatoid factors, and human anti-animal antibodies (HAAA)—which can compromise immunoassay accuracy—is significantly accelerating the demand for effective interference blocker solutions worldwide.

Browse Full Report: https://www.factmr.com/report/immunoassay-interference-blocker-market

Strategic Market Drivers

Rising Demand for High-Accuracy Diagnostic Testing

Immunoassays are widely used in disease diagnosis, hormone testing, oncology, cardiology, and infectious disease detection. However, assay interference can lead to false-positive or false-negative results, increasing diagnostic risks.

Immunoassay interference blockers play a critical role in:

- Enhancing test reliability

- Improving diagnostic confidence

- Reducing repeat testing and misdiagnosis

This growing emphasis on precision diagnostics is fueling market adoption across healthcare settings.

Growth in Chronic and Autoimmune Diseases

The rising global burden of autoimmune disorders, cancer, cardiovascular diseases, and endocrine conditions has led to increased immunoassay testing volumes.

Patients with autoimmune conditions often exhibit elevated interfering antibodies, making interference blockers essential for:

- Accurate disease monitoring

- Long-term patient management

- Clinical decision-making

Expansion of Clinical Laboratories and Diagnostic Centers

Rapid expansion of independent diagnostic laboratories, hospital labs, and reference testing centers—especially in emerging economies—is driving consistent demand for assay optimization solutions.

High-throughput laboratories increasingly rely on interference blockers to maintain:

- Standardized results

- Regulatory compliance

- Operational efficiency

Technological Advancements in Immunodiagnostics

Continuous innovation in chemiluminescence immunoassays (CLIA), ELISA, and automated immunoassay analyzers is creating demand for compatible, high-performance interference blockers.

Manufacturers are focusing on:

- Broad-spectrum blocking reagents

- Species-specific antibody blockers

- Ready-to-use formulations for automation platforms

Regional Growth Highlights

North America: Diagnostic Innovation & High Testing Volumes

North America dominates the market due to:

- Advanced healthcare infrastructure

- High diagnostic test volumes

- Strong adoption of automated immunoassay systems

The U.S. leads in clinical laboratory testing and research-based diagnostics.

Europe: Regulatory Emphasis on Diagnostic Accuracy

Strict regulatory frameworks and quality standards across Europe are driving adoption of interference blockers to ensure accurate and reproducible diagnostic results. Germany, the U.K., France, and Italy remain key contributors.

East Asia: Expanding Healthcare & Lab Automation

Countries such as China, Japan, and South Korea are witnessing strong growth due to:

- Expanding hospital networks

- Rising diagnostic awareness

- Increased investment in laboratory automation

Emerging Markets: Improving Diagnostic Infrastructure

India, Southeast Asia, Latin America, and the Middle East are experiencing growing demand driven by:

- Expanding diagnostic labs

- Rising chronic disease prevalence

- Increased healthcare spending

Market Segmentation Insights

By Product Type

- Heterophilic Antibody Blockers – Widely used in routine immunoassays

- Human Anti-Animal Antibody (HAAA) Blockers – High demand in specialized testing

- Rheumatoid Factor Blockers – Growing adoption in autoimmune diagnostics

By Application

- Clinical Diagnostics – Largest segment due to high immunoassay volumes

- Research Laboratories – Increasing use in assay validation

- Pharmaceutical & Biotechnology – Drug development and biomarker research

By End User

- Hospital Laboratories

- Independent Diagnostic Centers

- Academic & Research Institutions

Challenges Impacting Market Growth

Limited Awareness in Developing Regions

Lack of awareness regarding immunoassay interference can limit adoption in low-resource settings.

Cost Sensitivity

Smaller laboratories may hesitate to adopt additional reagents due to budget constraints.

Assay-Specific Compatibility Issues

Interference blockers must be optimized for specific assay platforms, increasing formulation complexity.

Competitive Landscape

The immunoassay interference blocker market is moderately fragmented, with companies focusing on assay compatibility, formulation improvements, and strategic partnerships with diagnostic manufacturers.

Key Companies Profiled

- Merck KGaA

- F. Hoffmann-La Roche Ltd.

- Abbott Laboratories

- Thermo Fisher Scientific

- Bio-Rad Laboratories

- Siemens Healthineers

- Danaher Corporation

Recent Developments

- 2024: Introduction of next-generation broad-spectrum interference blockers for automated immunoassay platforms

- 2023: Increased adoption of interference blockers in high-sensitivity cardiac and oncology assays

- 2022: Diagnostic labs enhance quality control protocols to reduce assay interference-related errors

Future Outlook: Precision Diagnostics Drive Sustainable Growth

The immunoassay interference blocker market is poised for stable growth through 2035, supported by:

- Rising immunoassay testing volumes

- Expansion of precision diagnostics

- Automation of clinical laboratories

- Increased awareness of assay accuracy

As healthcare systems worldwide prioritize reliable diagnostics, patient safety, and regulatory compliance, immunoassay interference blockers will remain a critical component of modern diagnostic workflows.