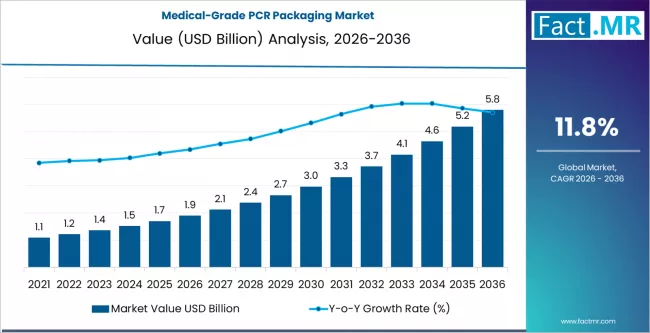

The global medical-grade Post-Consumer Recycled (PCR) packaging market is entering a phase of disruptive expansion, with its valuation projected to rise from USD 450 million in 2026 to USD 1.15 billion by 2036. According to a specialized industry analysis, the market is set to expand at a robust compound annual growth rate (CAGR) of 9.8%, driven by a structural shift in the pharmaceutical and MedTech sectors toward high-performance sustainable materials.

For decades, the medical industry relied exclusively on virgin plastics to ensure zero contamination. However, advancements in “Super-Sizing” mechanical recycling and chemical recycling (advanced recycling) have now produced PCR resins that meet the rigorous biocompatibility and purity standards required for medical applications. This breakthrough is allowing global healthcare brands to reconcile strict patient safety requirements with aggressive corporate ESG (Environmental, Social, and Governance) targets.

Summary Table: Medical-Grade PCR Packaging Market Outlook

| Metric | Details |

| Market Value (2026E) | USD 450 Million |

| Forecast Value (2036F) | USD 1.15 Billion |

| Projected CAGR (2026-2036) | 9.8% |

| Leading Material | PCR Polyethylene (42.5% Share) |

| Primary Application | Pharmaceutical Secondary Packaging (55%+ Share) |

| Highest Growth Market | India (12.2% CAGR) |

Request for Sample Report | Customize Report – https://www.factmr.com/connectus/sample?flag=S&rep_id=13631

Core Market Dynamics: Answering the Strategic ‘How’ and ‘Why’

Medical-grade PCR packaging involves the use of recycled resins—primarily Polyethylene (PE), Polypropylene (PP), and Polyethylene Terephthalate (PET)—that have undergone validated purification processes to be safe for contact with medical devices and pharmaceutical products.

-

Who is leading the sector? Industry pioneers including Berry Global, Amcor plc, Gerresheimer AG, Nelipak Healthcare Packaging, and West Pharmaceutical Services are at the forefront, partnering with resin specialists to secure high-purity PCR feedstocks.

-

What is the dominant material? PCR Polyethylene (PE) commands a leading 42.5% market share. Its versatility in producing flexible films, pouches, and squeeze bottles makes it the preferred choice for secondary and tertiary medical packaging, as well as non-sterile primary applications.

-

Where is growth most accelerated? India is emerging as a high-velocity market with a 12.2% CAGR, fueled by its role as the “pharmacy of the world” and new domestic plastic waste management rules. China follows with an 11.5% CAGR, supported by massive state-led investments in circular economy infrastructure.

-

Why is the technology shifting? The market is moving toward Chemical Recycling (Molecular Recycling). Unlike mechanical recycling, chemical processes break plastic down to its monomer state, effectively “resetting” the material to virgin-quality purity, which is critical for primary packaging that comes into direct contact with drugs or sterile implants.

Sector Insights: Pharmaceutical Secondary Packaging Leads Volume

The Pharmaceutical Secondary Packaging segment remains the primary application area, projected to hold over 55% of the market share by 2026. This includes folding cartons, trays, and outer wraps where the risk of migration to the drug product is minimal. However, the Medical Device Packaging segment is seeing the fastest growth as manufacturers redesign shipping containers and protective trays to include up to 50% PCR content.

“The ‘Virgin-Only’ era of medical packaging is ending,” the analysis states. “We are seeing a major trend where ‘Closed-Loop Medical Recycling’ is becoming a reality. Hospitals are beginning to segregate high-purity plastic waste (such as irrigation bottles and wrap) to be returned to manufacturers, creating a dedicated, high-quality PCR stream specifically for the healthcare industry.”

Key Market Trends and Strategic Outlook

1. Optimization through Multi-Layer Barrier Technology

A significant absolute dollar opportunity lies in Functional Barrier Laminates. Manufacturers are developing “sandwich” structures where a core layer of PCR is encapsulated between two thin layers of virgin plastic. This ensures that the recycled content provides structural volume while the virgin layers maintain the sterile barrier and regulatory compliance.

2. The Rise of “Mass Balance” Accounting

Innovation is currently focused on the regulatory side. The industry is adopting “Mass Balance” certification, which allows manufacturers to track the proportion of recycled feedstock used in their overall production process. This is a primary growth engine in the United States (9.2% CAGR) and European Union (10.5% CAGR), where brand owners need audited data to support their sustainability claims.

3. Regulatory Tailwinds and Plastic Taxes

Global regulations, such as the EU’s Packaging and Packaging Waste Regulation (PPWR), are becoming a massive tailwind. As governments introduce taxes on non-recycled plastic packaging, the “green premium” for medical PCR is shrinking, making it a cost-competitive alternative for large-scale pharmaceutical rollouts.

Investment Perspective: A High-Barrier, Essential Sustainability Niche

The medical-grade PCR packaging market represents a robust opportunity for specialty chemical and packaging firms. Because the regulatory barrier to entry is high—requiring extensive extractable and leachable (E&L) testing—established players with validated supply chains are positioned to capture the bulk of the “Sustainability Transition” spending from the world’s top 20 pharmaceutical companies.

Browse Full Report: https://www.factmr.com/report/medical-grade-pcr-packaging-market