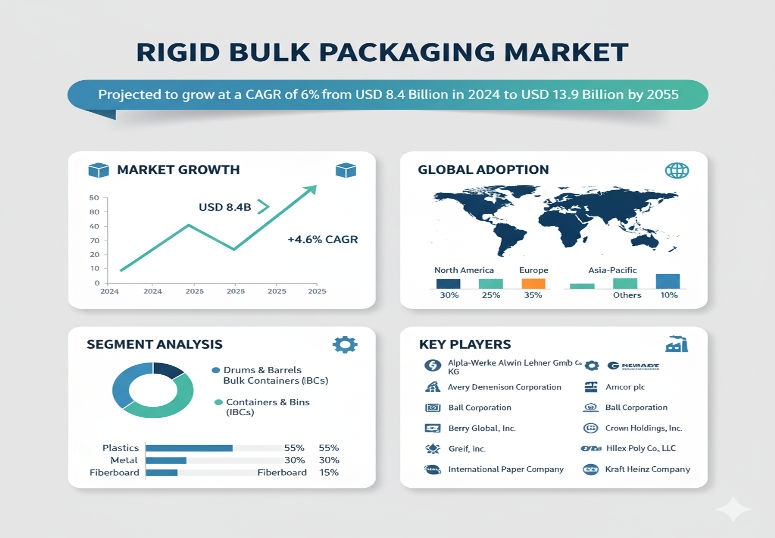

The global Rigid Bulk Packaging Market is undergoing a steady expansion, growing from an estimated USD 8.4 billion in 2024 to approximately USD 13.9 billion by 2035, at a compound annual growth rate (CAGR) of about 4.6%. This growth is being driven by sectors that demand durability, safety, and reliability—such as chemicals, food & beverage, pharmaceuticals—coupled with rising e-commerce, supply chain complexity, and sustainability demands. As supply chains span greater distances, the role of robust packaging that protects goods while enabling efficient handling is more vital than ever.

Market Dynamics & Growth Drivers

Several interconnected forces are shaping the rigid bulk packaging market. First, industries handling heavy or hazardous materials require containers that maintain structural integrity, resist environmental stress, and ensure safe transport—qualities intrinsic to rigid bulk packaging such as drums, intermediate bulk containers (IBCs), pails, and boxes.

Second, the growth of e-commerce and global trade is increasing demand for packaging that can withstand multiple handling steps, packaging and un-packaging, wide temperature or humidity variation, and longer transit times. Bulk packaging solutions that reduce damage, leakage, or spoilage are especially valued.

Third, sustainability has become a critical driver. Customers and regulators are increasingly pressuring for eco-friendly materials, greater recyclability, reusable designs, and reduction of packaging waste. Manufacturers are responding by introducing packaging made from recycled content, improving material efficiency, and seeking designs that are easier to recycle or reuse.

Fourth, regulatory oversight—particularly in food, pharma, and chemical transport—is pushing for stricter containment, safety, and traceability standards. Packaging that offers tamper evidence, barrier protection, and compliance with handling norms is increasingly preferred.

Segmentation & Key Material Trends

Rigid bulk packaging is segmented across materials, product types, end-use industries, and geography. Among material types, plastic (especially high-density polyethylene, polypropylene) maintains strong popularity due to its combination of durability, light weight, corrosion resistance, and cost efficiency. Metal packaging (steel, aluminum) remains critical where strength, barrier protection, or chemical resistance are required, especially in chemical or hazardous material sectors. Wood and composite materials play smaller roles, often for crates or pallets, though demand in certain industrial or export scenarios exists.

Product type segmentation sees intermediate bulk containers (IBCs), drums, pails, and rigid boxes dominating. IBCs are especially relevant in chemical, agrochemical, food & beverage, and pharmaceutical sectors, thanks to their reusability, ease of handling, and suitability for large volume liquids or granules. Drums and pails are used broadly across industrial and commercial sectors.

