The global Primary Charge Roller (PCR) market is poised for sustained expansion through the next decade, supported by increasing demand for high-performance electrophotographic printing solutions and ongoing maintenance cycles across commercial, office, and industrial print environments. The PCR market is expected to nearly double in value over the forecast period, driven by laser printing technology adoption, material innovations, and emerging regional opportunities.

Market Outlook: Growth Poised at a Steady Pace

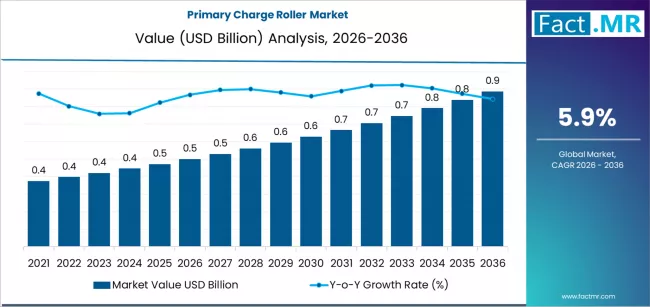

The global primary charge roller market is projected to grow from USD 0.5 billion in 2026 to approximately USD 0.9 billion by 2036, exhibiting a compound annual growth rate (CAGR) of 5.9% over the forecast period. This growth reflects strong replacement demand tied to installed hardware bases, particularly laser printers and multifunction devices, and ongoing investments in print quality optimization.

Key market drivers include:

-

Upgrading Commercial Printing Infrastructure: Rising enterprise and institutional print volumes require frequent component servicing to maintain output performance.

-

Focus on Operational Efficiency: Advanced PCRs improve charge distribution and operational stability across increasingly complex printing environments.

-

Regional Expansion: Rapid infrastructure growth in Asia Pacific and emerging markets supports broader adoption.

Segment Insights: Technology & Construction Trends

1. Printing Platform Dynamics

Laser printers dominate the PCR market, accounting for almost 68.2% of demand by value in 2026, due to:

-

Favorable installed base in commercial and enterprise environments.

-

Superior durability and output quality compared to other print systems.

-

Preference in high-duty cycles, necessitating robust PCR replacements to sustain print quality.

Multifunction printers (MFPs) and digital copiers also contribute notable demand, particularly in enterprise and education sector deployments.

2. Roller Construction Types

Conductive rubber PCRs lead the market with a 63.8% share, driven by uniform surface resistivity and durability under prolonged use. Other formats, such as foam and multi-layer rollers, serve niche applications where tailored charge distribution or lightweight designs are preferred but account for limited overall share.

Supply Chain Structure: OEM & Aftermarket Dynamics

The PCR supply stream is shaped by a balance of OEM cartridge production, certified remanufactured components, and service spares. OEM cartridges continue to command significant volume due to strict compatibility and warranty requirements, while remanufactured and compatible PCRs gain traction in cost-sensitive aftermarket segments. The interplay between quality assurance and pricing pressure represents a key competitive parameter.

Regional Landscape: Growth Hotspots & Strategic Opportunities

Asia Pacific: Unequivocal Growth Engine

Asia Pacific is a core growth engine, propelled by expansion across India, Indonesia, and Vietnam. India stands out with a forecasted CAGR of 6.7% through 2036, driven by expanding commercial print facilities, regulatory emphasis on print infrastructure optimization, and increased investment in advanced printing technologies. Indonesia and Vietnam are poised for above-average gains (~6.2% and 5.9% CAGR respectively), fueled by infrastructure development and rising digitalization.

North America & Europe: Mature, Quality-Centric Markets

North America, led by the U.S., is expected to grow at a moderate pace (U.S. CAGR ~2.3%) due to strong existing equipment penetration and steady replacement cycles. Europe, with Germany and other Western EU markets, continues to emphasize precision performance and integration standards across commercial printing lines.

Latin America & Emerging Regions

Mexico and Brazil are projecting mid-range growth (5.1% and 4.7% CAGR respectively) as commercial printing adoption stabilizes and service infrastructures mature.

Competitive Landscape: Established Players & Innovation Drivers

The PCR market is moderately consolidated, with global and regional players competing on performance, material innovation, and service reach. Key participants include:

-

Mitsubishi Chemical Group

-

Sumitomo Riko

-

CET Group

-

Katun

-

Static Control

-

Nippon Carbide Industries

-

Huaguang (HG) Photoconductor

-

Dinglong

-

UniNet

-

Aster Graphics

These players differentiate through robust R&D, precise material engineering (especially in conductive elastomers), and diversified distribution networks catering to OEM and aftermarket channels.

Market Drivers & Restraining Forces

Key Growth Drivers

-

Print quality imperatives: PCRs ensure uniform electrostatic charge distribution, reducing defects and enhancing resolution.

-

Maintenance-led demand cycles: The consumable nature of PCRs ensures recurring replacement demand.

-

Technology upgrade trajectories: Automated component compatibility and performance diagnostics boost demand for higher-spec PCRs.

Challenges & Restraints

-

Component cost pressures: High specification requirements and tight manufacturing tolerances can restrict adoption.

-

Technical complexity: Integrating advanced PCR designs into legacy fleets limits penetration and deployment ease.

Strategic Implications for Market Entrants

Opportunities for new entrants include:

-

Material Innovation: Conductive elastomers with stable resistivity and extended wear life offer competitive advantage.

-

Aftermarket Channel Growth: Partnerships with remanufacturers and service providers capture recurring demand.

-

Regional Partnerships: Focused strategies in high-growth Asia Pacific markets can accelerate adoption.

-

OEM Integrations: Aligning with OEM cartridge production can unlock scale advantages and strengthen product validation.

Browse Full Report : https://www.factmr.com/report/primary-charge-roller-market

Outlook Summary

The global primary charge roller market is forecast to deliver long-term, steady growth through 2036, driven by laser printing adoption, material advancements, and strategic regional dynamics. Sustained investment in OEM and aftermarket capabilities, combined with focused entry strategies in emerging markets, positions stakeholders to capitalize on recurring revenue streams in the print component ecosystem.