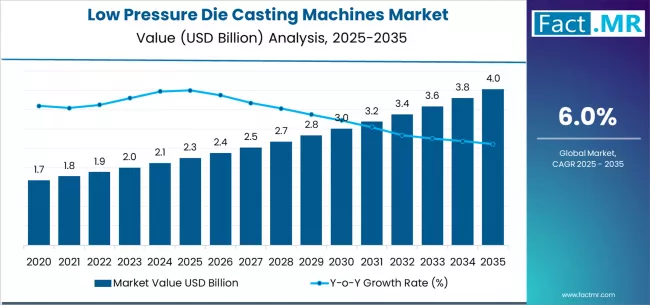

The Low Pressure Die Casting (LPDC) Machines market is on a robust upward trajectory, with a valuation of around USD 2.25 billion in 2025 and expected to reach USD 4.03 billion by 2035. The adoption of LPDC machines is accelerating due to rising demand for precision metal components — especially aluminum — across automotive, aerospace, electronics, and general engineering industries.

Quick Stats (2025 / 2035)

-

Global Market Value (2025): USD 2.25 billion

-

Projected Market Value (2035): USD 4.03 billion

-

Forecast CAGR (2025–2035): 6.0%

-

Leading Product Type: Automatic low pressure die casting machines (~56.1% share)

-

Leading Machine Configuration: Horizontal machines (~62.3% share)

-

Top End-Use Industry: Automotive (~52.6% share)

-

Key Growth Regions: Asia–Pacific, North America, Europe

-

Leading Companies: Buhler AG, Toshiba Machine Co. Ltd., Idra Group, UBE Industries Ltd., Dynacast International, SINTOKOGIO LTD., CPC Machines, LPM Group

To access the complete data tables and in-depth insights, request a Discount On The Report here: https://www.factmr.com/connectus/sample?flag=S&rep_id=12093

Market Overview

LPDC machines are essential for producing high-quality cast components with superior mechanical properties, reduced porosity, and excellent dimensional accuracy. Their ability to deliver lightweight, complex, and high-strength metal parts positions them as a preferred technology for modern manufacturing.

Automatic LPDC machines dominate global demand, reflecting the widespread shift toward automation and Industry 4.0 practices in foundries. Horizontal LPDC systems hold the largest configuration share due to their suitability for mass-production environments.

The automotive sector is the strongest end-use industry, driven by OEMs’ increasing focus on lightweighting to meet emission norms, boost fuel efficiency, and enhance EV performance.

Asia–Pacific remains the largest and fastest-growing region, supported by a strong manufacturing base, foundry modernization, and expanding automotive production. Europe and North America also contribute significantly, backed by advanced industrial infrastructure and increased use of high-performance cast components.

Key Market Drivers

1. Automotive Lightweighting & Aluminum Adoption

LPDC machines are gaining prominence as automakers transition toward lightweight aluminum components — such as wheels, structural elements, suspension components, and EV housing units. As electric vehicles grow, the need to reduce weight and improve efficiency accelerates the shift toward LPDC-based aluminum castings.

2. Surge in High-Precision Component Manufacturing

Industries increasingly demand complex, defect-free, and high-integrity castings. LPDC offers controlled metal flow, superior finish, tight tolerances, and fewer casting defects, making it suitable for critical applications in automotive, aerospace, and industrial machinery.

3. Automation & Industry 4.0 Integration

Modern LPDC machines offer real-time process monitoring, automated controls, digital interfaces, and optimized metal usage — supporting higher efficiency, lower scrap rates, and improved operational consistency. Digital foundries and smart manufacturing systems are driving rapid adoption.

4. Growth of Foundry Infrastructure in Asia-Pacific

Industrialization, capacity expansion, and technological upgrades across countries such as China and India are propelling the demand for LPDC machines. Local manufacturing of automotive and industrial components continues to fuel market growth.

5. Expansion Beyond Automotive

While automotive remains dominant, new opportunities are emerging in electronics housings, aerospace components, and industrial equipment — diversifying revenue streams for LPDC manufacturers.

Challenges in the Market

1. High Initial Investment Costs

Advanced automatic LPDC machines require substantial capital expenditure, posing challenges for small and medium-sized foundries, particularly in cost-sensitive regions.

2. Skilled Labor Requirement

LPDC operations require trained technicians who understand process dynamics, pressure control, alloy behavior, and defect minimization. Lack of skilled manpower can hinder adoption.

3. Limited Viability for Low-Volume Production

LPDC is highly efficient for medium-to-high volume production. However, for small-batch or basic castings, cheaper alternatives like gravity die casting or sand casting remain more economical.

4. Competitive Pressure and Margin Constraints

As more global and regional manufacturers enter the LPDC equipment market, competition intensifies. Companies increasingly differentiate through automation features, after-sales service, and process optimization rather than just hardware.

Future Outlook

The LPDC machines market is set for strong and sustained growth over the next decade. Expansion will be supported by rising aluminum component usage, EV penetration, and increased adoption of smart manufacturing systems.

Automation will evolve from optional to essential, with future LPDC systems offering fully integrated digital monitoring, AI-based defect prediction, minimal human intervention, and improved energy efficiency.

Industries beyond automotive — like renewable energy, aerospace, and industrial equipment — are expected to expand their reliance on LPDC technologies due to the need for lightweight, durable, and high-precision metallic structures.

Emerging markets will contribute significantly, as industrial growth, urbanization, and government-led manufacturing initiatives create strong demand for modern casting technologies.

Where Revenue Comes From — Now vs. Next

Revenue Sources Now (2025)

-

Automatic LPDC Machines: Highest contributor due to rising automation.

-

Horizontal Machines: Dominant segment because of automotive mass-production needs.

-

Automotive Components: Largest end-use segment, contributing over half of market revenue.

-

Core Regions: Asia-Pacific, North America, and Europe drive the majority of sales.

-

Capital Equipment Sales: Primary mode of revenue as foundries upgrade production lines.

Revenue Sources Next (Toward 2035)

-

Smart / Industry 4.0 Integrated LPDC Machines: AI-enabled control, IoT systems, and fully automated foundries will shape future revenue streams.

-

Electric Vehicle Component Casting: Demand for aluminum structural parts, battery housings, and heat-management components will boost LPDC adoption.

-

Expansion Beyond Automotive: Aerospace, defense, industrial machinery, and electronics will become high-value segments.

-

Emerging Market Growth: Increased adoption in Asia-Pacific, Latin America, and the Middle East.

-

Service-Based Revenue: Contract foundries and LPDC-as-a-service models will grow as smaller companies outsource casting operations.

Conclusion

The Low Pressure Die Casting Machines market is entering a phase of transformative growth. With increasing demand for lightweight, high-precision metal parts and the global shift toward electric mobility, the need for advanced LPDC systems is becoming more pronounced. While initial costs and skill requirements present challenges, the long-term benefits — including superior casting quality, automation capabilities, and optimized production — position LPDC technology as a core element of modern manufacturing.

Browse Full Report: https://www.factmr.com/report/low-pressure-die-casting-machines-market