Regional Insights: United States, China & East Asia

United States

In the U.S., the rigid bulk packaging market is a mature yet steadily growing market. Demand is driven by strong industrial activity (chemicals, food & beverage, pharmaceuticals), regulatory expectations about safety and packaging standards, and increasing awareness of lifecycle costs (durability, reuse, recycling). The domestic supply chain, logistics efficiency, and infrastructure support help adoption of more advanced and sustainable rigid packaging solutions.

China & East Asia

East Asia, and China in particular, are among the fastest growing regional markets. China’s rapid industrialization, expansion in manufacturing and exports, rising inland logistics, and growing e-commerce all contribute to high demand for rigid packaging capable of supporting both domestic use and export. Growth rates in China are estimated above global average, driven by policies that encourage more advanced materials, infrastructure expansion, and environmental regulation. Other East Asia regions (Southeast Asia, Japan, Korea) similarly exhibit strong demand growth, particularly for packaging materials that combine strength with cost efficiency.

Key Players & Competitive Landscape

Major companies operating in the rigid bulk packaging market include Alpla-Werke Alwin Lehner GmbH & Co KG, Amcor plc, Avery Dennison Corporation, Ball Corporation, Berry Global, Inc., Crown Holdings, Inc., DS Smith plc, Greif, Inc., Mauser Packaging Solutions, Mondi Group plc, Novolex Holdings, Inc., PTT Global Chemical Public Company Limited, Sealed Air Corporation, Sidel Group, Sonoco Products Company, among others.

These players compete by investing in material innovation, improving durability and barrier properties, and incorporating recycled or bio-based content. Some focus on design optimization (lighter walls, stackable or nestable containers) to reduce shipping cost. Others emphasize after-sales service, supply chain integration, or strategic location of manufacturing and distribution to cut lead times and transportation cost. Sustainability credentials are increasingly part of competitive differentiation: certifications, eco-design, recyclable and reusable packaging solutions are signals customers demand.

Recent Developments & Innovation Signals

Recent developments reflect both incremental improvements and strategic shifts. New rigid bulk packaging designs are featuring smarter features: tamper resistance, better sealing, improved lids and closures, modular stacking for space optimization, and improved ergonomics in handling. There is accelerating use of recycled plastics, higher proportion of post-consumer resin, and bio-based polymers. Manufacturers are also exploring hybrid materials and composites that deliver strength while improving environmental profile.

On the technology front, advances in molding, injection technologies, liner technologies (for chemical resistance or barrier protection), and additive manufacturing for prototypes or small runs are helping manufacturers test and adopt new designs faster. Also, supply chain innovations—such as just-in-time production, improved return logistics for reusable containers, and better tracking or traceability—are improving cost and environmental performance.

Challenges & Barriers

While trends are favorable, several hurdles limit more rapid adoption. The upfront cost of advanced materials and machinery for durable, high-performance rigid packaging is high—this can limit adoption especially for small and medium enterprises. Infrastructure for recycling or reuse is variable: in many regions, collection and material processing lag, reducing the benefit of recyclable materials. Regulatory compliance across different geographies (in terms of safety, chemical containment, transportation) can add complexity and cost. Competition from flexible packaging—which is lighter, less expensive, and more material-efficient for certain applications—is a continuing restraint. Finally, volatility in raw material costs (plastics, metals) and energy input costs affect profitability and pricing stability.

Browse Full Report: https://www.factmr.com/report/rigid-bulk-packaging-market

Market Forecast & Strategic Takeaways

Over the 2025-2035 period, the rigid bulk packaging market is expected to grow from ~USD 8.4 billion in 2024 to ~USD 13.9 billion by 2035, at ~4.6% CAGR. Growth will likely be strongest in materials and designs that optimize sustainability, lighter weight, and ease of reuse. Plastic-based containers will retain dominance by volume, but metal and hybrid materials may capture premium segments—especially in chemical, hazardous materials, or export-grade applications.

For companies, strategic priorities include localizing production to reduce lead times, investing in material innovation and recycled content, optimizing packaging design for strength, weight, and shipping efficiency, and embedding sustainability and lifecycle cost as core value propositions. Building partnerships across logistics, recycling, and material suppliers will strengthen competitive positioning.